Download

1 / 14

140 likes | 268 Views

T en Years of the EURO Inspiration for the Czech Republic HOLGER KINTSCHER Member of the Board of Management Škoda Auto a.s. Praha 25. 1 1.200 8. Production plants in the Czech Republic. Kvasiny Superb , Roomster Production : 76 Tsd cars Staff : 3 . 2 Tsd. Vrchlabí

E N D

Ten Years of the EURO Inspiration for the Czech RepublicHOLGER KINTSCHERMember of the Board of Management Škoda Auto a.s. Praha 25.11.2008

Productionplants in theCzechRepublic Kvasiny Superb, Roomster Production: 76Tsd cars Staff: 3.2Tsd. Vrchlabí OctaviaTour, Octavia Production: 100Tsd. cars Staff: 1.3Tsd. Poland Prague 75 Km 135 Km Germany Pilsen Ostrava Mladá Boleslav Octavia Fabia Production: 399Tsd. cars Staff: 22.5Tsd. Brno Slovakia Austria

30 countries 172 Tsd. Cars 28% share of export Škoda markets in 1991

Škoda markets 2008 100 countries 690 Tsd. cars 89% share of export

Δ% Key figures 1-9/2008 vs.1-9/2007 Deliveries to customers Tsd.cars 531 462 14.8 3.1 Numberofemployees Tsd.emp. 26.2 25.4 10.5 Turnover Million.€ 6,359 5,755 (14.3) Profit before tax Million.€ 451 527 5

Key figures 1-9/2008 vs.1-9/2007 (76) 531 527 69 14,8% 14,3% 2007 451 462 1-9/2007 1-9/2007 1-9/2008 1-9/2008 Deliveriestocustomers(Tsd. cars) Profitbefore tax (Million €) 6

Significant impact on Škoda Auto Externalimpacts Financial crisis More expensive / restrictivefinancingofproducts (cars) Decreaseoftotalmarkets Extreme Competition pressure in Central Europe CO2-Discussion/Legislation Negative exchangeratedevelopment(CZK, USD, GBP..) 7

Development of the exchange rate CZK/EUR Averagerate 1-9/2007 28.08 CZK/EUR Averagerate 1-9/2008 24.81 CZK/EUR Evaluation 11.6% 8

2.601 Revenues and Costs simulation Basis: Skoda Auto:1-9/2008 Million. € 6,091 5,626 1 % others* 32% 68 % EUR 56% ? 31% 12% Naturalhedging CZK Revenues Costs * USD, GBP, JPY, CHF, DKK, NOK, SEK, SKK, PLN 9

Revenues and Costs simulation Basis: Skoda Auto:1-9/2008 Costs 43Bill. CZK 1,740 Revenues 18Bill. CZK (82) 1,574 + 84 + 166 724 640 28.08 CZK/€ 24.81 CZK/€ 28.08 CZK/€ 24.81 CZK/€ 1-9/07 1-9/07 1-9/08 Million€ 1-9/08 10

Million € Impactof CZK/EURExchange RateDevelopment on Škoda Auto 1-9/2008 in comparison to 1-9/2007 (166) 84 (82) Revenues Costs Impact

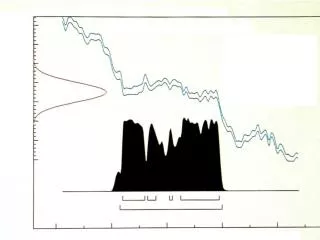

Planning stability ??? CZK/€ 14.10.08 23.10.08 29.10.08 18.11.08 Averagerate 2007 27,76 CZK/EUR Highestrate 2008 26,36 CZK/EUR Lowestrate 2008 22.97 CZK/EUR 12

Advantagesofswitchingfromlocalcurrency CZK to EUR • Eliminationoftheexchangerate risk of CZK/EURandrelatingcosts - purchaseandsales in EUR • Stableplanning / good sign forinvestors • Simplifyingoftheaccountingandtreasuryoperations • More transparent pricepolicy 13

Škoda challenges • To win the fight against financial crisis • To assure the finance stability of the company • To bring the figures back to 2007 level • To stay in the first league of automotive industry Skoda prefers EURO Implementation as soon as possible, because with Euro we will manage our challenges better 14