Download

1 / 13

140 likes | 400 Views

Bank Reconciliation. ACCN 1 - Accounting. Starter for 10…. Write 3 questions regarding anything topics we have studied so far this year…. Write the answers for the questions……..

E N D

Bank Reconciliation ACCN 1 - Accounting

Starter for 10….. • Write 3 questions regarding anything topics we have studied so far this year…. • Write the answers for the questions…….. • (try to think of questions that challenge your deeper knowledge and not just one word answers – Use Bloom’s Question Stems to help you) • Next Activity will be to quiz someone to see who can stay in the HOT SEAT… If they answer your questions correctly, they stay in the middle. If they are incorrect, you swap places… The WINNER is the person who remains in the middle at the end of the quiz. • TODAY’S WINNER – Oshane • Can you write 3 questions for next Tuesday to try and become the HotSeat reigning champion?

Learning Objective: • To verify the accuracy of the double-entry through the preparation of the bank reconciliation statement. • E grade – reconcile the cash book with the bank statement • C grade – To create a Bank Reconciliation statement • A grade - explain why bank reconciliations are prepared

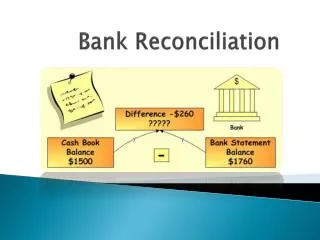

Completing entries in the Cash Book • A Business will record funds paid into & out of the bank in to the Cash Book • The Bank will also record funds paid into & out of the business bank account and issue a Bank Statement • The balances should be the same • What might cause the two balances to be different? In pairs, make a list.

Possible answers… • Time delay between receiving cheque and paying in to the bank • Time delay between paying into bank and it being ‘cleared’ • Bank interest & charges paid (shown on statement) • Standing order not shown in Cash book until actually paid • Direct Debits not shown in Cash book until actually paid • Customers pay accounts direct to bank

Cash Book v Banks Statement So what are the differences? What does this say you should sensibly do when balancing-off the Cash Book at the end of the accounting period?

Key Terms • UnpresentedCheques – Cheques that have been drawn (written), entered in the cash book BUT have not yet been presented to the bank • Outstanding (uncleared) lodgements – bank deposits that have been recorded in the cash book but haven’t yet been processed by the bank • Direct Debit – authority granted by a business to allow a 3rd party to request payments directly from the bank account. • Standing Order – Fixed/Regular interval payment automatically paid on the instruction of the BUSINESS

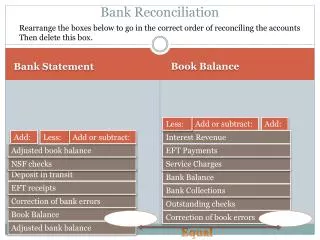

Preparing the Bank Reconciliation Statement • Tick all items that appear on the bank statement AND the Cash Book • Enter in to Cash Book any items missing that are on the bank statement • Balance the cash book (bank columns) & c/d closing balance • Start Bank Reconciliation Statement with the closing ‘balance as per the cash book’ • Unticked payments (CR) in the cash book - unpresentedcheques • Unticked receipts (DR) in the cash book – outstanding lodgements • Calculate the closing balance on the bank reconciliation statement

Bank Statement What is different about this statement when you compare it to the CASH BOOK?

Exam Questions…… • In the text book it shows how to update the cash book by adding the missing entries BEFORE you balance off • In the exam………? • What if they DON’T give you the cash book but just tell you what the Balance b/d is? • How would you process this?

Creating a Bank Reconciliation Statement Bank Reconciliation Statements as at (Date) £ Balance as per cash book xxx ADDUnpresentedChequesxxx xxx LESS Bank lodgement not on statement (xxx) Balance as per Bank Statement xxx

Using a Bank Overdraft • If the closing balance of the Cash Book shows an ‘Overdraft’ how does this effect the way that the Bank Reconciliation Statement is drawn up? • DEDUCT the unpresentedcheques • ADD outstanding lodgements • WHY?? • In order to show the correct amount in the bank account. If you had £200 overdraft and you added £100 of unpresentedcheques you would have £300 as the overdraft total. IN REALITY – unpresentedcheques means you have more money than you thought and therefore the overdraft is REDUCED. • £200 - £100 unpresentedcheques = £100 overdraft

Importance of the Bank Reconciliation Statement • Allows for identification of errors in cash book – own errors • Allows for identification of processing errors by bank • Account for missing entries • Identify FRAUD or act as deterrent • Out of date Cheques can be cancelled (over 6 months)