Download

1 / 11

110 likes | 332 Views

Exponential Smoothing. Part 2 – Holt’s Local Linear Trend Through Part 4 – Damped Trend. Holt’s Local Linear Trend. Holt (1957) extended SES to allow forecasting of data with trends. Two smoothing parameters: α and β * with values between 0 and 1. Simple Exponential Smoothing.

E N D

Exponential Smoothing Part 2 – Holt’s Local Linear Trend Through Part 4 – Damped Trend

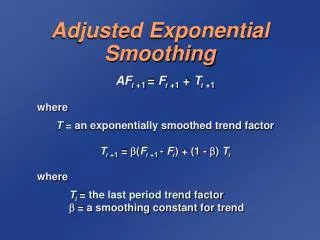

Holt’s Local Linear Trend • Holt (1957) extended SES to allow forecasting of data with trends. • Two smoothing parameters: α and β* with values between 0 and 1.

Simple Exponential Smoothing • lt denotes an estimate of the level of the series at time t. • bt denotes an estimate of the slope of the series at time t.

Optimization • Need to find α and β* by minimizing the value of MSE • We also optimize MSE for l0 and b0. • Optimizing over four parameters starts getting complicated…

Holt’s Method in R • fit1 <- holt(strikes) • plot(fit1$model) • plot(fit1, plot.conf=FALSE) • lines(fitted(fit1), col="red") • fit1$model • fit2 <- ses(strikes) • plot(fit2$model) • plot(fit2, plot.conf=FALSE) • lines(fit1$mean, col="red") • accuracy(fit1) • accuracy(fit2)

Comparing Holt and SES • Holt’s method will almost always have better in-sample RMSE because it is optimized over one additional parameter. • It may not be better on other measures. • You need to compare out-of-sample RMSE (using a test set) for the comparison to be useful. • Why don’t we do this? • …Because we don’t have enough data.

Exponential Trend Method • Holt’s linear trend method is… linear. • A multiplicative version of Holt’s method is:

Exponential Trend Method • In this method, lt denotes an estimate of the level of the series at time t. • bt denotes an estimate of the relative growth of the series at time t. • In R: holt(x, exponential=TRUE) • Unlike Holt vs. SES, comparing additive and multiplicative trend methods in-sample is ok because they have the same number of parameters to optimize.

Damped Trend Method • Gardner and McKenzie (1985) suggested that the trends should be “damped” to be more conservative for longer forecast horizons. • In addition to the two smoothing parameters, α and β*, there is a damping parameter φϵ (0,1). • φ dampens the trend so that it approaches a constant.

Damped Trend Method • If φ=1, this is the same as Holt’s method. • All three parameters, α, β*, and φ can be estimated/optimized by minimizing MSE. • Damped trend method often gives better forecasts than linear trend. • Forecasts converge to lT + φbT/(1-φ) as h→∞.

Multiplicative Damped Trend • Taylor (2003) introduced multiplicative damping. This is, generally, even more conservative than additive damping for longer-horizon forecasts. • If φ=1, you have the exponential trend method. • Forecasts converge to lT+ bTφ /(1-φ) as h→∞