Download

1 / 103

1.03k likes | 1.12k Views

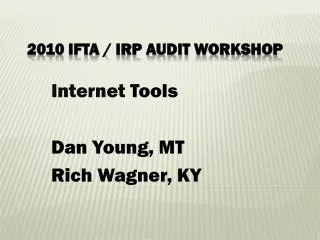

Partner Contracted Audit Workshop. October 27 & 28, 2011. Seven Months Timeline. 12. Start. 1. 11. End. 2. 2 weeks. 1 week. 10. 2 weeks. 1 week. 3 Months. 3. 5 weeks. 9. 4 Months. 2 week. 3 weeks. 2 weeks. 8. 4. 1 week. 8 weeks. 2 weeks. 7. 5. 6.

E N D

Partner Contracted Audit Workshop October 27 & 28, 2011

Seven Months Timeline 12 Start 1 11 End 2 2 weeks 1 week 10 2 weeks 1 week 3 Months 3 5 weeks 9 4 Months 2 week 3 weeks 2 weeks 8 4 1 week 8 weeks 2 weeks 7 5 6

Selecting the Applicable Scope of Work • Selecting the correct SOW depends on your award / subward type: 1- Grants and Cooperative Agreements (Except FOGs) Audit of the Fund Accountability Statement Scope of Work (Attachment No. 4 of the USAID/WBG Audit Guidelines)

Selecting the Applicable Scope of Work 2- Contracts (except firm fixed price / firm unit price) Audit of the Cost Representation Statement Scope of Work (Attachment No. 5 of the USAID/WBG Audit Guidelines)

Selecting the Applicable Scope of Work 3- Firm Fixed Price / Firm Unit Price Contracts and Fixed Obligation Grants (FOGs) Examination of Compliance with Terms and Conditions of the Award (Attachment No. 6 of the USAID/WBG Audit Guidelines)

The SOW Sections You Need to Fill In • Audit Title • Background Information • Terms of Performance • Payment Terms

Completing the Applicable Scope of Work 1- Audit Title: Use the language from the “Subject” of the Audit Notification Letter. Example1: (Prime Co.)

Completing the Applicable Scope of Work Example 2: (Sub Co.)

Completing the Applicable Scope of Work 2- Background Information Project Start and End Dates Expenditures incurred During the Audit Period Project Objectives Geographical locations of Operations Beneficiaries

Completing the Applicable Scope of Work (Background Info.) Category of Major Costs Incurred (salaries/ Workshops / Construction / Food Supply etc. Other Information: Period of Suspended Operations, Late Project Start Up, etc.

Where Can You Find the Background Information? Quarterly Reports Your Award & its Amendments Geo MIS / PMP Info

Sample 1 of Title & Background InformationAudit of Prime’s Cost Representation Statement (see handout)

Sample 2of Audit Title & Background InformationClose-out audit of Sub’s Fund Accountability Statement (see handout)

Sample 3 of Audit Title & Background InformationClose-out Examination of Sub’s Compliance (see handout)

Completing the Applicable Scope of Work – Terms of Performance 3- Terms of Performance The time period to be inserted by the auditee for the duration of the audit engagement which covers the period from signing the audit contract through issuance of the final draft audit report by the audit firm to the auditee. • Per the timeline chart, it is recommended to provide the audit firm with 4 months to issue their final draft report.

Completing the Applicable Scope of Work – Payment Terms 4- Payment Terms The auditee can choose the suitable payment terms provided thata significant amount is paid only after RIG/C approves and issues the report. Example: • 70 percent upon receiving the draft audit/exam. report. • 30 percent on the date the final report is approved and issued by the RIG/Cairo.

Completing the Applicable Scope of Work Exercise Complete the applicable Scope of Work for ABC Co.’s first year audit (10-15 minutes)

1- Scope of Work Content – Fund Accountability Statement Illustrative Fund Accountability Statement

1- Scope of Work Content – Fund Accountability Statement II- Objectives: What the auditor needs to do? • Conduct a financial audit – Express an opinion on the Fund Accountability statement. • Understand internal controls related to the award. • Assess control risk and identify reportable conditions. • Determine whether the recipient complied, in all material respects, with award terms and applicable laws and regulations.

