Download

1 / 11

E N D

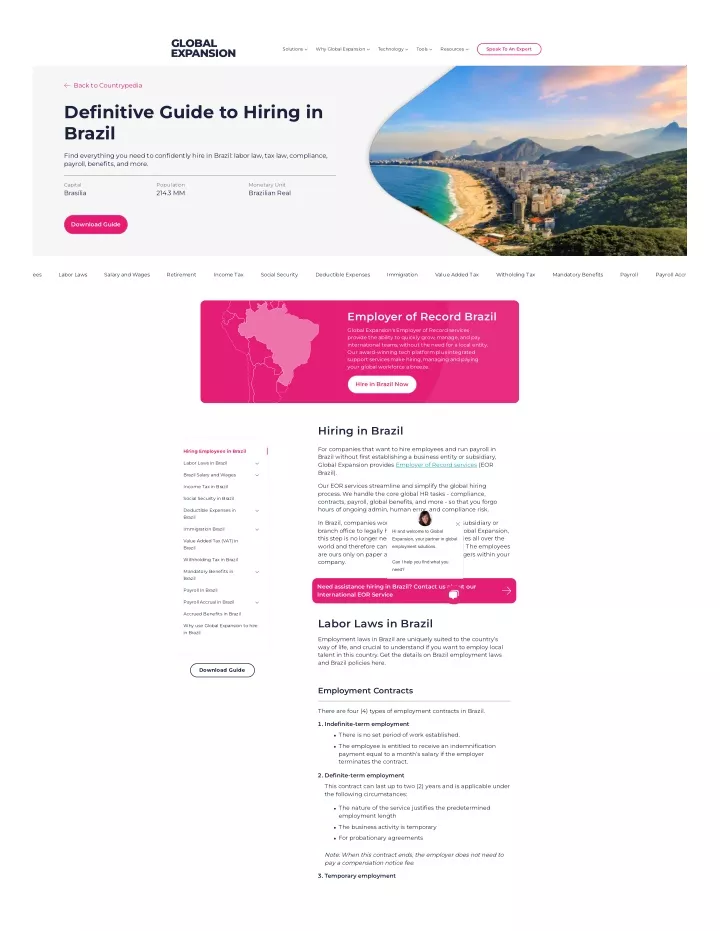

Solutions Why Global Expansion Technology Tools Resources Speak To An Expert Back to Countrypedia Definitive Guide to Hiring in Brazil Find everything you need to confidently hire in Brazil: labor law, tax law, compliance, payroll, benefits, and more. Capital Brasília Population 214.3 MM Monetary Unit Brazilian Real Download Guide Payroll Accr ees Labor Laws Salary and Wages Retirement Income Tax Social Security Deductible Expenses Immigration Value Added Tax Witholding Tax Mandatory Benefits Payroll Employer of Record Brazil Global Expansion's Employer of Record services provide the ability to quickly grow, manage, and pay international teams, without the need for a local entity. Our award-winning tech platform plus integrated support services make hiring, managing and paying your global workforce a breeze. Hire in Brazil Now Hiring in Brazil For companies that want to hire employees and run payroll in Brazil without first establishing a business entity or subsidiary, Global Expansion provides Employer of Record services (EOR Brazil). Hiring Employees in Brazil Labor Laws in Brazil Brazil Salary and Wages Our EOR services streamline and simplify the global hiring process. We handle the core global HR tasks - compliance, contracts, payroll, global benefits, and more - so that you forgo hours of ongoing admin, human error, and compliance risk. Income Tax in Brazil Social Security in Brazil Deductible Expenses in Brazil In Brazil, companies would historically establish a subsidiary or branch office to legally hire in that country. With Global Expansion, this step is no longer necessary. We have subsidiaries all over the world and therefore can legally hire on your behalf. The employees are ours only on paper and report directly to managers within your company. Can I help you find what you need? Immigration Brazil Hi and welcome to Global Expansion, your partner in global Value Added Tax (VAT) in Brazil employment solutions. Withholding Tax in Brazil Mandatory Benefits in Brazil Need assistance hiring in Brazil? Contact us about our International EOR Service Payroll In Brazil Payroll Accrual in Brazil Accrued Benefits in Brazil Labor Laws in Brazil Why use Global Expansion to hire in Brazil Employment laws in Brazil are uniquely suited to the country’s way of life, and crucial to understand if you want to employ local talent in this country. Get the details on Brazil employment laws and Brazil policies here. Download Guide Employment Contracts There are four (4) types of employment contracts in Brazil. ?. Inde?nite-term employment There is no set period of work established. The employee is entitled to receive an indemnification payment equal to a month’s salary if the employer terminates the contract. ?. De?nite-term employment This contract can last up to two (2) years and is applicable under the following circumstances: The nature of the service justifies the predetermined employment length The business activity is temporary For probationary agreements Note: When this contract ends, the employer does not need to pay a compensation notice fee. ?. Temporary employment

