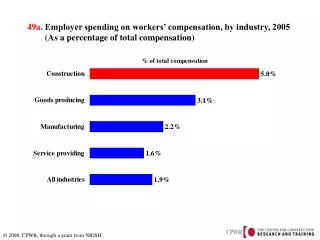

Download

1 / 47

480 likes | 493 Views

Awareness Programme on Ind AS. Topics. Overview of Ind AS Convergence Process Roadmap for implementation of Ind AS Carve-outs made in Ind AS. Overview of Ind AS. Background. Need for International Financial Reporting Standards?. Key Terms - IFRS.

E N D

Topics • Overview of Ind AS • Convergence Process • Roadmap for implementation of Ind AS • Carve-outs made in Ind AS

Background • Need for International Financial Reporting Standards?

Key Terms - IFRS IASB : International Accounting Standards Board (formerly IASC) IASC : International Accounting Standards Committee (now IASB) IFRIC : International Financial Reporting Interpretation Committee SIC : Standard Interpretations Committee (now IFRIC) IFRS : International Financial Reporting Standards (formerly IAS) IAS : International Accounting Standards (now IFRS) FASB: Financial Accounting Standards Board in the US IFAC : International Federation of Accountants

Key Terms - IFRS International Financial Reporting Standards (IFRSs)are Standards and Interpretations issued by the International Accounting Standards Board (IASB). They comprise: (a) International Financial Reporting Standards (developed by the IASB); (b) International Accounting Standards (developed by the IASC); (c) IFRIC Interpretations (developed by the IFRIC Committee); and (d) SIC Interpretations (developed by the SIC Committee).

Key Terms – Ind AS MCA : Ministry of Corporate Affairs NACAS : National Advisory Committee on Accounting Standards ASB : Accounting Standard Board of ICAI Ind AS : Indian Accounting Standards AS : Accounting Standards Indian GAAP : Indian Generally Accepted Accounting Principles

Adoption vs Convergence IFRS adoption: A country adopting IFRS is implementing IFRS into its legislation in exact form as issued by IASB. IFRS convergence: A country converging to IFRS cooperates with IASB to mutually develop compatible accounting and financial reporting standards (i.e. with few carve outs). These carve outs have been made to fill up the gap/differences in application of Accounting Principles Practices and economic conditions prevailing in the country of implementation.

Key Carve Outs IndAS 1 (Presentation of Financial Statements) and Ind AS 10 (Event after the Reporting Period) In case of long term loan arrangement, for breach of material provision on or before the end of reporting period, with the effect that the liability becomes payable on demand on the reporting date. Any waiver or rectification of such breach subsequent to year end before the approval of the financial statements for issue are considered as adjusting event and continues to classify as non-current labilities. Under IFRS, it is considered as non-adjusting event.

Key Carve Outs 2. IndAS 17 (Leases) The straight lining of lease rentals under operating lease arrangements may not be required in cases where periodic rent escalation is due to inflation. IFRS does not provide an exception to straight lining of lease rentals where rent escalation is due to inflation.

Key Carve Outs 3. Ind AS 18 (Revenue) IFRIC 15 on Agreement for Construction of Real Estate prescribes that construction of real estate should be treated as sale of goods and revenue should be recognised when the entity has transferred significant risks and rewards of ownership and retained neither continuing managerial involvement nor effective control. IFRIC 15 has not been included in Ind AS 18. Instead, a footnote has been given specifying that the Guidance Note on the subject being issued by the Institute of Chartered Accountants of India shall be followed.

Key Carve Outs 4. Ind AS 21 (The Effects of Changes in Foreign Exchange Rates) IndAS provides an option to continue with the policy adopted for accounting for exchange differences arising from the translation of long-term foreign currency monetary items recognized in the financial statements for the period ending immediately before the beginning of the first Ind AS financial reporting period as per the previous GAAP.

Key Carve Outs 5. Ind AS 28 (Investment on Associate and Joint Ventures) Uniform accounting policies may not be used by the investors of an associate in case it is impracticable under Ind AS. This carve out has been made because the investor does not have ‘control’ over the associate.

Key Carve Outs 6. Ind AS 28 (Investment on Associate and Joint Ventures) On the lines of Ind AS 103, Business Combinations, to transfer excess of the investor’s share of the net fair value of the investee’s identifiable assets and liabilities over the cost of investment in capital reserve whereas in IFRS (IAS 28), it is recognisedin profit or loss.

Key Carve Outs 7. Ind AS 32 (Financial Instruments : Presentation) IndAS states that where the exercise price for the conversion of the FCCB (Foreign currency convertible bonds) is fixed, irrespective of any currency, it is to be classified as equity rather than as an embedded derivative. IFRS on the other hand, requires that where the conversion of bond into equity shares is fixed, but the exercise price for such conversion is defined in currency other than the functional currency of the entity, the conversion aspect is to be accounted as embedded derivative.

