Download

1 / 23

1.35k likes | 3.05k Views

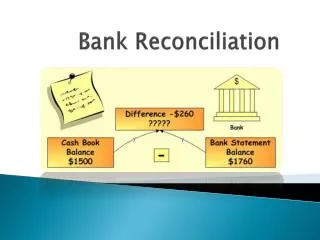

Here we have considered the Difference between the Bank balance as per Cash Book & the Pass book by preparation of the Bank Statement. The reasons of differences & importance of finding the variation is discussed.

E N D

BANK RECONCILIATION STATEMENT Takshila Learning Learn anything anywhere Visit: http://www.takshilalearning.com Call: +91-8800999280

Meaning & Concept Statement prepared by the Business entity, Reconciling/Matching the bank balance as per the cash book(Bank Column) & the Pass book. find out the differences between the balances & nullify them BRS is prepared by the business entity

Cash V/s Pass Book The Cash Book is prepared by the business entity Pass book/Bank Statement is prepared by the bank to have a record of the customer’s banking transactions.

BRS • BRS is not the part of the Accounting process/financial statements. • It is prepared at a particular date as a part of cash book • not mandatory to be prepared, voluntary for matching the balances of both books

Importance Bring out errors in Cash book/Pass book Detection of Undue delay by the bank Discourages any manipulation by Accountant Finding out actual position of bank balance

Reasons of Differences • Timing differences : Differences due to different treatments in Cash & Pass book. (on different dates) • Other differences : Difference due to errors in Cash book.

Examples of Timing Differences Cheque deposited but not cleared Cheque issued but not presented for payment Bank Charges/Interest debited/credited in bank account. Direct payment/receipt by bank

Other Differences • Transaction not recorded/twice recorded in cash book. • Any other clerical mistake( wrong amount, wrong casting, etc) in cash book.

Balances Cash Book • Debit : Favourable/Positive Balance • Credit : Unfavorable/Negative/Overdraft Pass Book • Debit : Unfavorable/Overdraft/Negative • Credit : Positive/Favourable

Techniques of reconciliation • Without Adjusted Cash Book ( all changes are done in BRS ) • With Adjusted Cash Book (the errors of cash book are rectified in adjusted Cash book & the timing differences in BRS from the rectified cash balance) Note : Adjustments done in Adjusted Cash book not to be again treated in BRS.

BRS- Basic Idea • While preparing BRS, the changes (cancellation of the differences) are: • to be done in the book from which we have started • Keeping in mind the treatment done of the same transaction in the other book.

Illustration If the Debit balance as per Cash book (as on 31/12/14) is ` 65,000 • Cheque of `15,000 was deposited in bank but not cleared. • A cheque of `12,000 was issued but not presented for payment. • Bank charges of `150 was debited. • Bank interest of `1600 was credited to the account. • A dividend of `2,000 was received by the bank from ABC company.

MCQs Q.1. A Bank Reconciliation Statement is prepared to know the causes for the difference between:

MCQs Q.2. Debit Balance as per Cash Book: ` 2,000, Cheques deposited but not cleared: ` 100, Cheques issued but not presented: ` 150, Bank allowed interest: ` 50, Bank collected dividend ` 50. Balance as per Pass Book will be:

MCQs Q.3. Under bank reconciliation statement, while adjusting the cash book

MCQs Q.4. While preparing BRS, Starting with over draft balance of cash book, a cheque of ` 5,500 deposited in bank and duly credited in pass book, but not recorded in cash book ____ in B.R.S

MCQs Q.5. Bank Overdraft as per Cash Book is ` 10,500 Interest debited by bank ` 3,500 for which advice was not received by account holder. Cheques deposited but not credited by bank ` 7,500. Cheques issued but not yet presented ` 9,500. What is the Overdraft amount as per pass book?

MCQs Q.6. When preparing a Bank Reconciliation Statement if you start with balance as per Pass Book, then cheques paid by bank recorded twice in Pass Book ` 1050 will be

MCQs Q.7. When money is withdraw from bank ,the bank

MCQs Q.8. The total payment side of Cash book is Rs. 700 short , if Bank Reconciliation statement is started with passbook (overdraft )balance then

MCQs Q.9. Mr. Y presented three cheques of Rs.3000,Rs.4500 and Rs.3600 with the bank on 28th March 2005. Out of these cheques amounting to Rs.4500and Rs.3000 were shown in the pass book in the month of April 2005. while reconciling the balance on 31-03-2005 which of these cheques would be taken in reconciliation

MCQs Q.10. overdraft as per Pass book is given Rs. 10,000 Cheques deposited in bank but not recorded in cash book Rs. 100 Cheque drawn not presented for payment Rs. 6,000 Bank charges recorded twice in Cash book Rs. 30 Overdraft as per cash book will be