This kind of contract is used for particular types of work, such as maternity leave coverage, seasonal work, or other extended leave periods. ?. Intermittent employment This contract does not include a fixed salary. This contract is provided for someone with an irregular and ad-hoc working schedule. The employee is paid on an hourly basis. Employee Probation Period The maximum probationary period allowed in Brazil is 90 days (two terms of 45 days). If the initial trial period is 45 days, it may be renewed but only for an additional term of 45 days. Annual Leave in Brazil Professionals in Brazil are entitled to 30 calendar days of vacation per year after every 12 months of service, plus 1/3 of their monthly salary as a vacation bonus. The vacation period is typically taken in one block (or split between 20 days and 10 days). Holidays in Brazil Workers are entitled to paid holidays during Festival (public and religious) holidays. These include memorial holidays and religious holidays (Christian origin). Here is the full list of public holidays in Brazil: 1st January New Year’s Day 10th April Good Friday 13th April Easter Monday 21st April ‘Tiradentes’ Day 1st May Labor Day / May Day 7th September Independence Day 12th October Our Lady Aparecida / Children’s Day 2nd November All Souls Day 15th November Republic Proclamation Day 25th December Christmas Day Get started now Maternity Leave Brazil Women are entitled to 4 months of fully paid maternity leave and may not be dismissed during pregnancy or during the 12 months after birth. An extension can be granted by a maximum of 4 weeks on medical grounds (2 weeks prior and 2 weeks after birth). Leave lasts from 28 days before and 91 days after the expected date of childbirth and is paid by the Social Security Institute. Paternity Leave Brazil Men are entitled to 5 days of paid paternity leave, which they must request in advance. Other than this, a 2016 law provides for 15 days of paid paternity leave for workers of companies enrolled in a Corporate Citizenship Program. Sick Leave in Brazil If an employee is sick and provides a medical note, the first 15 days of absence must be paid. Any further days off are paid through the National Institute of Social Security (INSS), at fixed rates.

Thereafter, benefits must continue to be paid until work is resumed or employment is ended. Working Hours in Brazil According to the Brazil Labor Law, a typical workweek in Brazil is 44 hours, ideally eight (8) hours per day (plus one hour for lunch) and four (4) hours on Saturday. Though permitted, overtime is only allowed two (2) hours a day. Companies can choose to have longer work days during the week and remain closed on Saturday.Hours worked on night shifts must be paid at an additional 20% premium. Overtime in Brazil The law prohibits shifts over 10 hours per day, so only 2 overtime hours are allowed for a regular working day. The hours that exceed the workday must be paid with a minimum additional of 50 percent (100 percent on Sundays or holidays). This rate can be increased under the collective labor agreements. Termination of Employment in Brazil Employees can be dismissed without cause at any time, subject to notice periods and severance pay. The employer is not required to formally justify the dismissal, except in the case of termination with cause. Employees are entitled to resign on the basis of constructive dismissal if: They are assigned to tasks outside the scope of the services for which they were hired or that are immoral or illegal. They are treated immorally or without respect by the employer. The employer does not respect their main employment rights. They suffer physical abuse or damage to their (or their family members') honor or reputation, among other circumstances. An employer can dismiss an employee with cause in certain circumstances such as gross misconduct, dereliction of duties, improper act or lack of self-restraint. Notice Period in Brazil Either party may terminate the employment contract by giving written notice known as aviso prévio of 30 days or payment in lieu of working the notice period. After one year of service, the employee is entitled to 3 additional ‘days’ notice per completed year of service until 60 days are added, thereby making the total possible prior notice period equivalent to 90 days Severance in Brazil Employees terminated without cause or constructive dismissal are entitled to receive: The balance of their wages. A proportional payment for untaken holidays, plus one-third of the holiday remuneration. A proportional 13th month salary (Christmas bonus). Access to the funds deposited in a severance fund called the Brazilian Government Severance Indemnity Fund Law (FGTS). - The FGTS contains monthly deposits of 8% of an employee’s gross compensation. - Deposits are made by the employer into an escrow account with a governmental bank, in the name of the employee. - The employer must also pay a 40% penalty on the balance in the account. Any payments due under collective agreements. Any other benefit provided under the employer’s policies or the employment contract. Employees terminated with cause receive only the balance of their wages, an unused holiday payment and a proportional 13th month salary. Employees that resign are entitled to all funds that are due in the case of a termination without cause (see above), except for the FGTS penalty and the indemnification for not having received the advance notice period. Brazil Salary and Wages Average Salary

