Download

1 / 30

300 likes | 605 Views

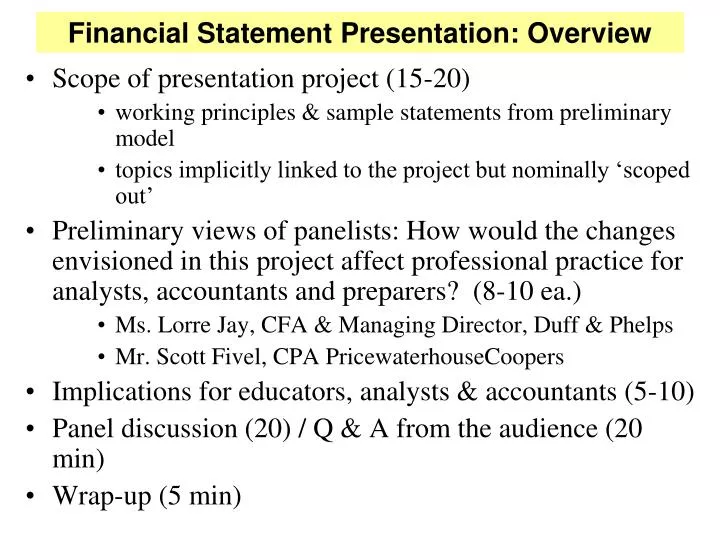

Financial Statement Presentation: Overview. Scope of presentation project (15-20) working principles & sample statements from preliminary model topics implicitly linked to the project but nominally ‘scoped out’

E N D

Financial Statement Presentation: Overview • Scope of presentation project (15-20) • working principles & sample statements from preliminary model • topics implicitly linked to the project but nominally ‘scoped out’ • Preliminary views of panelists: How would the changes envisioned in this project affect professional practice for analysts, accountants and preparers? (8-10 ea.) • Ms. Lorre Jay, CFA & Managing Director, Duff & Phelps • Mr. Scott Fivel, CPA PricewaterhouseCoopers • Implications for educators, analysts & accountants (5-10) • Panel discussion (20) / Q & A from the audience (20 min) • Wrap-up (5 min)

Financial Statement Presentation: objectives for this session • Alert educators to a standards-setting project which has potential to significantly affect the practice, use & teaching of accounting • Provide key-point summary of the project • Provide resources • specific FASB materials • influential documents (CFA CBRM) • Consider some implications for educators • course content • course sequencing • new skill sets that employers will need • Benefit from the range of skills and backgrounds present at this conference

Joint project with the IASB (since 2004; formerly known as Performance Reporting Project) • Purpose: establish a common, high-quality standard for presentation of information in the financial statements • Scope: • - All business entities (public and private) • - All financial statements • - Form, content, classification and display • - Aggregation into totals and subtotals • - Address non-financial institutions first; financial institutions next Financial Statement Presentation:Background & Scope (TJL 2/22/2007)

‘scoped out’ last update 8/3/2007

Most recent iteration of FSP 9/14/2007 JIG & FIAG meeting in Norwalk • Joint International Group • Financial Institutions Advisory Group • FASB & IASB • Minutes available under “Project Activities’ tab on FASB site – “meeting materials” • http://www.fasb.org/project/09-14-07_jig_fiag.pdf • Meeting handout provides basis for examining present scope of the project (§ x 9/14 HO) • FASB anticipates discussion through 2007, with discussion document due 1st Q 2008

Working Principles (§ 4, 9/14 HO) Financial statements should: a. Portray a cohesive financial picture of an entity b. Separate an entity’s financing activities from its business and other activities and further separate financing activities between transactions with owners in their capacity as owners and all other financing activities c. Disaggregate line items if that disaggregation enhances the usefulness of that information in predicting future cash flows.

Working Principles (§ 4 9/14 HO) – cont. d. Help a user assess an entity’s ability to: (1) Meet its financial commitments as they come due (including, but not limited to, its ability to raise capital and to use existing assets for generating future cash flows) (2) Invest in business opportunities. e. Help a user understand: (1) The basis on which assets and liabilities are measured (2) The uncertainty in measurements of individual A & L (3) What causes a change in reported amounts of individual assets and liabilities (4) The difference between cash-based & accrual accounting (5) The effects of noncash activities during the period on an entity's financial position.

Cohesiveness (§ 5 9/14 HO) “a corporate finance view of the firm” – TJL, 2/22/2007

Cohesiveness (§§ 10-13 9/14 HO) financial return focus is different from SFAS 95 ¶ 15 def. of investing – acquire / dispose of “assets held for or used in the production of goods or services . . . other than inventory” – 9/14 participants discussed sustainability focus

Disaggregation by Function & Nature (Agenda Paper 2, § 3-4 9/14 HO) • “Function refers to the primary activities in which an entity is engaged, such as selling a product or providing a service, cost of sales, research and development, marketing, and administrative activities.” • “Nature refers to the inputs (costs) required to accomplish those functional activities, such as costs related to people (labor and benefits), materials, energy, equipment (depreciation), and occupancy (rent).” • disaggregation increases ‘granularity’ of the information, improves analyst’s ability to separate recurring & non-recurring events (JIG Jan 2005)

Presentation of Income Tax Expense (Agenda Paper 2, § 7-8 9/14 HO) • The Boards are of the view that all income taxes, including those related to transactions with owners, should be presented in a separate section of the financial statements as income taxes are not related to the underlying transaction. Rather, income taxes are a form of income appropriation to taxing authorities. Moreover, members of both Boards generally agreed that any income tax allocation would be arbitrary and that the costs of providing this information exceed the benefits. • income taxes should no longer be allocated. . . all items, including discontinued operations and other comprehensive income (OCI) items would be presented on a pre-tax basis).