Key Carve Outs 8. Ind AS 40 (Investment Property) Alternative option to value Investment Property subsequently at each reporting date on fair value is not allowed instead it will be valued only at cost.

Key Carve Outs 9. Ind AS 101 (First-time Adoption of Ind AS) Allowing the use of carrying cost of Property, Plant and Equipment (PPE) on the date of transition in accordance with existing GAAP as its deemed cost instead of retrospective application of IAS 16 or fair value.

Key Carve Outs 10. Ind AS 103 (Business Combinations) IndAS 103 requires bargain purchase gain arising on business combinationto be recognized as other comprehensive income and accumulated in equity as capital reserve, unless there is no clear evidence for classifying the business combination as a bargain purchase. In this case, it is to be recognized directly in equity as capital reserve. IFRS 3 requires the same to be recognized in profit or loss.

Convergence Road Map For companies other than banking companies, insurance companies and non-banking finance companies, implementation of Ind AS is as follows: On voluntary basis: • For accounting periods beginning on or after 1 April 2015, with the comparatives for the periods ending 31 March 2015 or thereafter. On mandatory basis • For accounting periods beginning on or after 1 April 2016, with comparatives for the periods ending 31 March 2016, or thereafter, for: • all companies having net worth of Rs. 500 cror more. • holding, subsidiary, joint venture or associate companies of the above companies.

Convergence Road Map On mandatory basis (cont.) • For accounting periods beginning on or after 1 April 2017, with comparatives for the periods ending 31 March 2017, or thereafter, for: • companies whose equity and/or debt securities are listed or are in the process of being listed on any stock exchange in India or outside India and having net worth of less than Rs. 500 cr • unlisted companies having net worth of Rs. 250 cr or more (less than Rs. 500 cr) • holding, subsidiary, joint venture or associate companies of the above class of companies.

Convergence Road Map The net worth shall be calculated in accordance with the stand-alone financial statements of the company as on 31st March, 2014 or the first audited financial statements for accounting period which ends after that date. Once Ind AS are applied voluntary or mandatorily it is irrevocable and not require to prepare another set of financials as per AS. Application is for both standalone as well as consolidated financial statements if threshold criteria met.

Convergence Road Map Scheduled Commercial Banks, (excluding RRBs), Insurers/Insurance Companies and Non-Banking Finance Companies (NBFCs), will start in phase manner from the accounting period beginning 1 April 2018. Urban Co-operative Banks (UCBs) and Regional Rural Banks (RRBs) shall not be required to apply Ind AS and shall continue to comply with the existing standards for time being.

Steps • Check the period of applicability as per Road Map • Identify GAAP differences • Ascertain implication on financial reporting, business process, IT, tax, etc. • Project planning • Implementation i.e. Transition to Ind AS as per Ind AS 101: First-time Adoption of Indian Accounting Standards • Post implementation review (continuous process)

Objective of Ind AS101 The objective of Ind AS 101is to ensure that an entity’s first Ind AS financial statements, and its interim financial reports for part of the period covered by those financial statements, contain high quality information that: • is transparent and comparable over all periods presented • provides a suitable starting point for accounting under Indian Accounting Standards (Ind AS) • can be generated at a cost that does not exceed the benefits to users

Illustration - Ind AS Adoption Timeline • Entity will produce its first Ind AS statements ending on 31/03/2017 which is at least two years after the date of transition to Ind AS (01/04/2015) • Entity will have one year of full comparative information • The opening statement of balance sheet is prepared 'as at' the date of transition to Ind AS (01/04/2015) but using Standards effective at the first Ind AS reporting date (i.e. 31/03/2017).

Recognition and Measurement • The Starting Point: • An entity shall prepare an opening Ind AS balance sheet at the date of transition to Ind AS. • Accounting Policies: • Same accounting polices at opening and throughout all period presented with exceptions. • Other standards: • Not to apply different version of other standards that were effective at earlier dates. • May apply a new Ind AS that is not yet mandatory if that Ind AS permits early application • Subject to the exceptions and exemptions listed in Ind AS 101, transitional provisions in other Standards do not apply.

Recognition and Measurement - contd. • Opening balance sheet: An entity shall, in its opening Ind AS balance sheet: • recognise all assets and liabilities whose recognition is required by Ind AS • not recognise items as assets or liabilities if the Standards do not permit such recognition • reclassify items that it recognised under previous GAAP as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity under Ind AS • apply Ind AS in measuring all recognised assets and liabilities • Adjustments • The adjustments resulting between the accounting policies that an entity uses in its opening Ind AS and those used under its previous GAAP shall be recognised directly in retained earnings (or, if appropriate, another category of equity) at the date of transition to Ind AS.

Exceptions / Exemptions Exception to the retrospective application to other Ind AS: Mandatory Voluntary

Presentation and Disclosure Components and reconciliations to be presented in first Ind AS financial statements along-with notes, say for 31 March 2017.

Questions? Thank You! akhilkanthalia@gmail.com