Download

1 / 33

330 likes | 342 Views

Rail Value for Money Study. Railway Study Association 7 March 2012. Sir Roy McNulty Chair, RVfM Study. Contents. The RVfM Study – Findings and Recommendations Things that surprised me Things the Report didn’t say Progress since the Report was issued Making Change happen.

E N D

Rail Value for Money Study Railway Study Association 7 March 2012 Sir Roy McNulty Chair, RVfM Study

Contents • The RVfM Study – Findings and Recommendations • Things that surprised me • Things the Report didn’t say • Progress since the Report was issued • Making Change happen

Terms of Reference 1. To examine the overall cost structure of all elements of the railway sector and to identify options for improving value for money to passengers and the taxpayer while continuing to expand capacity as necessary and drive up passenger satisfaction. 2. In particular, to examine: • what legal, operational and cultural barriers stand in the way of efficiency improvements; • the incentives across different parts of the rail industry to generate greater efficiency; • the role of new technology, processes and working practices in fostering greater efficiency; • ways of generating more revenue, e.g. car parking, gating at stations, better utilisation of property; and • to make recommendations. 3. The study will examine the whole industry costs and revenues and their composition. In doing so, it will look at comparable industries in the UK and abroad.

In many ways GB Rail has performed well • Increasing customer satisfaction • High levels of operational performance/punctuality • Continued improvement in safety • Significant investment • Important contributions to decarbonisation, and to the economy • Sustained growth – passenger and freight

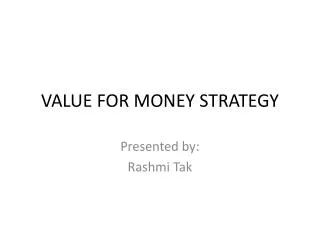

Figure 2.1: Change in network length (route-km), passenger-km and journeys, 1948-2009

And GB rail has major opportunities for the future • Prospect of doubling current levels of traffic by 2030 • But NOT if railway economics remain as they are • GB rail has to earn its “licence to grow”

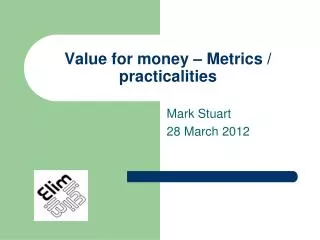

Figure 2.3: Industry expenditure per passenger-km(2009/10 prices)

Table 2.3: Impact on industry costs of “should cost” exercise (2008/09 prices) On this basis, the efficiency gap is 20 – 30%

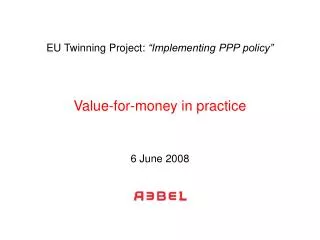

International benchmarking • Benchmarking GB rail against France, Netherlands, Switzerland and Sweden, based on 2009 data

Figure 2.10: Comparison of whole system costs (partly normalised)£/k passenger-km

Findings on Costs and Revenues • Unit costs of the GB passenger railway have not improved since the mid 1990’s • The study’s desk analysis suggested that GB rail should cost 20-30% less than it did in 2008/09 • Benchmarking against four European comparators indicates an efficiency gap of some 40% • Some of the difference between 20-30% and the 40% is due to difference in train utilisation, some of which may be systemic The result of GB Rail’s higher costs is that GB Passengers and Taxpayers are each paying at least 30% more than their counterparts elsewhere GB Rail should aim for a 30% reduction in unit costs by 2018/19

Barriers to Efficiency • Fragmentation – Structures and Interfaces • The ways in which the main players have operated • Roles of Government and industry • Incentives/Franchising • Fares structures • Legal and contractual framework • Supply chain management • Limitations on whole-system approaches • Relationships and culture The basic principles of the UK approach do not need to be changed, but there is a need for improved Collaboration and Alignment Some of the issues apply to UK Infrastructure generally

Barriers to Efficiency - Conclusions • Not a cause for despair • we need a thorough understanding of the causes of excessive costs • these barriers can be overcome, with strong leadership and concerted effort by all • nothing to be gained from “blame games” or “inquests” • Not a simple set of problems; no “silver bullet” • The problems get solved if everyone contributes

Principal Recommendations(1) Creating an Enabling Environment

Creating an Enabling Environment • Leadership from the top • Clearer Objectives • More Devolved Decision-making • Changes to Structures and Interfaces • More Effective Incentives (particularly in Franchising) • Changes to Regulation

Principal Recommendations(2) Delivering greater efficiencies

Delivering Greater Efficiencies • Asset Management • Programme and Project Management • Supply Chain Management • Safety, Standards and Innovation • HR Management • Information Systems • Rolling Stock • Lower cost Regional railways

(3) Driving implementation • Learn the lessonsfrom the past • Rail Delivery Group to take a lead • Small independentchange team

Things that surprised me • Good GB Rail Performance (other than costs) • Scale and complexity of operations and projects • Organisations and people committed to “the railway” • Organisations and people ready for change • Extent of Government involvement • Lack of clear Focus on Costs • Lack of clarity as to what the Subsidy is buying

Things the Report didn’t say • The UK got it wrong • the basic principles of the UK approach are sound • privatised/liberalised/competitive • clear separation of roles (track/train, franchises etc) • clear accountability • strong independent regulation • transparency of costs • but in addition, there is a need for better Alignment and Co-operation, particularly at Industry and Route levels, and between Customers and Suppliers • and we need an environment which encourages/enables a clear focus on Costs and Value for Money.

Things the Report didn’t say (cont’d) • Sweep away the whole complicated structure and start again, instead of trying to make what we’ve got work better • in an industry as big and complex as GB Rail, no structure is going to be simple and easy to operate • even more importantly, no other conceivable structure is likely to yield sufficient additional savings to compensate for the 5-7 years delay, which major reorganisation would involve, in addressing the areas where savings can clearly be made • passengers and taxpayers want their burdens eased NOW

Progress since the Report was issued • Rail Delivery Group • formation/composition • programme of work • asset, programme and supply chain management • contractual relationships • train utilisation • technology and innovation • Rail systems Agency • Initial Industry Plan • commitment from those involved • interaction with Government and ORR

Progress since the Report was issued (cont’d) • Network Rail • devolution to Routes • new ways of working with suppliers • external benchmarking and competition • behaviour safety programme • asset condition systems • all this on top of existing commitments • Train operators • review of rolling stock procurement and management • new Franchises

Progress since the Report was issued (cont’d) • Network Rail and Train Operators • support for Rail Delivery Group • alliancing • Initial Industry Plan • DfT • changes to franchising • Command Paper • ORR • expanded role • capability review • Areas where more progress is needed

Why major change on this scale is achievable • The barriers and solutions are well understood; • Easier in an environment of growth; • Significant changes are already in progress; • Many people in the industry ready for change; • The industry can provide the vision, leadership and energy to make change happen; and • We have a Secretary of State who is determined to see this happen.

Making Change Happen • A Framework for Change • Recognising the need for change • Creating and communicating a new vision • Empowering people to act on the vision • Institutionalising change • Key Ingredients • Vision • Leadership • Energy • Relationships • Structures

Rail Value for Money Study Rail Study Association 7 March 2012 Sir Roy McNulty Chair, RVfM Study