Download

1 / 58

580 likes | 663 Views

CHAPTER 6 Relation between Discount Factors,Betas,and Mean-Variance Frontiers. Main contents.

E N D

CHAPTER 6Relation between Discount Factors,Betas,and Mean-Variance Frontiers

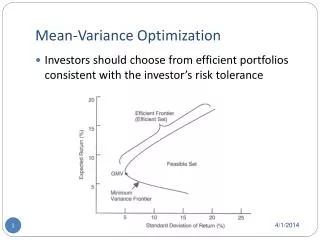

Main contents • we will draw the connection between discount factors,mean-variance frontiers, and beta representations,then we will show how they transform between each other,because these three representations are equivalent.

Transformation between the three representations(2) • . If we have an expected return-beta model with factors f , then linear in the factors satisfies . • If a return is on the mean-variance fron-tier,then there is an expected return-beta model with that return as reference variable.

Beta representation using m Multiply and divide by var(m),define ,we get:

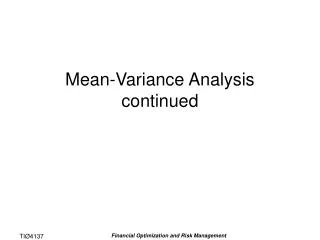

状态2回报 Rf R* 1 x* P=1(收益率) pc 状态1回报 Re* P=0(超额收益率)

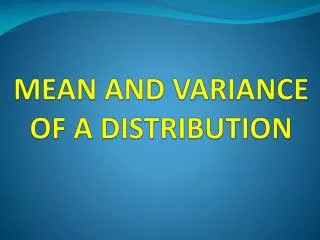

状态2回报 Rf R* 1 x* P=1(收益率) pc 状态1回报 Re* P=0(超额收益率)

6.2 From Mean-Variance Frontier to a Discount Factor and beta Representation

Proof(3) n

Note • If the denominator is zero, i.e., if ,this construction cannot work. • If there is a risk-free rate, we are ruling out the case • If there is no risk-free rate, we must rule out the case (the “constant- mimicking portfolio return”). • 证毕。

Proof • From (6.7), • Here we get (6.8) • where

6.4 Discount Factors and Beta Models to Mean-Variance Frontier

=E(R*2)/E(R*) 利用相似三角形 其长度为

Minimum-Variance Return • The risk-free rate obviously is the minimum -variance return when it exists. When there is no risk-free rate, the minimum-variance return is (6.15) • Taking expectations,

Risk-Free Rate • Here we will show that if there exists a risk-free rate,then all the zero-beta return, minimum-variance return,and constant-mimicking portfolio return reduce to the risk-free rate. • These other rates are: • Constant-mimicking:

Minimum-variance: • Zero-beta: • And the risk-free rate: (6.19) • To establish that there are all the same when there is a risk-free rate, we need to show that: