Download

1 / 13

130 likes | 262 Views

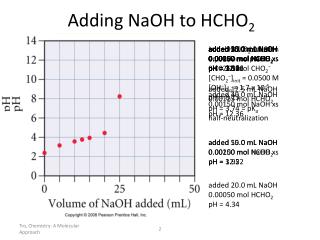

Key Challenges in the Deployment of ‘Value Added’ Services for Telecoms Operators. Jean Herv é Jenn President – Convergys EMEA. Agenda. Challenges in the global communication industry Opportunities for Telecom operators Q-Tel example. 1,600. Developed Markets - Telecoms Market Size.

E N D

Key Challenges in the Deployment of ‘Value Added’ Services for Telecoms Operators Jean Hervé JennPresident – Convergys EMEA

Agenda • Challenges in the global communication industry • Opportunities for Telecom operators • Q-Tel example

1,600 Developed Markets - Telecoms Market Size Global - Telecoms Market Size 1,200 1,400 1,000 1,200 1,000 800 Pay TV BB Internet NB Internet 800 600 Mobile Fixed Voice 600 400 400 200 200 0 0 1999 2000 2001 2002 2003 2004 2005 2006 2007 1999 2000 2001 2002 2003 2004 2005 2006 2007 Source: Pyramid Research Source: Pyramid Research The Dynamics of the Industry are Changing for Fixed & Mobile Access and Pay TV revenues will contribute an increasing proportion to global telcos Fixed operators in first-tier, core markets can no longer hide from substitution

Telecom and Cable operators are competing for a $1,200bn industry Technology Industry Cable Industry Telco Industry Entertainment $171.4bn Primary Battle Internet Access $74.7bn 30 25 Extended Battle 28.1 24.6 25 20 20.5 16.2 Information $13.6bn 20 13.4 15 15.8 15 Cable modem subs (m) DSL subs (m) 10.5 10 7.4 10 Enterprise Services $160.0bn 5 5 0 0 Extended Battle Fixed Telephony $403.1bn 2003 2005 2003 2005 Primary Battle Wireless Telephony $375.7bn ISP Industry

VoIP is Disruptive in Residential and Corporate Markets Residential market Corporate market Global fixed line voice “Merrill Lynch has made the strategic decision to deploy Cisco IP telephony and call center solutions to create a new IP-powered virtual call center” Cisco website, 2002 $403bn 5000 users Later to be scaled globally VoIP revenues $bn “IBM is in the midst of ripping out that infrastructure and replacing it with Ethernet, not just for speed and manageability, but also because it can support IP telephony” nwfusion.com, 3-Mar-2003 “The insurance industry isn't renowned for the adoption of leading-edge technology so the implementation of VoIP at Lloyds represents a departure from tradition” Chris Rawson, CIO, Lloyds 2003

Telecom operators are Seeking to Offer a New Customer Experience Value Tomorrow: The new customer experience Phase 4: Provider of value-added info-media-comm services • Multiparty conferencing • Real time interactive entertainment and information • Web agents Phase 3: Provider of media services • Personal digital multi-media library • Video library • Intelligent search and retrieval tools Today: Providing connectivity Phase 2: Connecting devices in the home • Wi-Fi technology • Connect all home devices • Home networking Phase 1: Bundling of voice and data • Fixed line telephony • Wireless telephony • High speed Internet access Time Source: Goldman Sachs Strategic Group

Fixed/Mobile Convergence New Service Mix Leading Operator Approaches

Prepay / Postpay Challenges Operator Consumer • Separate rating and billing platforms for prepaid and postpaid • Current prepaid solutions lack flexibility in supporting requirements of next-generation 2.5G/3G services • Prepaid consumers demand same level of service offerings • Consumers demanding next-generation services IT Infrastructure Services Payment Methods ROI • Subscribers demand flexibility of multiple payment options • Enterprise users demand flexibility in combinations of prepaid and postpaid accounts • High operational overheads associated with multiple platforms • Limited up-sell and cross-sell opportunities

Prepay / Postpay Convergence • Prepaid/Postpaid become payment options • Multi-service prepaid from one balance • Integration of Prepaid and Postpaid accounts • Prepaid style financial control available to Postpaid customers • Pre-event rating, advice of charge, authorisation • Single database for all customers, services and tariffs

Technology Offers Service Convergence, but Customer Segments Drive Divergence Convergence Divergence • Multiple Products & Services • Multiple Customer Segments • Multiple Brands • Multiple Business Models • Voice & Data • Devices & Services • Fixed & Wireless • Prepaid & Postpaid • Switched & IP Integration of systems • Front office Back office • Customer Management • Web Services • Business Intelligence • Predictive analytics • Billing and rating • Mediation • Order management • Activation

Q-Tel Example: Total Convergence Wireless & Mobinet Internet Qatar - QTel Network Planning Call Collection and Activation Web Self-Care Banks Customer Care Order Mgmt Finance &Accounts Clearing House NII (Inventory Mgmt) Work ForceAutomation Fraud Document MgmtGroup1 Wireline (Voice/Data) Qatar Cablevision (QCV)

Qtel Implementation Highlights Functionalities Partnership • Customer Care • Order popular products on line • Service Order Management • Rate for all services • Bill and print (English and Arabic supported) • Collections (including e-mail, SMS and IVR reminders) • Payments: Credit Card, Direct Debit, Cash (in shops), ATM to come • Web Self Care • Confidence in its suppliers and partners • Knowledge transfer and expertise • Ability to address current and future requirements • A solution to manage diverse businesses, with convergent processes • Responsive support, shared vision and strategic advice

Thank you for your time Jean Herve JennPresident – Convergys EMEA