Download

1 / 12

120 likes | 619 Views

General Equilibrium and Market Efficiency. Production Economy. Pareto Efficiency. An allocation of goods in an economy is Pareto efficient if there is no other allocation that will make at least one individual in the economy better off without worsening the well-being of the others.

E N D

General Equilibrium and Market Efficiency Production Economy

Pareto Efficiency • An allocation of goods in an economy is Pareto efficient if there is no other allocation that will make at least one individual in the economy better off without worsening the well-being of the others. • There may be several Pareto efficient allocations of goods.

A simple production economy • Assume that two goods can be produced in the economy, clothing and food • Production of each one of the goods requires capital and labor. • Total quantities of the inputs are fixed • What is the optimal allocation of food and clothing to the two activities? • How to allocate the goods to Ann and Bill?

Condition 1 determining Pareto Efficient Allocation • Assume that technologies are convex • Then in a Pareto optimal allocation the marginal rates of technical substitution in production of the two goods should be equal. Assume MRTS for clothing is 5, while MRTS for food is 3 Then a benevolent planner can [fill the blank]. Therefore more food and clothing can be produced with the same amount of resources. Thus, the initial allocation was not Pareto optimal

Condition 2 determining Pareto Efficient Allocation • Assume that Ann’s and Bill’s preferences are (strictly) monotonic and convex • Then in a Pareto optimal allocation the marginal rates of substitution between the two goods (clothing and food) of Ann and Bill should be equal. Assume Ann is ready to exchange at most 5 units of food for 1 unit of clothing, but Bill’s MRS between food and clothing is 3 Then a benevolent planner can offer to take 4 units of food from Ann and give it to Bill in exchange for 1 unit of clothing. Both will agree, as the will be happier under the new allocation. Thus, the initial allocation of final goods was not Pareto optimal

Condition 3 determining Pareto Efficient Allocation • Define the Marginal rate of transformation between clothing and food, • In a Pareto optimal allocation the marginal rates of substitution between the two goods should equal to the marginal rate of transformation: Assume MRT between clothing and food is 5 and MRS of both consumers is 3 Then a benevolent planner can [fill the blank]. Therefore, both consumers will be happier. Thus, the initial allocation of inputs across production of food and clothing was not Pareto optimal

Generating Production Possibilities Frontier • Contract Curve in the Edgeworth production box is a set of all Pareto efficient allocations of inputs to production of clothing and food • The curve contains all the points (allocations) for which • Production possibilities frontier is the set of all possible output combinations that can be produced with a given endowments of factor inputs. • The slope of PPF is

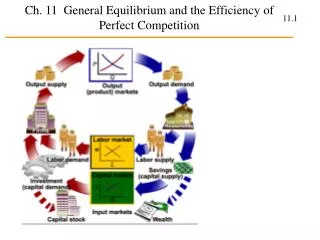

Equilibrium Allocation • Assume Ann and Bill own capital and a (fixed amount) of labor. They want to consume clothing and food. • Consider a Walrasian Auctioneer who announces prices for clothing, food, capital and labor in the economy • Once the prices are announced, the producers determine the amounts of labor and capital they want to employ, Ann and Bill announce their demand for clothing and food. • The procedure continues till the markets for capital, labor, clothing and food clear (supply for each good equals to the demand)

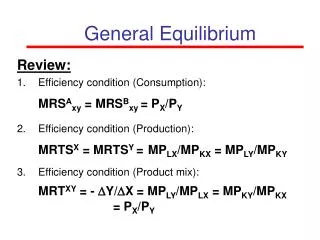

Condition 2 for Pareto Efficient Allocation is satisfied • Consumers choose how much to consume (clothing, food for Ann and Bill): • Marginal rate of substitution of Ann is equal to the ratio of output prices • The same is true for the marginal rate of substitution of Bill • Thus, the marginal rates of substitution of Ann and Bill are equal to each other!

Condition 1 for Pareto Efficient Allocation is satisfied • Firms choose a combination of inputs (labor, capital in each type of production): • Marginal rate of technical substitution between labor and capital in production of food equals to the ratio of input prices • The same is true for MRTS in production of clothing • Thus, the marginal rates of technical substitution in both activities are equal to each other!

Condition 3 for Pareto Efficient Allocation is satisfied • Firms choose the level of output (total clothing, total food): • The market value produced by the last unit of input (capital, labor) should equal to its rental price in production of food • The same is true for the market value of inputs in production of clothing • Thus, the market value produced by the last unit of capital is the same in both activities. The same is true for labor. The market value of the last unit of capital is its marginal product times the price of output. Therefore,

First Welfare Theorem The Invisible Hand • If • consumers and producers act as price takers; • there is a market for every commodity; • all the commodities are rival and excludable (there are no externalities neither in consumption nor in production); • consumers’ preferences and the production technologies are “well-behaved” • Then a market allocation is Pareto Efficient Q