The average salary in Brazil for an employee is roughly 8,560 Brazilian Real (BRL) per month. Wages in Brazil vary between different careers. The average salary in Brazil includes housing, transport, and other benefits. Health Care and Medical professions pay the most (631,656 BRL). Start your Global Expansion Brazil Salary Ranges Brazil minimum wage The minimum salary in Brazil is 2,170 BRL monthly, or about $421.27. Median wage The median salary is 8,220 BRL per month, or about $1,588.10. The median represents the country’s middle-wage value. Maximum average wage Brazil’s maximum average wage is around 38,200 BRL per month, or $7380.22. This figure is not the actual maximum salary in Brazil, but rather the highest average wage recorded. Brazil Salary Ranges Visualized Minimum wage 2,170 BRL 8,200 BRL Median wage Maximum average wage 38,200 BRL Brazil Salary Comparison Those with 2-5 years of experience earn 32% more than those fresh out of college or junior employees. Those with 10 or more years of experience have a salary increment of 21%, while workers who cross the 15-year mark get an additional 14%. Workers with a higher education degree get paid more for skills and knowledge. Those with a bachelor’s degree earn 24% more than those who only attained a certificate or diploma. Meanwhile, workers with a Ph.D. make 23% more than those with a Master’s degree, even if they do the same job. On average, male employees in Brazil make 10% more reais than female employees in all industries. 13th Month Salary in Brazil A 13th-month salary is required in Brazil and is an amount equal to one month’s salary which is paid out to employees in two parts in November and December. The prorated 13th-month salary is also due upon termination. Income Tax in Brazil Brazilian residents are taxed on worldwide income. Nonresidents are taxed on Brazilian-source income only. Under Brazilian law, source is defined according to the place where the payer is located, regardless of where the services are provided. Therefore, income paid by a Brazilian entity is considered a local source, while income paid abroad is considered foreign source. Individuals are considered to be tax residents from the moment of arriving in Brazil if any of the following conditions are satisfied: They are involved in a local labor relationship. They hold a residence permit based on a statutory representative status. They hold a residence permit based on an investor status. Other foreign nationals are taxed as nonresidents if they satisfy all the following conditions: They hold other types of temporary visas. They are not involved in a local labor relationship. They do not stay in Brazil for more than 183 days (consecutive or nonconsecutive) during any 12-month period.

A foreign national who remains in Brazil for longer than 183 days is subject to tax on his or her worldwide income at the progressive rates applicable to residents. Taxable employment income generally includes wages, salaries, and any other type of remuneration and benefits received by an employee from an employer. Federal income tax is levied on taxable income. Under Normative Instruction #1558/2015, the following tax rates apply to monthly taxable income. Deductible Amount (BRL) Monthly taxable income Rate (%) Not Exceeding (BRL) Exceeding (BRL) 0 1,903.98 0 0 1,903.98 2,826.65 142.80 7.5 2,826.65 3,751.05 354.80 15 3,751.05 4,664.68 636.13 22.5 4,664.68 - 869.36 27.5 Deductible Amount (BRL) Monthly taxable income Rate Exceeding (BRL) Not Exceeding (BRL) 0 22,847.76 0 0 22,847.76 33,919.80 1,713.58 7.5 33,919.80 45,012.60 4,257.57 15 45,012.60 55,976.16 7,633.51 22.5 55,976.16 - 10,432.32 27.5 Hire anyone, anywhere Social Security in Brazil All employees, self-employed individuals, and employers in Brazil are required to make contributions to the social security system. Contribution rates range from 7.5% to 14 percent, depending on the amount of the compensation. There is a cap to the individual contribution, which represents a percent applied upon the maximum contribution income (R$ 7,087.22 per month) as of 2022, thus resulting in a maximum R$828.38 contribution for the employee. The employer contribution usually ranges from 26.8% to 28.8% (20 percent is allocated to the National Social Security Institute, or INSS, and up to 8.8% to other social security taxes), depending on the type of activity, calculated on each employee's monthly salary. There is no cap on the employer's contribution. Ceiling Contribution (BRL) Social Security Rate (%) Contribution Salary From (BRL) Up to (BRL) 0 1,100 7.5 - 1,100 2,203.48 9 - 2,203.48 3,305.22 12 - 3,305.22 6,433.57 14 828.38 Social security contributions due by the employer ranges from 26.8 percent to 28.8 percent (20 percent are allocated to the National Social Security Institute, or INSS, and up to 8.8 percent to other social security taxes), depending on the type of activity, calculated on each employee's monthly salary. There is no cap to the employer's contribution. Private pension plans are optional in Brazil. An individual is able to subscribe directly within an authorized financial institution or via an employer-sponsored plan. In addition to the referred social security contribution, additional social charges are due by the employer, whose rate will depend on its economic activities. Social security payable by self-employed individuals may be 5%, 11%, or 20% of the ceiling contribution salary, depending

on specific conditions of the individual and of the services rendered. Social Security Contribution Contribution Self Employed 5% to 20% Employee 8% to 11% Employer 20% to 22.5% We take care of everything Deductible Expenses in Brazil Personal Deductions Brazil’s tax system allows for a number of personal deductions. For Brazilian tax legislation purposes, the following items can be deducted from an employee's annual taxable income: Dependents (a specific amount per dependent is established each year by the tax authorities). Alimony payments, in Brazil or abroad, provided some requirements are met. Tuition expenses, in Brazil or abroad, are limited to a certain specific amount established each year by the tax authorities (applicable to the taxpayer and dependents per year). Medical expenses (e.g. hospital, psychologists, dentists), in Brazil or abroad, are deductible (when not reimbursed), with no limits. Payments for medical insurance located outside Brazil are not deductible. Brazilian official social security contributions made by the individual. Private pension contributions (if the entity is located in Brazil) made by the beneficiary and for one’s dependents, limited to 12% of gross taxable income. Cut down on your onboarding time The taxpayer may also deduct from the tax due, and not from the calculation base, the following: Donations made to official government, state, and/or municipal child care entities and elderly fund, through a municipal fund. Certain qualified contributions/investments to cultural, audio- visual, and sports projects. Note, however, that the above deductions are limited to 6% of the tax due. Contributions made by the taxpayer to the official social security system on behalf of registered domestic employees (e.g. maids, house cleaners, drivers), within certain limits. Contribution to health programs related to cancer and mentally handicapped support (for example, Pronon, the National Support Program for Oncology Care and Pronas/PCD, the National Support Program for Health Care for People with Disabilities ), limited to 1% of the income tax during the calendar year, considering each program. Standard Deductions In lieu of the above itemized deductions, taxpayers may take the benefit of a standard annual deduction (20% of gross taxable income, limited to a certain specific amount established each year by the tax authorities). The option for a standard deduction is not allowed on exit returns or for those individuals who will offset losses from farming activities in the annual income tax return. Business Deductions Individuals who receive income from work without an employment relationship may deduct the following from the income received: Payments made to third parties, provided they have an employment relationship and the respective payroll charges. Expenses necessary to produce the business’ revenue. Investments and expenses to maintain the business Immigration Brazil Learn about immigration requirements in Brazil, work visa requirements, work permits and more.

