Download

1 / 27

270 likes | 419 Views

ELECTRONIC COMMERCE. CIT 245 Advanced Diploma in Information Technology - [ADIT II] and Advanced Diploma in Computer Science – [ADCS II] By Mohammed A. Saleh. STORED-VALUE CARDS.

E N D

ELECTRONIC COMMERCE CIT 245 Advanced Diploma in Information Technology - [ADIT II] and Advanced Diploma in Computer Science – [ADCS II] By Mohammed A. Saleh

STORED-VALUE CARDS Q: What looks like a credit or debit card, acts like a credit or a debit card, but isn’t a credit or a debit card ? A: Stored-value cards • Monetary value is normally preloaded onto the card. • It is distinguishable from as it is plastic and has a magnetic stripe on the back, although may not have the cardholder’s name on it.

STORED-VALUE CARDS • Used fro purchases, offline or online transactions. • The difference is that it can be obtained by anyone without prior to financial standing or having an existing bank account. • They come in two varieties: closed loop and open loop. • Closed loop is issued by a specific merchant or a merchant group (e.g shopping mall) and can only be used to make purchases from that merchant or merchant group.

STORED-VALUE CARDS • Example cards include: mail cards, store cards, gift cards and prepaid telephone cards. • Open loop (multipurpose) card can be used to make debit transactions at variety of retailer. • Used for other purposes such as direct deposits or withdrawing from ATM machines. • Some are issued by financial institutions with card association branding, Visa or MasterCard. • Examples include: payroll cards, benefit cards etc.

STORED-VALUE CARDS • Acquired in a variety of ways: • Employers or government agencies may issue them as payroll cards • Gift cards are purchased from and loaded by the merchant or merchant group. • Prepaid debit cards can be purchased by telephone, online or in in-person at various financial institutions. • The stored-value market is growing rapidly.

STORED-VALUE CARDS • Estimates show that there are over 2,000 store value programs with over 7 million branded cards in use today. • They are heavily marketed to the “unbanked” and “overextended” • Suits people with no bank accounts – people with low income, young adults, immigrants and minorities. • Established programs using stored-value cards include:

STORED-VALUE CARDS • EasySend program • Used in the US as an alternative way to transfer money securely to friends and relatives • An individual establishes a banking a/c, deposits money in the account and mails the EasySend card to relative or friend who then withdraws cash from an ATM machine.

STORED-VALUE CARDS • Visa Buxx • operation explained in Case Study 3.0 (tutorial)

E – MICROPAYMENTS • Consider the following online shopping scenarios: • A customer wanting to purchase a single CD for $8.95 • A person going online to buy an archived news article for $1.50 • A person goes to an online gaming company, selects a game and plays it for 30 minutes. The person owes the company $3 for playing time.

E – MICROPAYMENTS • All these are examples of e-micropayment, which are small online payments normally under $10. • Credit cards do not work well with such kind of payments. • History of e-micropayments is one of the unfulfilled promises and collapsed companies. • Digicash, First Virtual, Cybercoin and Internet Dollar are some of the micropayment companies that went under during the dot-com crash.

E – MICROPAYMENTS • Factors that led to their demise is the fact that early users of the Internet thought that digital content should be free. • Today evidence depicts out that users are willing to pay for content, music services, and applications for mobile devices such as ring tones and game. • The success of Apple iTune’s store shows this, it sold about 70 million songs at 99 cents during its first year of operation and 250 million songs in January 2005.

E – MICROPAYMENTS • Companies have developed e-micropayment products. They all enable online purchases under $10 but they differ: • BitPass (bitpass.com) • To use it a customer establishes a “buyers a/c” and adds money to the account via PayPal or a credit card. • For merchants or providers. BitPass can be hosted or implemented by adding BitPass gateway software to EC sites.

E – MICROPAYMENTS • When they click BitPass-enabled content, they are prompted for their password. • After the buyer has been authenticated and approved, the buyers BitPass a/c is debited, and the merchant is paid by PayPal. • Paystone (paystone.com) • Buyers establish prepaid accounts using their bank’s bill payment service or merchants impelement Paystone by adding special links to Paystone’s e-micropayment system.

