Download

1 / 2

30 likes | 244 Views

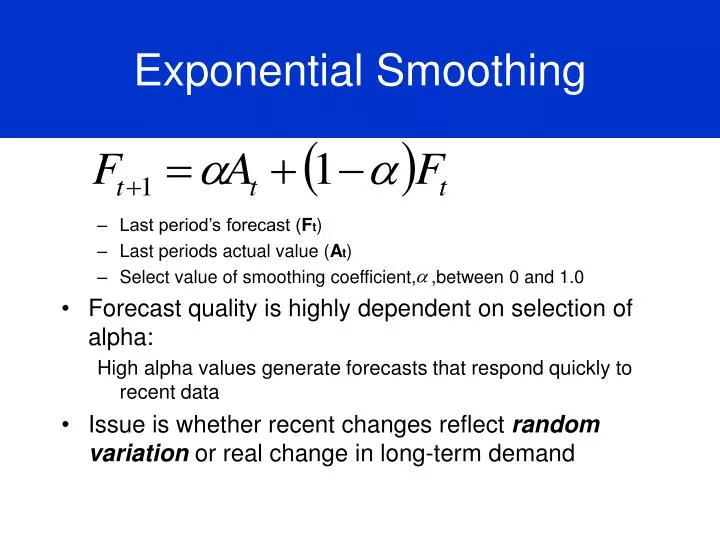

Exponential Smoothing. Last period’s forecast ( F t ) Last periods actual value ( A t ) Select value of smoothing coefficient, ,between 0 and 1.0 Forecast quality is highly dependent on selection of alpha: High alpha values generate forecasts that respond quickly to recent data

E N D

Exponential Smoothing • Last period’s forecast (Ft) • Last periods actual value (At) • Select value of smoothing coefficient, ,between 0 and 1.0 • Forecast quality is highly dependent on selection of alpha: High alpha values generate forecasts that respond quickly to recent data • Issue is whether recent changes reflect random variation or real change in long-term demand

Selecting Appropriate Value of Smoothing Constant • The larger the value of alpha the more sensitive the forecast will be to the current demand • Use low value of alpha when demand data has high variability (i.e. up & down) • Use larger value of alpha when demand data has low variability • Alpha should probably be between 0.01 and 0.30 – higher value may place too much value on last period’s actual random variation