Need assistance hiring in Brazil? Contact us about our International EOR Service Temporary work permits and process A temporary work permit is designed for immigrants who have an interest in establishing residence in Brazil. Some temporary work permits may be renewable for an additional equivalent period. To obtain temporary work permits for their expatriate employees, employers must apply for authorization from the Ministry of Justice and National Security. The process and documents required depend on the type of work permit: ?) Temporary technical work permit based on Normative Resolution 03. This is for a service contract between a Brazilian company and a foreign company. The contractor in Brazil initiates the procedure by applying to the Immigration Division of the Ministry of Justice and National Security. If the application is approved, the authorization is forwarded through the Ministry of Foreign Affairs to a designated Brazilian consulate abroad, where the individual designated in the service contract requests the issuance of the visa in the passport. To obtain a temporary technical work permit under a service contract, the immigrant individual and the company must provide certain documents and information, including the technical service agreement between the companies. ?) Temporary work permit based on Normative Resolution 02. For expatriate employees of Brazilian companies under local work contracts. To obtain a temporary work permit based on a labor contract with a Brazilian company, the individual must file proof of education and professional experience in addition to the passport. The employer in Brazil must also file certain documents with the Ministry of Justice and National Security, together with an employment contract. Residency visa / residence permit Immigrants may obtain a residency visa in Brazil as an investor to be able to be self-employed in the country. To obtain this type of residence permit, both of the following conditions must be satisfied: The immigrant must make a minimum investment, which is currently BRL500,000 if certain requirements are met, and register the investment at the Central Bank of Brazil. This limit may be reduced to BRL150,000 if certain requirements are met. The investor must present a plan of investment and a commitment to create work positions for Brazilian nationals. Visa requirements Brazil overview Learn about the visa policy in Brazil and all the ways to obtain a regular or a work visa for Brazil. VITEM V visa (Temporary work visa) Documentation Valid Passport Photo 2x2 inches Completed Application Form Proof of residence in consular jurisdiction Employment contract Validity: 2 years Eligibility Foreign citizens traveling to Brazil under an employment contract or to perform technical assistance/emergency work must hold a temporary work visa (VITEM V). Permanent Brazil work visa (“Visto Permanente”) Investor Visa Brazil Get started now

Value Added Tax (VAT) in Brazil Brazil’s VAT can be confusing: each of the 26 states and the Federal District set their own indirect tax rates, which range between 17% and 19%. Some examples of the ICMS standard rate are as follows: São Paulo, Paraná e Minas Gerais 18% Rio de Janeiro 19% Remaining States: 17% Rates of IPI range from 0 to 330%, and average around 15%. ISS standard rate ranges from 2% to 5%. The following rates are those applied generally across most states apart from Rio de Janeiro, São Paulo, and Paraná e Minas Gerais Value Added Tax 7% Reduced Rate 17% 12% Standard Rate Reduced Rate Withholding Tax in Brazil In general, payments made to non-residents are subject to withholding tax (WHT) in Brazil. As a general rule, payments to non-residents for services rendered to Brazilian residents and payments to non-resident individuals as work compensation are subject to the general WHT at a 25% rate. However, interest, royalties and other fees that are not paid in connection to the provision of services are taxed at a 15% rate. Brazilian dividends paid to nonresidents are exempt from withholding tax. The WHT shall also be levied at a 15% rate over the provision of technical services, administrative assistance and other similar services, which do not involve transfer of technology. Note that payments made to entities located at low tax jurisdictions are subject to the WHT at a 25% rate. Tax treaties may reduce or eliminate WHT. Other taxes may be imposed on the local source of payment depending on the nature of the transaction. Withholding Tax 25% Payment made to non-residents 15% Payment made to non-residents 15% Payment made to non-residents 15% Payment made to non-residents Exempt Payment made to non-residents Mandatory Benefits in Brazil

It’s important to understand the legal requirements of hiring employees in Brazil (whether it’s remote or in-office) so that your business remains compliant. As part of Global Expansion’s International PEO and Employer of Record (EOR) solution, we guarantee employees are registered with the appropriate government agency, and that they receive mandatory benefits such as minimum wage, workers’ compensation and paid time off (PTO). Additionally, all tax deductions associated with the employee are processed at the source, meaning our in-country entity will be responsible for paying all taxes to the authorities on behalf of the new hire. These are mandatory benefits as postulated by law These include probationary period, annual leave, public holidays, sick leave, maternity leave, paternity leave, overtime pay, notice period, severance pay and 13th month pay Mandatory benefits also include social security benefits. Hire anyone, anywhere Mandatory Bene?ts overview Probationary period Annual Leave Public Holidays Sick Leave Maternity Leave Paternity Leave Overtime Pay 13th month pay Notice period Severance Pay Social Security Benefits Payroll In Brazil Payroll in Brazil is typically on a bi-weekly or monthly cycle. Employees can expect to receive a paycheck on the 15th or 30th of the month. Here’s what you need to know to run payroll in Brazil. The Brazilian tax year is the calendar year. Brazil imposes a pay-as-you-earn (PAYE) system. Under the PAYE system, income tax on income received by an individual through a foreign payroll should be paid on a monthly basis through a tax voucher known as carnê-leão. In addition, for the portion of the compensation paid through a Brazilian payroll, taxpayers are subject to withholding income tax. The tax is due on the last working day of the month following the month when the income is received. Late payments are subject to penalties (at a daily rate of 0.33%, limited to 20%) and to interest (at a monthly rate of approximately 1%). To make monthly income tax payments, residents must register as individual income tax contributors and obtain a Taxpayer Identification Number (CPF). Disclosure of the CPF number is mandatory in most financial transactions. Married persons may be taxed jointly on all types of income if one spouse has no income and is listed as a dependent in the other spouse’s return. In all other cases, married persons are taxed separately on all types of income Global Expansion’s EOR and international PEO solution can help you run payroll in Brazil with ease. In just a few clicks, your employees will be onboarded and enrolled into our payroll system. Additionally, we can invoice for clients locally, meaning we can enroll any new hire quickly and efficiently, whether they're an expatriate or a local national. Payroll Accrual in Brazil Country Accruals Additional Information 1% INSS Social Security 0.01%