Long term goal: end OCI & ‘recycling’ • alternative presentations for intermediate future • distribute OCI in various sections of the statement in order to achieve ‘cohesiveness’; maintain recyclying • separate section, same prominence as other major sections (similar to current practice) • “long term / short term” classification for all items (position not fully worked out @ 9/14/2007) • similar to (1), but no recycling OCI (Agenda Paper 2, § 14-27 9/14 HO)

breakouts for intermediate determinates of income Alternative (1) distribution of OCI repeated disaggregation of natural expenses Alternative 1 – Agenda Paper 2,

IASB also has a view direct method “more cohesive”

this approach is ‘Alternative 1” – not presently favored by boards from CFA CBRM – Peter Knutson AIMR “Financial Reporting in the 1990’s and Beyond”

Sample Conundra • is pension expense part of COGS or financing? • should equity method income from an associate be presented in operating or financing section? • should dividends be deducted from comprehensive income? (“should equity be treated as a category separate from business and financing – answer may lie in conceptual framework & debt / equity projects”) • segment-level status for recognition of Discontinued Operations (see Discntd. Ops. project) • define exceptions based on “impractical” (comment in 9/14 meeting) • information may not exist for certain restatements (segment didn’t exist & information can’t be constructed)

some challenges ahead for all of us (1) • mastering the new model • transitioning through a period of uncertainty • no firm timeline for final rollout • there may be 2 or more interim treatments of OCI • complexity - interrelationship b/t this project & • Discontinued Operations ─ Codification • ongoing Fair Value work ─ Revenue Recognition • Conceptual framework • relevance to private companies • direct costs to implement (some of these may be borne by the accounting firms which frequently prepare the statements) • exacerbate practitioner/academic tension over scope & content of accounting education

some challenges ahead for all of us (2) • recasting financial metrics (how does ‘the end of Net Income’ affect DuPont analysis? • classification by nature & comparability – COGS info: • company A outsources all production • company B outsources 50% of production • company C produces 100% in-house • XBRL taxonomies will need to be updated • research: trend analysis, comparability to “before FSP project” data

skills our students will need in order to master this new model (1) • valuation • conceptual appreciation @ introductory course • awareness of ‘gaming’ issues - skepticism • ability to use valuation models will probably become a part of Intermediate • reconciliation (ability to produce reconciling schedules and to tie the statements together) • understanding of diverse business models • evaluate reasonableness of segment disclosure • ability to evaluate judgments about operating, investing and financing activities • enhanced ability to read and interpret footnote disclosure • understand the differences b/t legally independent subsidiary and internally-designated segments

skills our students will need in order to master this new model (2) • greater awareness of IS capabilities that will be needed to ‘tag’ and/or define accounting information • nature of expense • function of expense • segment which incurred the expense • operating, investing or financing • direct-method preparation of SoCF

challenges for educators – long term issues (1) • Are freshman going to be ready for the new model? • if not, when do we schedule the first course? • what impacts will this have on sequencing and curriculum design? • In which course(s) do we provide the skills necessary to work with this new model? • How will the introductory accounting course be structured? • can this new model be taught in one course, or will we need a second introductory course? • will it make sense to teach the introductory course with ‘clean’ & ‘simple’ examples (e.g. no ambiguous allocations, limited fair value, one segment, etc.) and then overlay complexity in Intermediate?

challenges for educators – long term issues (2) • Intro financial accounting has traditonally been gateway to business studies. If that is no longer feasible, what course takes its place? • Auditing class will spend more time examining allocations & classifications • Heightened prominence for SoCF • @ Geneseo students see this in 2-3 classes @ 102, in Intermediate I (2nd ½ of CH 5 KWW) and intensively in Intermediate II • most of them still struggle with it • finding time for more attention to this statement

challenges ahead for educators - transition issues • when will the textbooks be ready? when will be the cutover? • what arrangements will need to be made in downstream courses (e.g. Advanced, Theory, Financial Statement Analysis) for students who learned the old model? • ‘mixed’ classes

corporate challenges • one-time & ongoing costs for new systems • more segment disclosure & consolidation work • 9/14 panel quote: “I support the management approach . . . [but] there’s a caution . . . there’s a presumption that segments has all these attributes or that the corporation look at it [this way] I would say in our case I could not produce a segment balance sheet under this approach – we don’t measure internally that way . . . under SFAS 131 we’re not required to [do this]” • need to allocate some items to operating, investing and financing categories (e.g. CFO salary) • data collection

Greg Jonas (Moody’s) • Despite some criticisms . . . “this is one of the most important projects of any the board has ever undertaken from a user’s perspective . . . • it offers tremendous help . . . want to congratulate staff and board for . . . many wonderful ideas other comments • analysts argue for disaggregated revenue data • FPS is “back door” approach to mark-to-market accounting for everything