Download

1 / 10

110 likes | 208 Views

ABB robotics Cost Management Assignment. Process Analyzed. Group: JAMBO1 Federico Rosales Federico Tagliabue Jesper Jarnhall Panthep Pengniti Wyclife Amollo. ME2605 - Cost management and control. Cost Drive Structure.

E N D

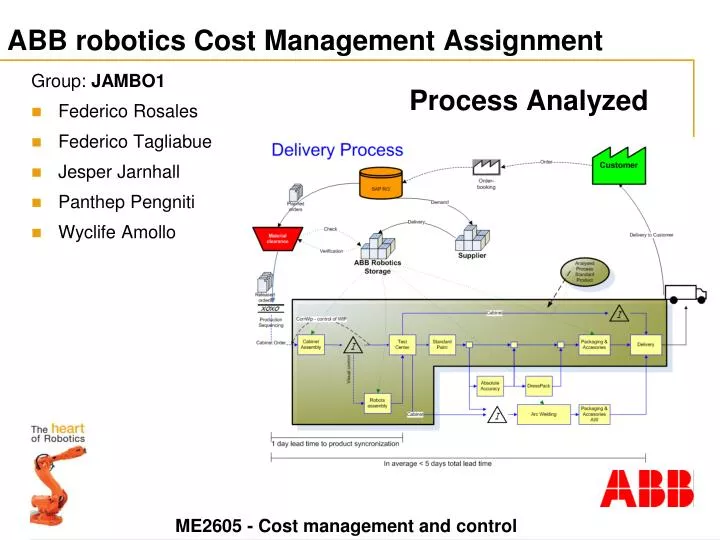

ABB robotics Cost Management Assignment Process Analyzed • Group: JAMBO1 • Federico Rosales • Federico Tagliabue • JesperJarnhall • PanthepPengniti • WyclifeAmollo ME2605 - Cost management and control

Cost Drive Structure *This analysis is based on cost assumptions and not on real costs. Also is assumed that ABB Robotics is using a traditional costing system. All the conclusion taken derive from these assumptions.

Traditional Cost System Cost analysis sheet

ABC system Adequacy of use at ABB • This methodology can potentially bring high benefits to ABB, since the nature of the company’s products implies that some of the service departments account for a high portion of the total costs. Some examples: • Purchasing: the differences in the complexity of the materials implies that they have to be managed diversely. Some materials are difficult to negotiate even if their proportional value in the product is not so high. This represents a great opportunity to apply ABC. • Customer service: most products encompass a post-sales service package (installation, maintenance, etc). These differences should be taken into account to trace down the costs in a more effective way • ABB is a huge company that relies strongly on Information Systems and therefore possesses the pre-requisites to track costs with a more detailed approach.

Mix model proposal • Identify Direct costs and directly allocate them to cost objects. • direct material, direct labour, direct energy used. • Identify easy assignable manufacturing Overhead Cost and allocate them to cost objects with the traditional method. • indirect material, facility expenses, indirect wages and supervision. • Rank the remaining manufacturing overhead costs by their total contribution. Potential Outcome of ranking Machinery expenses Logistic and distribution Management salaries Customer service Sales and marketing Purchasing General management

Mix model proposal (2) • Starting with the most important one select the appropriate cost drivers according to ABC model • Transaction, Duration or Intesity driver • The driver has to be chosen trading-off between its cost and benefit. Potential Outcome of ranking Machinery expenses Logistic and distribution Management salaries Customer service Sales and marketing Purchasing General management • Driver • Duration • Intensity • Intensity • Intensity • Duration • Transaction • Intensity • Allocation base • machine time used • weight and distance • Discretionary method • Average post-sales cost per product • Time spent per customer • number of purchase orders • Discretionary method Allocate both direct and overhead costs to the cost objects

Pricing • Since the company is a leader in Robotic industry, ABB is a price setter. ABB also provides products with premium quality and excellent service. However, ABB has also cannot sets price too high, or customers will move to competitors. • ABB also could use cost-plus approach compared with the market price.As long as the market price is higher than the cost-plus price they could price their products according to what the market is willing to pay. If the market price is lower they have to reduce costs or profit margin and always considering that they have cover all the costs occurred and gets appropriate profit to survive and satisfy stockholders.

Pricing (2) Transfer pricing • Transfer pricing is a methodology to price goods and services within a multi-divisional organisation. Transfer pricing has 3 main functions: • price setting for services or goods performed/produced by a division; • a mean to evaluate financial performance of a division; • determine the contribution to net income by profit centres in the organisation. • Born to shifting the profits in low taxes county to reduce overall taxes paid by multinational enterprises, transfer pricing is today used to determine profitability for the single divisions and to show the performance of each department in financial terms, since is not longer permitted use it for tax reduction due to the arm’s length principle introduced by tax authority. • In our situation, ABB Robotics Warehouse will sale materials to production departments. Cabinet and robotic departments will sell products to assembly department. The assembly department can either sell goods to testing department or buying service from it. The last holder will sell products to sale and marketing department. Other services departments can set prices for their services. • ABB Robotic is performing in a single location so the benefits from transfer pricing will be limited, since financial performance can be measure by accounting department too. There is also no benefit from taxes. Therefore, ABB Robotic has few reason to use transfer pricing and probably does not use it.

Budgeting • Based on our analysis we consider that the budgeting process which fits better the division that we observed is the bottom-up approach. The reasons for this are the following: • It is a manufacturing company that produces highly-complex products. This makes it virtually impossible to estimate the costs accurately from a level that is not directly linked to the production floor or production control. • Even if a top-down approach could be considered in manufacturing companies with highly standardized products this wouldn’t be the case. This plant receives orders that reflect the different needs of customers and thus call for some customization. This implies differences in costs that can only be assessed by the people that works at plant level. • Manual labour has a great importance in the process under consideration. This makes it difficult to establish very precise standards because there is always the intrinsic variation in manual processes. The best way to estimate costs accurately therefore is to have it done by the persons that have the best grasp of the situation and that is in the bottom levels.

Conclusion The conclusions of the analysis of the case considerd could be summarized as follows: • Costing system: • ABB Robotics should use a Mix model costing system with the benefits of both the traditional and ABC costing system. • Pricing: • The usual situation in competitive markets a cost-plus approach compared with the market price should be undertaken. • For innovative products (patent or high technology) ABB Robotics could act as the price setter. • For the current situation, the usage of a transfer pricing system would not add enough value compared to the cost and the complexity that will be introduced. • Budgeting process: • Due to the cost structure deriving from complex products, need for customization and variation in manual processes a bottom-up approach for budgeting is preferred. This guarantees a better accuracy in allocation of recourses and costs.