Christmas Bonus 0.01% 0.01% Vacations Christmas Bonus over Vacations 0.01% Cut down on your onboarding time Description INSS is responsible for collecting contributions to maintain the Brazilian Social Security regime operating: paying retirements, pensions due to death, illness, disability, aids, and other benefits foreseen by law. Both employers and employees pay social security contributions. These contributions are used to fund government pensions paid to retired citizens. Individuals who receive compensation from a Brazilian source are subject to the local social security tax, which is withheld by the employer or the source of income. Contribution rates range from 8 percent to 11 percent, depending on the amount of the compensation. There is a cap to the individual contribution, which represents 11 percent applied upon the maximum contribution income (R$ 5,531.31 per month) as of January 2017, thus resulting in a maximum R$608.44 of contribution for the employee. The employer contribution usually ranges from 26.8 percent to 28.8 percent (20 percent are allocated to the National Social Security Institute, or INSS, and up to 8.8 percent to other social security taxes), depending on the type of activity, calculated on each employee's monthly salary. There is no cap to the employer's contribution. Payroll Accruals Additional Information Annual Leave Maternity Leave Paternity Leave Sick Leave Overtime Severance 13th Month Pay Social Security Accrued Benefits in Brazil Christmas Bonus % It is based on 50% of the salary of December 4.16% 0% Christmas Bonus Over Vacations % Severance per Year% After one year of service, 8% of an employee's gross salary is put in an Escrow that will contribute to their severance pay 8% Vacations % Professionals in Brazil are entitled to 30 calendar days of vacation per year after each 12 months of service (8.24% of annual salary) 8.24% Of annual salary Notice % Employees are entitled to 30 days of notice period for one year of service or more 8.24% Christmas Bonus Over Notifications % 0% Vacations Plus % It is based on 50% of the salary of the month 4.16%

Total percentage of Salary (yearly) 32.8% The total employment accruals as a percentage of salary per annum Why use Global Expansion to hire in Brazil Establishing a branch office or subsidiary in Brazil can be time- consuming, expensive and complex. With such a robust labor market in place, one must pay great attention to detail when structuring employment because Brazilian labor laws are complex. The company also has a responsibility to comply with specific employment practices dictated by Brazilian law to maintain its good standing as an equal opportunity employer. Global Expansion makes it easy for you to expand into Brazil. We'll help you hire your candidate of choice, handle HR matters and payroll, and ensure that you comply with local laws without the burden of setting up a foreign branch office or subsidiary. In addition, you'll have complete control and direction over your employees. We enable you to stay in control of everything. Our Brazilian Global Professional Employer Organization (PEO) and Employer of Record (EOR) solution provides you with peace of mind to focus on running your company and the security to enter new markets. Ready to hire anywhere in the world? Grow your team the right way with Global Expansion. Request a Proposal Contact Solutions Why Global Expansion Tools United States Employer of Record How we’re different CountryPedia United Kingdom Employment Compliance About GX Global Hiring Guides Follow 5,013 Portugal Global Immigration Total Cost of Employment Calculator Technology France Global Taxes GX One Philippines Global Payroll Resources Equity Pro Articles Singapore Employee Benefits Data Security & Privacy Blog Contact Us Global HR Thought Leadership Global PEO Become a Partner FAQ © 2022 Global Expansion | Privacy Policy | Cookie Policy | Code of Conduct Policy | Responsibility Policy | Anti-Bribery and Corruption Policy