Download

1 / 16

160 likes | 265 Views

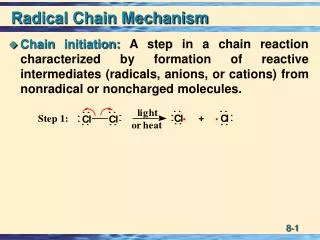

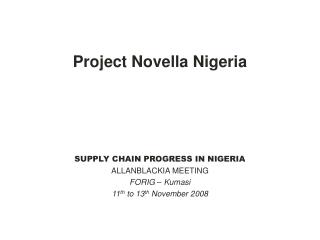

Putting Value Back in the Value Chain Iowa’s Value Chain Partnerships Project Rich Pirog – Associate Director Leopold Center. The Music Industry: decentralized to centralized and back again. 1890. Individual Musicians. 1945. Independent Record Labels. 2000. Big Five. 2001. Napster.

E N D

Putting Value Back in the Value Chain Iowa’s Value Chain Partnerships Project Rich Pirog – Associate Director Leopold Center

The Music Industry: decentralized to centralized and back again 1890 Individual Musicians 1945 Independent Record Labels 2000 Big Five 2001 Napster 2006 P2P CENTRALIZED DECENTRALIZED From: the Starfish and the Spider: The Power of Leaderless Organizations

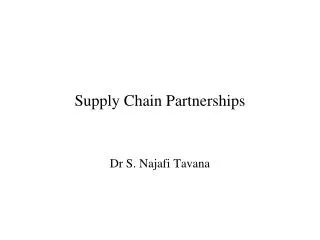

The Food Industry (System) 1880 Local farms –local markets Larger farms –Regional & national markets 1945 1990 Local food movement 2000 Five global retailers – huge farms 2015 Networked local food – scaled up CENTRALIZED DECENTRALIZED

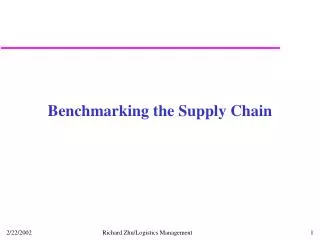

Supply Chain Approach to Developing Regional Food Businesses • Technical assistance: R&D • Transportation & logistics • Transaction costs • Business/quality management • Product traceability • Technical assistance: R&D • Processing innovation • Co-location, transaction costs, • Business/ quality management Access to capital Capitalization strategies • Technical assistance: R&D • Production & Transaction costs • Business planning & structure • Marketing • Certification • Consumer market research • Food safety and health • Product and market authenticity • Transaction costs • Business/quality management Access to capital Capitalization strategies Farmers Distributors Markets (consumers) Processors Focused beginning farmer programs New business models with farmers, processors, and markets ( trade channels) Policy & Market incentives Access to capital Capitalization strategies Policy & Market Incentives Policy and Market Incentives • What must be present • Community and state support and incentives to start and grow businesses • Collaborative research and development • Coordination of loan opportunities and technical assistance • Culture of collaboration across funders, NGOs, universities, state agencies, and • private sector – synchronized Farmers (direct market and farmer networks) Processors (local, regional, and national) Distributors (existing and new infrastructures) Markets (food service, retail, wholesale, direct)

Technical and financial assistance Hierarchical, Centralized, SiloedDifficult for businesses to negotiate consultants NGOs Community level ??? Cooperatives Sustainable ag centers Private sector

Value Chain Partners foster value chains that provide economic, social, and ecological benefits to Iowa farmers, communities, and landscapes. Regional Foods Pork Niche Communities of Practice Small Meat Processing Fruits and Vegetables

Why is Value Chain Partnerships (VCP) different? A network orientation(Forces for Good; L.R. Crutchfield and H.M. Grant 2008)

How we are differentVCP communities of practice function as: • Catalysts for cooperationof diverse interests to create solutions for producers and businesses; • Hubswhich create, capture, document, leverage knowledge, and deploy this knowledge as technical assistance; • Magnetsto attract funding and for leveraging, channeling, and distributing funding; • Scouts to identify emerging opportunities with high potential to deliver economic benefits

County-Based Regions – RFSWG 2008 Just pledged $30,000 year for 5 years Northeast Iowa Food and Farm Coalition South West Iowa Farm and Food Initiative Hometown Harvest of SE Iowa Northwest Iowa Regional Local Foods System Northern Iowa Food and Farm Partnership Marshall County

What we’ve done • Supported more than 60 projects to address challenges across the chain and in communities • Raised more than $2.5 million since 2002 • Involved 60-70 (farm or community-based) companies, consultants, organizations, and communities (Iowa and neighboring states) • Started the MBA with minor in sustainable agriculture option at ISU • Accelerated R&D, marketing, and networking efforts in building value-based value chains (niche pork company cooperation)

Value Chain Partners – “Knights of the Foodtable” Future Serves as a hub for many groups (state and regional level) All groups support the important work at the local level Good Food Network Upper Midwest National Good Food Network eXtension NC SARE * Groups such as food policy council, farm-based energy, financial assistance, hunger

Turning the Flywheel (in the Social Sectors): Implications for building Good Food farmer networks, buyers, TA providers-researchers • Attract Believers • Time • Money Relentless focus on what you are good at, and what drives the resource engine • Build Strength • First Who…then what • Sustainable networks • Build Brand • Emotion (heart) • Reputation • Demonstrate Results • Mission Success • Trend Lines (Indicators) Adapted from Good to Great and the Social Sectors – Jim Collins

www.valuechains.org • Rich Pirog E-mail: rspirog@iastate.edu Regional Food Systems Working Group