Download

1 / 29

300 likes | 1.05k Views

Bank Reconciliation Statement. Dr.Mukku Syam Babu Lecturer in Commerce, Government Degree College, Razole , East Godavari Dist. Introduction. Generally most of Business firms open current account with the bank to conduct business transactions through cheques .

E N D

Bank Reconciliation Statement Dr.MukkuSyamBabu Lecturer in Commerce, Government Degree College, Razole, East Godavari Dist.

Introduction • Generally most of Business firms open current account with the bank to conduct business transactions through cheques. • The bank supplies a pass book or a statement which shows the firms’ transactions with the bank.

Pass Book • The pass book/ Bank Statement is the Xerox copy of the business firm’s ledger account maintained by the bank.

Cash Book • On the other hand, the business firm records these transactions with the bank either in the bank account opened in the ledger or in the bank column of its cash book. • It is maintained by the firm.

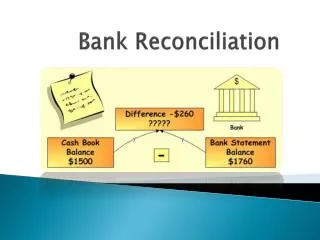

Pass Book VS Cash Book • On any day, the pass book and the cash book must show the same bank balance, because both books are governed by the same set of transactions, • Although the nature of the balances will be different. • .

If cash book shows a debit balance, passbook shows a credit balance and vice-versa. • Deposited cash or cheques are debited in cash book and credited in pass book.

Similarly cheques drawn on the bank are credited in cash book but the banker debited them in the pass book.

Favorable Balance • if cash book shows a debit balance, then the pass book shows a credit balance which is known as favorable balance.

Unfavorable Balance • if cash book shows a credit balance and pass book will show a debit balance which is known as unfavorable balance.

Disagree of Balances • In practice, Bank Balance as per CB & PB do not agree on same day, because some of the entries might not been recorded or incorrectly recorded in any of these two books.

Therefore, it is desirable for the business firm to check periodically the entries in the pass book with the entries in the bank column of the cash book.

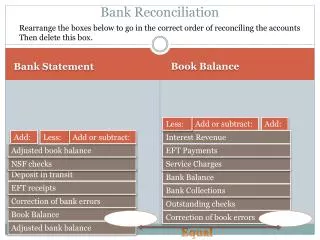

Bank Reconciliation Statement • The statement, which is prepared with a view to reconcile the two balances on a particular date, is called Bank Reconciliation Statement.

Reasons for differences between Bank balances as per CB & PB • Cheques issued but not yet presented for payment. • Cheques deposited for collection but not yet collected.

BRS from Businessmen point • of View

Reasons for differences between Bank balances as per CB & PB • Direct payments by the customers into the bank. • Insurance premium or any expenses paid by the bank. • Interest on investment received by the bank.

Reasons for differences between Bank balances as per CB & PB • Dividend on shares collected by the bank; • Interest allowed by the bank • Interest on overdraft charged by the bank; • Bank charges charged by the bank;

Reasons for differences between Bank balances as per CB & PB • Rebate on bills retired under rebate through the bank but full amount entered in the cash book • Dishonored cheques-bills entered in Pass Book only

Reasons for differences between Bank balances as per CB & PB • Any wrong entry on credit side of the passbook or Cash Book; • Any wrong entry on debit side of the passbook or Cash Book;

Steps in the preparation of Bank Reconciliation Statement • Take the cash book or passbook balance as a starting point. • If the starting point denotes a favorable balance as per cash book or passbook, take it as a positive figure.

Steps in the preparation of Bank Reconciliation Statement • However, if the starting point denotes negative unfavorable balance, take it as a negative figure.

Steps in the preparation of Bank Reconciliation Statement • Adjust the starting point amount as per the information given and analyze its impact on other balances