Download

1 / 1

10 likes | 181 Views

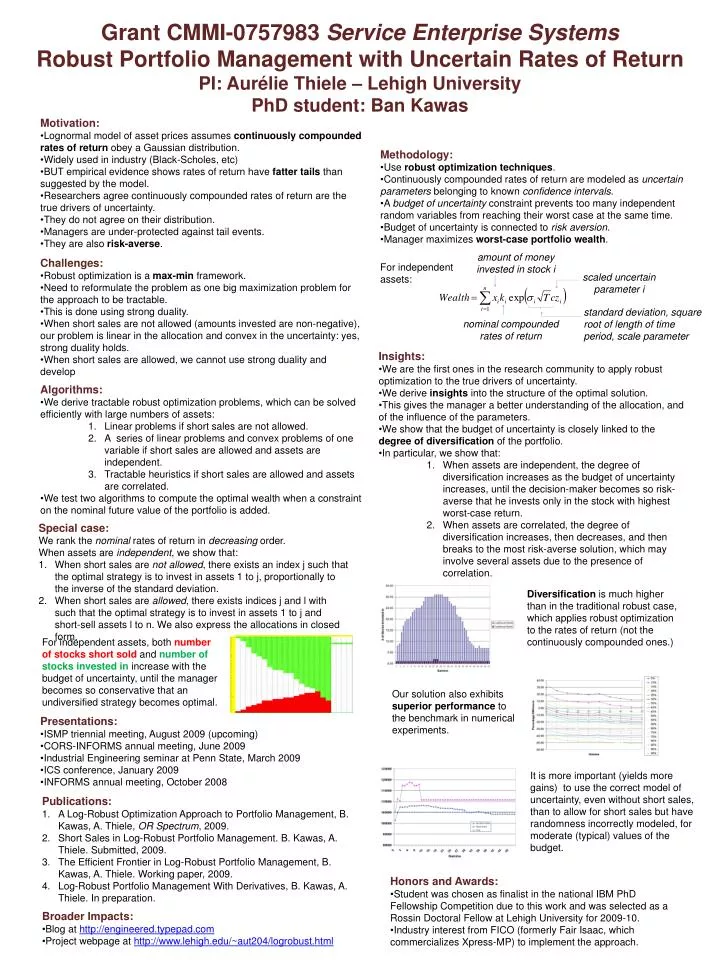

Motivation: Lognormal model of asset prices assumes continuously compounded rates of return obey a Gaussian distribution. Widely used in industry (Black-Scholes, etc) BUT empirical evidence shows rates of return have fatter tails than suggested by the model.

E N D

Motivation: • Lognormal model of asset prices assumes continuously compounded rates of return obey a Gaussian distribution. • Widely used in industry (Black-Scholes, etc) • BUT empirical evidence shows rates of return have fatter tails than suggested by the model. • Researchers agree continuously compounded rates of return are the true drivers of uncertainty. • They do not agree on their distribution. • Managers are under-protected against tail events. • They are also risk-averse. • Methodology: • Use robust optimization techniques. • Continuously compounded rates of return are modeled as uncertain parameters belonging to known confidence intervals. • A budget of uncertainty constraint prevents too many independent random variables from reaching their worst case at the same time. • Budget of uncertainty is connected to risk aversion. • Manager maximizes worst-case portfolio wealth. amount of money invested in stock i • Challenges: • Robust optimization is a max-min framework. • Need to reformulate the problem as one big maximization problem for the approach to be tractable. • This is done using strong duality. • When short sales are not allowed (amounts invested are non-negative), our problem is linear in the allocation and convex in the uncertainty: yes, strong duality holds. • When short sales are allowed, we cannot use strong duality and develop For independent assets: scaled uncertain parameter i Grant CMMI-0757983 Service Enterprise SystemsRobust Portfolio Management with Uncertain Rates of ReturnPI: Aurélie Thiele – Lehigh UniversityPhD student: Ban Kawas standard deviation, square root of length of time period, scale parameter nominal compounded rates of return • Insights: • We are the first ones in the research community to apply robust optimization to the true drivers of uncertainty. • We derive insights into the structure of the optimal solution. • This gives the manager a better understanding of the allocation, and of the influence of the parameters. • We show that the budget of uncertainty is closely linked to the degree of diversification of the portfolio. • In particular, we show that: • When assets are independent, the degree of diversification increases as the budget of uncertainty increases, until the decision-maker becomes so risk-averse that he invests only in the stock with highest worst-case return. • When assets are correlated, the degree of diversification increases, then decreases, and then breaks to the most risk-averse solution, which may involve several assets due to the presence of correlation. • Algorithms: • We derive tractable robust optimization problems, which can be solved efficiently with large numbers of assets: • Linear problems if short sales are not allowed. • A series of linear problems and convex problems of one variable if short sales are allowed and assets are independent. • Tractable heuristics if short sales are allowed and assets are correlated. • We test two algorithms to compute the optimal wealth when a constraint on the nominal future value of the portfolio is added. Special case: We rank the nominal rates of return in decreasing order. When assets are independent, we show that: When short sales are not allowed, there exists an index j such that the optimal strategy is to invest in assets 1 to j, proportionally to the inverse of the standard deviation. When short sales are allowed, there exists indices j and l with such that the optimal strategy is to invest in assets 1 to j and short-sell assets l to n. We also express the allocations in closed form. Diversification is much higher than in the traditional robust case, which applies robust optimization to the rates of return (not the continuously compounded ones.) For independent assets, both number of stocks short sold and number of stocks invested in increase with the budget of uncertainty, until the manager becomes so conservative that an undiversified strategy becomes optimal. Our solution also exhibits superior performance to the benchmark in numerical experiments. • Presentations: • ISMP triennial meeting, August 2009 (upcoming) • CORS-INFORMS annual meeting, June 2009 • Industrial Engineering seminar at Penn State, March 2009 • ICS conference, January 2009 • INFORMS annual meeting, October 2008 It is more important (yields more gains) to use the correct model of uncertainty, even without short sales, than to allow for short sales but have randomness incorrectly modeled, for moderate (typical) values of the budget. Publications: A Log-Robust Optimization Approach to Portfolio Management, B. Kawas, A. Thiele, OR Spectrum, 2009. Short Sales in Log-Robust Portfolio Management. B. Kawas, A. Thiele. Submitted, 2009. The Efficient Frontier in Log-Robust Portfolio Management, B. Kawas, A. Thiele. Working paper, 2009. Log-Robust Portfolio Management With Derivatives, B. Kawas, A. Thiele. In preparation. • Honors and Awards: • Student was chosen as finalist in the national IBM PhD Fellowship Competition due to this work and was selected as a Rossin Doctoral Fellow at Lehigh University for 2009-10. • Industry interest from FICO (formerly Fair Isaac, which commercializes Xpress-MP) to implement the approach. • Broader Impacts: • Blog at http://engineered.typepad.com • Project webpage at http://www.lehigh.edu/~aut204/logrobust.html