Download

1 / 26

280 likes | 486 Views

FINANCIAL RATIOS. FOUR BASIC TYPES List the most commonly used in each category LIQUIDITY Current ratio = Current Assets / Current Liabilities, Quick ratio = (Current Assets - Inventory) / Current Liabilities, Cash ratio = Cash / Current Liabilities. MANAGEMENT SKILL

E N D

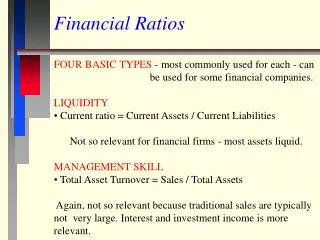

FINANCIAL RATIOS • FOUR BASIC TYPES • List the most commonly used in each category • LIQUIDITY • Current ratio = Current Assets / Current Liabilities, • Quick ratio = (Current Assets - Inventory) / Current Liabilities, • Cash ratio = Cash / Current Liabilities

MANAGEMENT SKILL • Total Asset Turnover = Sales / Total Assets, • Fixed Asset Turnover = Sales / Fixed Assets • Inventory Turnover = Sales / Inventory • Working Capital Turnover = Sales / (Accounts Receivable + Inventory) • Capital Spending Rate = Capital Spending / Sales,

PROFITABILITY • Return on Equity = Net Income/Equity • Return on Assets = Net Income/Assets or • EBIT/Assets, • Operating profit margin = Operating Profit/Sales, • Net Profit Margin = Net Income/Sales,

FINANCIAL RISK • Debt to Equity = Debt / Equity, • Debt Ratio = Debt / Assets • Debt / Capital where Capital = Long-Term Debt + • Equity • Times Interest Earned = Net Operating Income / • Interest Expense

DUPONT ANALYSIS - ANALYZING ROE ROE = (Net Income/Pretax Income) x (Pretax Income/EBIT) x (EBIT/Sales)x (Sales/Total Assets) x (Total Assets/Equity) = (Tax Burden) x (Interest Burden) x (Return on Sales) x (Total Asset Turnover)x (Financial Leverage) Note that to get the net effect of debt on ROE we use (interest burden) x (financial leverage)

THE RELATIONSHIP BETWEEN ROE AND ROA • ROE • = (1 - tax rate)[ROA + (ROA - Interest rate)Debt / Equity] • IMPICATIONS • High debt firms have positive leverage on ROE as • long as their ROA exceeds the interest rate paid on debt, otherwise, debt creates negative leverage. • This negative leverage effect is what drove many high debt firms into bankruptcy in the recession. • Example of Ratio Analysis using Reuters.com

In the next section we will discuss some of the ways companies may manipulate their accounting to mislead investors.

GENERALLY ACCEPTED ACCOUNTING PRINCIPALS (GAAP) • BASIC PREMISES • Going Concern • Historical Costs - reduce judgment • Consistency - similar transactions treated similarly • Matching - match cost with cost-caused revenues • Conservatism - when uncertain, report lowest figure • for income or assets. • Disclose Fully - all relevant information.

QUALITY OF EARNINGS NO GENERALLY ACCEPTED DEFINITION FASB definition: normal, recurring, cash flow generating earnings from operations, reflecting the need to replace depreciating assets.

SIMPLE, OUTWARD INDICATORS OF QUALITY • Choice of conservative policy when a liberal • alternative is available. (see Summary of • Accounting Policies in financial statements) • Stable policies (look for frequent changes reported • in footnotes) • Stable earnings relative to the industry (gimmicks • eventually run out and earnings drop). • Stable dividends - same as above • Stable debt levels through time.

No large changes in “Other Accounts” • Simple and clear financial reports with few • footnotes and comments. • Short bland audit report long, wordy ones • mentioning material uncertainties mean trouble. • Check date - reports dated later than usual mean • accountants / management disagree. • Check auditors reputation unknown accounting firm • may mean trouble

CATEGORIZING GIMMICKS - 3 BASIC WAYS • REPORTED INCOME = REVENUES - EXPENSES + (TAX BENEFIT) • REALIZE REVENUES FASTER / SLOWER • should be booked when high probability of • payment but managers have some discretion. • REALIZE COSTS SLOWER / FASTER -SAME • some avoid proper write-offs • TAX RELATED - increase / decrease expenses • for tax books but not for financial statements to shareholders. - lower taxes - higher income.