1- Scope of Work Content – Fund Accountability Statement III- Audit Scope: What steps and tests should auditors follow /conduct? A- Pre-Audit Steps • Lists some applicable documents that the auditors should review such as the agreement, budget, progress reports, etc.

1- Scope of Work Content – Fund Accountability Statement B- What auditors need to test (sample only) • Direct & Indirect Costs • Procedures used to control the funds • Procurement procedures • Salaries and related benefits, travel & transportation, etc. • Technical assistance and services procured. • Compliance with USAID policies and local laws and regulations • Cost sharing schedule, if applicable. Auditors Can Definitely Go Beyond What is Listed!

1- Scope of Work Content – Fund Accountability Statement C- Cost-Sharing Schedule D- Internal Controls This will determine the extent, timing and nature of tests to be applied. E - Compliance with Award Terms and Applicable Laws and Regulations Key Areas Are: VAT, Vetting and Mandatory Clauses. F - Indirect Cost Rates Provisional Rate VS. Final Rates

1- Scope of Work Content – Fund Accountability Statement G - Follow-Up on Prior Financial Reviews and Audit Recommendations Any findings raised in the financial reviews that were not fixed will be reported as current findings. H – Other Audit Responsibilities

1- Scope of Work Content – Fund Accountability Statement IV- Audit Reports (attachment #1 under Partners Resources – Audit Matters) • The auditors should submit to the auditee the draft audit report. The auditee shall submit the draft report to the USAID/WBG to prepare for the exit conference if USAID/WBG plans to attend. • Once the auditors issue the final report to the auditee, the auditee shall submit the final report to USAID/WBG for general review. USAID/WBG will then submit the final signed report via email to the RIG/C for technical review and issuance.

1- Scope of Work Content – Fund Accountability Statement The report shall: A- Contain a title page, table of contents, transmittal letter and a summary which includes: (1) a background section (2) the objectives and scope (3) a brief summary of the audit results on the fund accountability statement, questioned costs, internal control, compliance with award terms and applicable laws and regulations (4) a brief summary of the results of the review of cost-sharing contributions; and (5) a brief summary of the recipient's management comments regarding their views on the audit results and findings.

1- Scope of Work Content – Fund Accountability Statement B - Contain the auditor's report on the fund accountability statement, identifying any material questioned costs not fully supported with adequate records or not eligible under the terms of the awards. C- Contain a report on the auditor's review of the cost-sharing schedule. D- Contain the auditor's report on internal control. (Scope of auditor’s work and reportable conditions).

1- Scope of Work Content – Fund Accountability Statement E - Contain the auditor's report on the recipient's compliance with award terms and applicable laws and regulations related to USAID-funded programs and projects. (material instances). All material questioned costs resulting from instances of noncompliance must be included as findings in the report on compliance and cross-referenced to the fund accountability statement.

1- Scope of Work Content – Fund Accountability Statement F - If applicable, for local recipients, contain the schedule of application of indirect cost rate and the auditor's report on the schedule of application of indirect cost rate. G- Contain the auditor's comments on the status of prior audit recommendations.

1- Scope of Work Content – Fund Accountability Statement V- Inspection & Acceptance of Audit Work and The Report Will be covered tomorrow. VI- Relationships and Responsibilities Examples: • The audit firm will contact USAID/WBG to obtain obligations and disbursements information. • The audit firm will contact RIG/C for any audit scope limitation. • The auditee will contact USAID/WBG for any questions related to the audit process.

1- Scope of Work Content – Fund Accountability Statement VI- Relationships and Responsibilities (Continued) • The audit firm shall immediately notify the auditee and USAID/WBG of any key/essential Personnel's departure and the reasons therefore. • The audit firm shall take steps to immediately rectify this situation and shall propose a substitute candidate for each vacated position along with an impact statement in sufficient detail to permit evaluation of the impact on the program. VII- Terms and Performance Refer to the audit timeline sheet.

2- Scope of Work - Cost Representation Statement Similar to the Fund Accountability Statement SOW except that it covers the audit of the Contractor/Sub Contractor’s Cost Representation Statement instead of the Recipient/Sub Recipient Fund Accountability Statement. It also covers the other areas such as Internal Controls and Compliance with Contract Terms and Applicable Laws and Regulations.

