Download

1 / 13

140 likes | 322 Views

Financial Ratios. Financial Ratios. Ratio Analysis: Ratio analysis addresses issues such as a firm’s liquidity, use of leverage, asset management, cost control, profitability, growth, and valuation. Can be compared to competitors (especially industry leaders)

E N D

Financial Ratios • Ratio Analysis: • Ratio analysis addresses issues such as a firm’s liquidity, use of leverage, asset management, cost control, profitability, growth, and valuation. • Can be compared to competitors (especially industry leaders) • Can be compared over time (trend analysis)

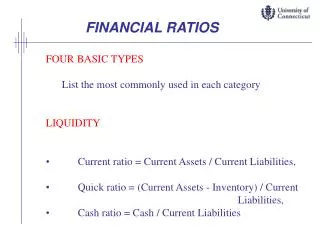

Liquidity Ratios • The relationship of a firm’s liquid assets to current liabilities • Used to provide information about a firm’s short term ability to pay obligations via: • Current Ratio(working capital ratio): • Current assets / current liabilities • The most common measure of short-term solvency • Working Capital • Current assets – current liabilities

Leverage Ratios • Measure of a firm’s use of debt to finance assets and operations • Solvency • A firm’s financial ability to survive in the long term by paying its long-term obligations

Leverage Ratios • Debt to Total Assets: • Total liabilities / total assets • Measures the percentage of funds provided by creditors • Creditors prefer this ratio to be low as a cushion against losses • Equity to Total Assets(financial leverage index): • Return on common equity / return on assets • When the ratio exceeds 1 the ratio is favorable and the use of financial leverage is successful

Profitability Ratios • Measure earnings relative to some base, i.e. productive assets, sales, or capital • Used by investors, creditors, and others to evaluate management’s stewardship of the firm’s assets

Profitability Ratios • Gross Profit Percentage: • (Net sales – Cost of Sales) / net sales • Measures the percentage of profit that is derived from the sale of goods • A high gross margin implies effective cost control • Profit Margin: • Net Income / net sales • Measures the amount of profit from each dollar of sales, after all operating expenses

Profitability Ratios • Return of Equity: • Net income available to common shareholders / their average equity • Measures the income earned on each dollar of investment by stockholders

Asset Management Ratios • Measures the firm’s use of assets to generate revenue and income • Relates to liquidity

Asset Management Ratios • Receivable Turnover: • Sales / average accounts receivable • Measures the efficiency of accounts receivable collection • High-turnover is preferable • Inventory Turnover: • Cost of sales / average inventory • High-turnover implies that the firm does not hold unproductive inventories or obsolete goods

Growth Ratios • Measure the change in the economic status of a firm over a period of years • Compared against competitors, as well as, the economy as a whole • Earnings per share (EPS): • Net income available to common shareholders • Measures the amount of net income earned on each share of common stock

Valuation Ratios • Broad performance measures that reflect the basic principle that corporate management’s ultimate goal is to maximize shareholder value • Price-Earnings Ratio (P-E ratio): • Market price per share of common stock / EPS • Measures investors assessment of a company’s future earnings

Limitations of Ratio Analysis • Although ratio analysis is a useful tool for evaluating the efficiency of operations and the stability of financial conditions, be weary of its limitations: • Different ratios for different industries • Inflation • Management’s desire to make financials look good • Sources of information