General Equilibrium and Efficiency

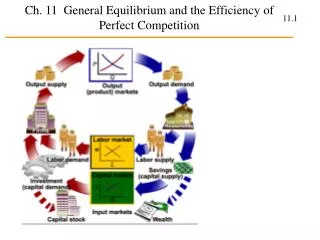

General Equilibrium and Efficiency. General Equilibrium Analysis is the study of the simultaneous determination of prices and quantities in all relevant markets. General Equilibrium (GE) occurs when: There is no excess demand or excess supply in any output or input markets

General Equilibrium and Efficiency

E N D

Presentation Transcript

General Equilibrium Analysisis the study of the simultaneous determination of prices and quantities in all relevant markets.

General Equilibrium (GE)occurs when: • There is no excess demand or excess supply in any output or input markets • Consumers are maximizing utility subject to budget constraints • Producers are maximizing profit subject to the production function • Input suppliers are optimizing

Economic Efficiency • An efficient (or Pareto efficient) allocation of goods is an allocation in which no one can be made better off without making someone else worse off.

Conditions of Economic Efficiency • Efficiency in exchange • Efficiency in production • Efficiency in the output market

Efficiency in Exchange • Efficiency in exchange occurs when • MRSA = MRSB • where • MRSi = marginal rate of substitution of good y for good x for consumer i, i = A, B • = amount of good y that consumer iis willing to give up for one more unit of good x

Example: 2 consumers Ann & Bob; 2 goods X & Y • Ann is willing to trade 4Y for 1X (MRSA = 4) • Bob is willing to trade 2Y for 1X (MRSB = 2) • Ann and Bob can benefit from trading, e.g., • If Ann trades 3Y for 1X she is better off since she is willing to pay 4Y. • If Bob receives 3Y for 1X he is better off since he would accept 2Y for 1X. • When MRSA > MRSB there are gains from trade. • Only when MRSA = MRSB can no one be made better off without making someone else worse off, and the Pareto efficient allocation occurs.

Efficiency in Production • An allocation of inputs is technically efficient if the output of 1 good cannot be increased without decreasing the output of another good. • Efficiency in production (or efficiency in the use of inputs in production) occurs when • MRTSx = MRTSy • MRTSj= marginal rate of technical substitution of labor (L) for capital (K) for good j , j = x, y • = amount by which K can be reduced when 1 more unit of L is used, so that output remains constant.

Example: SupposeMRTSx > MRTSy • e.g., MRTSx =4 and MRTSy=3 • For good x, producers can give up 4 units of K for 1 more unit of L, without changing output. • For good y, producers can give up 3 units of K for 1 more unit of L, without changing output. • Efficiency can be improved by using more K to produce good y and more L to produce good x. • When MRTSx = MRTSy, production efficiency cannot be improved by changing the input mix.

Efficiency in the Output Market • Efficiency in the output market occurs when • MRT = MRSA = MRSB • where • MRT = marginal rate of transformation of good y for good x • = amount of good y that must be given up to produce one additional unit of good x

Example: 2 individuals Ann & Bob; 2 inputs L & K; and 2 goods X & Y • MRSA = MRSB = 3, i.e., Ann and Bob are willing to trade 3Y for 1X. • MRT = 2, i.e., the economy can give up 2 units of Y to produce 1 more unit of X. • It benefits society to produce more Y and less X until • MRT = MRSA = MRSB

MRT = MCx/MCy • where • MCj = marginal cost of good j • = additional cost of producing 1 more unit of j • Example: MCx=$1, MCy= $2, MCx/MCy= ½ • The economy can produce 1 more unit of X for $1 or 1 more unit of Y for $2. • For $1, economy can produce 1 unit of X or ½ unit of Y. • The amount of Y that must be given up to produce 1 more unit of X is ½. (i.e., MRT = ½ ) • MRT = MCx/MCy

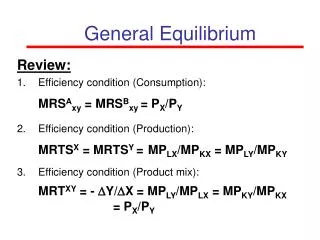

Economic Efficiency Summary • Conditions of Economic Efficiency • Efficiency in exchange: MRSA = MRSB • Efficiency in production: MRTS1 = MRTS2 • Efficiency in the output market: MRT = MRSA = MRSB • Note: For the entire economy, MRS must be equal for all consumers, MRTS must be equal for all firms, and MRT must be equal to MRS for all consumers .

First Welfare Theorem • The First Welfare Theorem (the Invisible Hand Theorem) • A competitive equilibrium is efficient.

A competitive equilibrium satisfies the 3 conditions for efficiency. • Efficiency in exchange: MRSA = MRSB • holds because constrained utility maximization requires • MRSA = Px/Py for Ann • MRSB = Px/Py for Bob and thus, • MRSA = Px/Py = MRSB • where Px is the price of good x and Pyis the price of good y.

Efficiency in production: MRTSx = MRTSy • holds in perfect competition because cost minimization requires: • MRTSx = w/r for good x • MRTSy = w/r for good y , and thus • MRTSx = w/r = MRTSy • where w = wage, r = rental rate on capital

Efficiency in the output market: MRT = MRSA = MRSB • holds because of the following. • MRT = MCx/MCy • Px = MCxfor profit maximization of firm 1 which produces good x • Py = MCyfor profit maximization of firm 2 which produces good y • These imply that: • MRT = Px/Py • For utility maximization: • MRSA = Px/Py = MRSB • Thus: • MRT = MRSA = MRSB