3- Scope of Work – Examination of Compliance • Financial statements are not audited/presented. The main objectives is to determine whether: 1- The contractor/grantee complied with the award terms and conditions; and 2- Had internal controls in place related to the award. Therefore, the auditor issues a report on compliance and a report on internal controls.

Scope of Work – Final Remarks • The Prime should use only one scope of work if it applies to more than one award / sub award. Example: If the partner has 5 subs who qualify for an examination audit, then use one examination SOW and provide the required info. For each of the 5 subs. Title 1 …………………………………. Background 1………………………... Title 2………………………………….. Background 2………………………... . .

Scope of Work – Final Remarks • Once you complete your applicable SOW, you need to send it to WBGPCA@usaid.gov for review and approval. • DO NOT DELETE / MODIFY any of the applicable SOW content. • Contact USAID/WBG if you need to add other items or concerns that you like to draw the auditor’s attention to or certain areas you want the auditor to focus on based on your knowledge of the project under audit.

Subject: Solicitation of Proposals Main Steps for Partners: I. Prepare the Request for Proposal (RFP) package II. Send the RFP to RIG/Cairo approved audit firms

Subject: Solicitation of Proposals I. Preparing the Request for Proposal (RFP) package: • Scope of Work, approved by USAID • Cover letter, explaining what Partner wants in the RFP Sample of cover letter • Sample Evaluation Criteria: ◘ Past Performance ◘ Past Experience ◘ Audit Team Qualifications ◘ Proposed completion schedule ◘ Proposed cost

Subject: Solicitation of Proposals Why is it important for the partner to include the evaluation criteria in the RFP? • Basis for evaluation – objectiveness • Transparency – so that all audit firms receive the same treatment • Consistency – compare apples with apples • Equity – to fairly evaluate the proposals • So that the Audit Firms address them in their proposals

Subject: Solicitation of Proposals II. Sending the RFP. • Partner issues the solicitation package to all RIG/Cairo approved audit firms by e-mail. Audit Firms List • In case of audit request for prime and sub/s, it is preferable for the partner to issue one RFP. • Time Frame: not more than 5 weeks for the entire RFP / Evaluation / Selection process.

Subject: Solicitation of Proposals Questions

Evaluation & Selection of Audit Firm - Overview • Procurement Officer receives proposals from audit firms. • Requesting Office(r) forms a Technical Evaluation Committee (TEC) at request of Procurement Officer [Sample detailed technical guidance (optional – not PCA specific) to the TEC members for evaluating proposals included in the binder]. Sample Technical Guidance for TEC Members.doc

Evaluation & Selection of Audit Firm - Overview • TEC Reviews and evaluates proposals based on evaluation criteria in the RFP. • TEC prepares selection memorandum and draft audit contract. • Procurement Officer approves and submits selection memo and draft audit contract to USAID/WBG for review and approval.

TEC Reviews and Evaluates Proposals • The TEC must use the same selection criteria in the RFP to ensure transparency, equity, and consistency. • The TEC assigns a weight or score for each criteria. • Weight and score allocated to cost cannot be controlling factor. • The TEC reviews and evaluates the proposals and selects the audit firm. • The TEC documents the evaluation and selection process in a selection memorandum.

Sample Evaluation Criteria • Firm’s past performance in terms of: a) quality of work conducted b) quality of the audit reports c) timeliness, and d) backlog of pending RIG/C audits. • Where to get information about audit firms’ past performance? a) Partner’s own experience with the audit firm. b) Other partners (reference checks). c) USAID/WBG, Financial Management Office. Evaluation Criteria of Audit Firms 2.docx

Sample Evaluation Criteria • Firm’s past experience in terms of conducting similar engagements, • Experience and credentials of the firm’s proposed team to participate in the audit, a) Appropriate mix of the audit team, and b) Level of involvement of each audit team member in conducting the engagement. Evaluation Criteria of Audit Firms 2.docx

Sample Evaluation Criteria - Continued • Proposed completion schedule, and • Cost. However, audit cost cannot be the only or controlling factor in the selection criteria. Please see sample evaluation criteria in the provided binder. Evaluation Criteria of Audit Firms 2.docx