WHY MIGHT MANAGERS WANT TO REDUCE REPORTED INCOME? • Keep reserve to cover mistakes made in the future • New CEO takes a bath - blames earlier CEO - sets • up good results in future - Daimler Benz (conversely, retiring CEO may artificially boost earnings in his last year to look good) • Incentive compensation paid only to some • maximum of earnings or ROE • Transfer some earnings to next year when bonus • may increase.

REVENUE GIMMICKS BY RECOGNITION METHOD installment - book earnings when paid - offer discounts for fast payment shipping - book earnings at shipment - ship faster production method - when produced - produce faster completed contract and percent completed contract- when contract (or %) completed - speed completion Such manipulation shows up in increases in accounts receivable and inventories.

BOGUS REVENUE • Grossing up – Priceline resells tickets and counts the full price as their revenue even though they don’t buy the ticket from the airline until it is sold. • Exchanges of overvalued products – side agreement to buy at high price if seller buys from you at high price – cell phone companies buy each others unused lines. • Exchange of same product at higher prices to boost end consumers’ sale price – electric companies sold each other the same electricity, boosting price each time and then sold to customers who pay based upon average price of electricity sold. • Lend a customer the money to buy your product when there is little chance the customer will repay.

SELL PRODUCT TO UNCONSOLIDATED SUBSIDIARY AT INFLATED PRICES Sell receivables to subsidiary to cover bad credit sales and late payment. Usually, 50% ownership in subsidiary requires consolidation so this does not have an effect for consolidated subsidiaries. But if subsidiaries is judged to be very different than parent then consolidation is not required e.g., Ford , GM, GE, finance subsidiaries. Accounted for in one line by the equity method, proportionate share of value of unconsolidated subsidiary appears under Investments account on the balance sheet and proportionate share of income appears in Equity in Income from Non-Consolidated Subsidiary account on income statement if subsidiary has a loss then Investments account is written down and Equity in Income is negative.This tactic obscures the loss- makes it look like subsidiary's problem.

Sell assets to realize one-time gains at low capital gains tax rates – or take gain on early debt retirement • GE - you will know the company is in trouble • if it has large loss - they would smooth it otherwise • Receives large dividend payment from subsidiary (assumes cost method of accounts) • Control sales versus lease of product to control sales (look at sales breakout).

Hides revenues by taking unwarranted bad debt expenses or reserves for product repair. • German and Japanese accounting system encourage • Merges and sells off assets whose book value underestimates market value.

COST GIMMICKS CAPITALIZING EXPENSES Increase unfunded pension liabilities - don't have to fully fund pensions. Federal pension insurance agency covers defaults. Many expenses can be capitalized if management can explain how the expense provides benefits in future periods. for example, utilities - interest on construction/ new firms - start up costs / marketing expenses/ increase intangible assets.

REDUCE MANAGED COSTS • advertising / investment in plant & equipment / research and development / Avoid taking reserves for expected loss in future on sales now, e.g., warrantee costs, provision for bad loans etc. (do reverse to hide income to add in future periods through reversals of charges) / reduce inventories • and avoid payables / reduce maintenance - same effect as reducing assets life. • CHANGE DEPRECIATION METHOD OR LENGTHEN ASSET LIFE ASSUMPTION - reduces depreciation expense reported to shareholders - inflates earnings - keep tax depreciation the same - usually accelerated.

USE FIFO INSTEAD OF LIFO - inflates earnings in • inflationary period. • IF YOU USE LIFO - let inventory rundown to get to older, • cheaper inventory. • REDUCE PENSION EXPENSES - assume higher return/ • reduce contribution for past employees (retirees) • that have not been funded previously/ unfunded • pension 10% of equity (bad), 40% (worst). • FLOW THROUGH TAX CREDIT - reduces tax expense • now / more conservative to defer some credit - • spread over life of equipment purchased.

MANIPULATE TAX LOSS CARRY FORWARD (5 YEARS) OR BACKWARD (3 YEARS) • STATEMENT OF CASH FLOWS CAN HELPFIND PROBLEMS - it shows where cash is coming from and where it goes. • See Enron’s 2000 10K filed 4/2001 for example • See American International Group 10K filed 2/28/2008

You can’t rely on Wall Street analysts as much as you might think.