E – MICROPAYMENTS • When they click on the link, they are taken to Paystone’s system where they are authenticated. • After a purchase, their accounts are debited and redirected back to the content they purchased. • PayLoadz (payloadz.com) • Works in conjuction with PayPal. • Buyers actually purchase content through PayPal.

E – MICROPAYMENTS • For merchants or providers to use PayLoadz, they need to establish accounts at both PayPal and PayLoadz and add special PayLoadz links to their EC checkout pages. • When a purchase is made, the PayLoadz site works behind the scenes with the PayPal site to complete the transaction and to notify the buyer by email where they can obtain the content they purchased.

E – MICROPAYMENTS • For merchants or providers to use PayLoadz, they need to establish accounts at both PayPal and PayLoadz and add special PayLoadz links to their EC checkout pages. • When a purchase is made, the PayLoadz site works behind the scenes with the PayPal site to complete the transaction and to notify the buyer by email where they can obtain the content they purchased.

E – MICROPAYMENTS • Peppercoin (peppercoin.com) • Users normally enter their credit card or debit card information just as they would with any other purchase. • To avoid the transactions costs associated with credit and debit card purchases, the Peppercoin software works in the background, aggregating the purchases of multiple buyers into a few large transactions.

E – CHECKING • Growing rapidly. • By 2003, online e-checks grew by 210%, reaching 500 million transactions. • Currently 27% of Web merchants surveyed offer e-check payment. • Merchants hope that this will raise sales by reaching consumers who do not have credit cards or who are unwilling to provide credit card numbers online.

E – CHECKING Definition: • It is an electronic version or representation of a paper check • Contain the same info. as a paper check and can be used wherever a paper check are used and are based on the same legal framework. • With an e-check, the buyer provides the merchant with his or her a/c number , bank routing number, bank a/c type, name of the bank a/c and the transaction amount.

E – CHECKING • Most businesses rely on 3rd party software to handle e-check payments. • CheckFree, Telecheck, AmeriNet, Paymentech and Authorize.Net are some of the major vendors of software and systems that enable an online merchant to accept and process e-checks directly from a Web site.

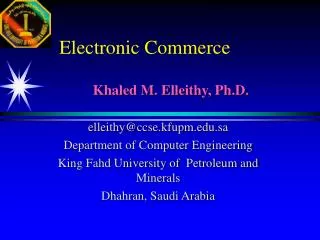

Processing E-Checks with Authorize.Net Authorize.Net’s Bank (ODF) Customer 1 Internet 3 2 6 Merchant Authorize.Net* 5 4 7 Customer’s Bank (RDF) 5 ACH Network 4 Merchant’s Bank Account

E – CHECKING Step 1:merchant receives written or electronic authorization from a customer to charge his or her bank a/c. Step 2: merchant securely transmits the transaction info. to the Authorize.Net Payment Gateway server. - The transaction may be accepted or rejected based on the criteria defined by the Payment Gateway

E – CHECKING Step 3: If accepted, the transaction is sent as an Automated Clear House (ACH) transaction to its bank (Originating Depository Financial Institution or ODFI) Step 4: ODFI then forwards the transaction to the ACH Network for settlement. It then uses the bank a/c info provided with the transaction to determine the bank that holds the customer’s a/c (known as Receiving Depository Financial Institution or RDFI).

E – CHECKING Step 5: The ACH Network instructs the RDFI to charge or refund the customer’s a/c. The RDFI passes the funds from the customer’s account to the ACH Network. Step 6: The ACH Network relays the funds to the ODFI (Authorize.Net’s bank). ODFI passes any returns to Authorize.Net Step 7: Authorize.Net deposits the e-check proceeds into the merchants account.

E – CHECKING The ACH Network • It is a nationwide batch-oriented e-funds transfer system that provides for the interbank clearing of e-payments for participating financial institutions. • ACH Operators include the Federal Reserve and Electronic Payments Network. • These operators transmit and receive ACH payment entries.

E – CHECKING • ACH entries are of two sorts; A credit entry where this credits a receivers account and a debit entry, which debits the receivers account. Assignment 2 • What are the benefits of E-checking? • Five benefit • Submit on the 18th June, 2009 • Single page – Word processed, font 12, Times New Roman