Download

1 / 1

10 likes | 87 Views

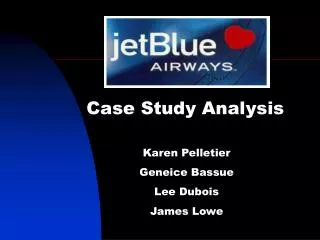

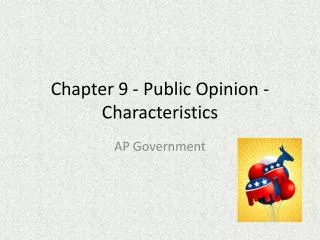

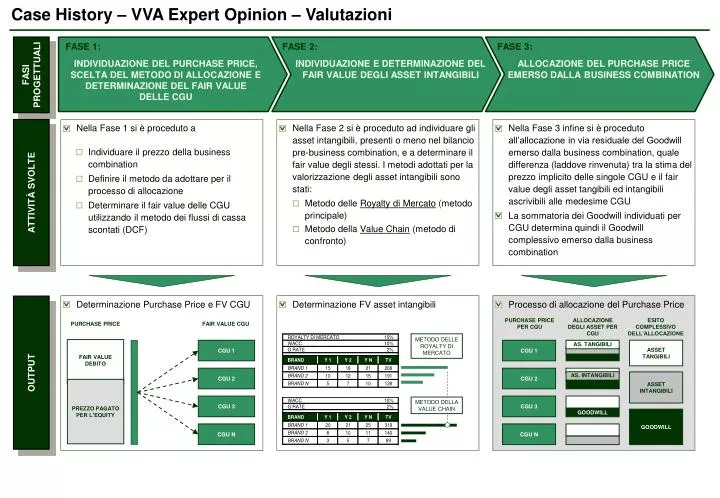

CGU 1. AS. TANGIBILI. CGU 1. ASSET TANGIBILI. CGU 2. CGU 2. AS. INTANGIBILI. ASSET INTANGIBILI. CGU 3. CGU 3. GOODWILL. GOODWILL. CGU N. CGU N. Case History – VVA Expert Opinion – Valutazioni. FASE 1:. FASE 2:. FASE 3:.

E N D

CGU 1 AS. TANGIBILI CGU 1 ASSET TANGIBILI CGU 2 CGU 2 AS. INTANGIBILI ASSET INTANGIBILI CGU 3 CGU 3 GOODWILL GOODWILL CGU N CGU N Case History – VVA Expert Opinion – Valutazioni FASE 1: FASE 2: FASE 3: INDIVIDUAZIONE DEL PURCHASE PRICE, SCELTA DEL METODO DI ALLOCAZIONE E DETERMINAZIONE DEL FAIR VALUE DELLE CGU INDIVIDUAZIONE E DETERMINAZIONE DEL FAIR VALUE DEGLI ASSET INTANGIBILI ALLOCAZIONE DEL PURCHASE PRICE EMERSO DALLA BUSINESS COMBINATION FASI PROGETTUALI • Nella Fase 1 si è proceduto a • Nella Fase 2 si è proceduto ad individuare gli asset intangibili, presenti o meno nel bilancio pre-business combination, e a determinare il fair value degli stessi. I metodi adottati per la valorizzazione degli asset intangibili sono stati: • Nella Fase 3 infine si è proceduto all’allocazione in via residuale del Goodwill emerso dalla business combination, quale differenza (laddove rinvenuta) tra la stima del prezzo implicito delle singole CGU e il fair value degli asset tangibili ed intangibili ascrivibili alle medesime CGU • La sommatoria dei Goodwill individuati per CGU determina quindi il Goodwill complessivo emerso dalla business combination • Individuare il prezzo della business combination • Definire il metodo da adottare per il processo di allocazione • Determinare il fair value delle CGU utilizzando il metodo dei flussi di cassa scontati (DCF) ATTIVITÀ SVOLTE • Metodo delle Royalty di Mercato (metodo principale) • Metodo della Value Chain (metodo di confronto) • Determinazione Purchase Price e FV CGU • Determinazione FV asset intangibili • Processo di allocazione del Purchase Price PURCHASE PRICE PER CGU ALLOCAZIONE DEGLI ASSET PER CGU ESITO COMPLESSIVO DELL’ALLOCAZIONE PURCHASE PRICE FAIR VALUE CGU METODO DELLE ROYALTY DI MERCATO FAIR VALUE DEBITO OUTPUT METODO DELLA VALUE CHAIN PREZZO PAGATO PER L’EQUITY