Download

1 / 6

90 likes | 220 Views

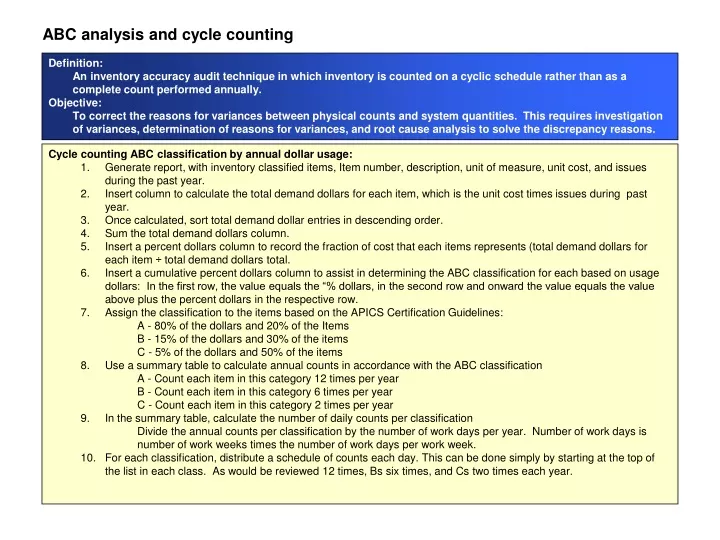

ABC analysis and cycle counting. Definition: An inventory accuracy audit technique in which inventory is counted on a cyclic schedule rather than as a complete count performed annually. Objective:

E N D

ABC analysis and cycle counting Definition: An inventory accuracy audit technique in which inventory is counted on a cyclic schedule rather than as a complete count performed annually. Objective: To correct the reasons for variances between physical counts and system quantities. This requires investigation of variances, determination of reasons for variances, and root cause analysis to solve the discrepancy reasons. • Cycle counting ABC classification by annual dollar usage: • Generate report, with inventory classified items, Item number, description, unit of measure, unit cost, and issues during the past year. • Insert column to calculate the total demand dollars for each item, which is the unit cost times issues during past year. • Once calculated, sort total demand dollar entries in descending order. • Sum the total demand dollars column. • Insert a percent dollars column to record the fraction of cost that each items represents (total demand dollars for each item ÷ total demand dollars total. • Insert a cumulative percent dollars column to assist in determining the ABC classification for each based on usage dollars: In the first row, the value equals the “% dollars, in the second row and onward the value equals the value above plus the percent dollars in the respective row. • Assign the classification to the items based on the APICS Certification Guidelines: • A - 80% of the dollars and 20% of the Items • B - 15% of the dollars and 30% of the items • C - 5% of the dollars and 50% of the items • Use a summary table to calculate annual counts in accordance with the ABC classification • A - Count each item in this category 12 times per year • B - Count each item in this category 6 times per year • C - Count each item in this category 2 times per year • In the summary table, calculate the number of daily counts per classification • Divide the annual counts per classification by the number of work days per year. Number of work days is number of work weeks times the number of work days per work week. • For each classification, distribute a schedule of counts each day. This can be done simply by starting at the top of the list in each class. As would be reviewed 12 times, Bs six times, and Cs two times each year.

Cycle counting process Objective: To provide the process for the Inventory analyst to follow for the conducting of cycle counting • The Inventory analyst generates the daily count list for cycle counters. This should be done efficiently by generating the daily counts for the entire month at one time. The analyst will need to add new items to the list each month and remove obsolete, so once per month is effective. • Cycle counter performs the count and reports the count quantity in the CMMS. Note that the cycle counters shouldn’t know what the system quantity is, so that the count is not biased. If any notes need to be communicated to the Inventory Analyst about the count, these should be entered into the system at the same time the count is entered. • Each morning, the inventory analyst gets an exception report that lists only those items for which the count and the system don’t match. • The inventory analyst calculates the count accuracy, which is system quantity less actual count ( “+”: system is over, “-” system is short). • Establish a tolerance guideline. The inventory analyst should review each item with variances, but a full investigation into the cause of the error is not mandated if it’s within the allowable tolerance. • A – 0% Tolerance • B – 2% Tolerance • C – 5% Tolerance • The inventory analyst might request a recount or perform an audit personally. Once the count is confirmed, the analyst updates the system to reflect the proper quantity. • The inventory analyst investigates the reasons for the errors, determines a corrective action, implements the corrective action if possible, or advises management of the recommendation to correct the error. • The inventory analyst records inventory accuracy each day by classification and in total. Management reports are generated once per month. • Advantages of cycle counting: • Timely correction of errors, which allows for more accurate inventory more often; errors are being corrected sooner avoiding the same issue with other items • Less elapsed time between cause and effect, therefore more likely to determine the cause(s) of the error(s) • Develop specialists in finding and fixing errors • Operations aren’t disrupted while count is being conducted, as they would likely be during a physical inventory

Cycle Count Template ABC classification by annual dollar usage: Cycle count Template (Sample to describe visually) ABC Classification: Available Days to Count:

Cycle Count Template ABC classification including criticality: This is important for maintenance items – some items are classified as critical to the mill operation and need tighter controls. Cycle count template -- ABC classification Including criticality: Need to choose the highest ABC from annual dollar usage and criticality. Count summary (assume above is representative of 10,000) items): Available days to count:

Perform count and compare to system quantity Cycle count example:

Cycle counting Investigation of errors: Once the inaccurate Items have been determined, the items to be investigated are listed on the cycle count evaluation table Cycle count evaluation table Error is what occurred to make cause the variance between the count and the system quantities. Reason for Error is the cause determined to be the root of the count variance. Corrective Action is the solution that would solve the reason for the error if it were put in place. Containment is a temporary measure put in place immediately to stop or minimize the cause of the error while waiting for the corrective action solution to be implemented. Status is used to state the progress towards a solution.