Download

1 / 27

270 likes | 441 Views

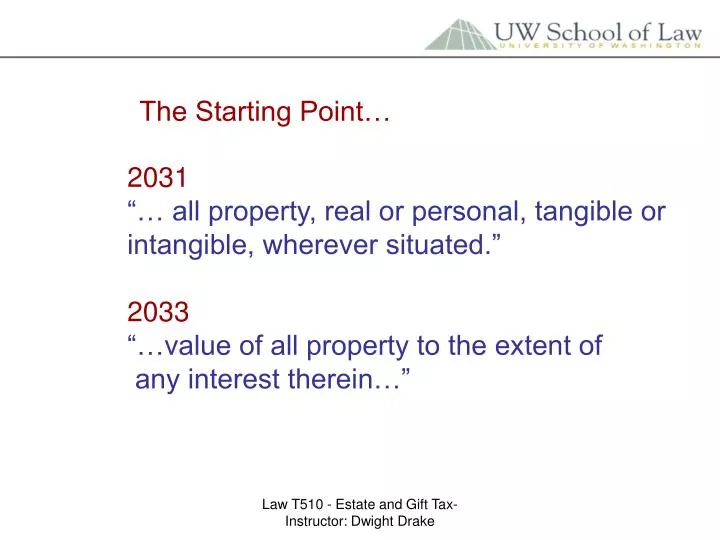

The Starting Point…. 2031 “… all property, real or personal, tangible or intangible, wherever situated.” 2033 “…value of all property to the extent of any interest therein…”. Fair Market Value…. “…willing buyer and willing seller” “…neither any any compulsion”

E N D

The Starting Point… 2031 “… all property, real or personal, tangible or intangible, wherever situated.” 2033 “…value of all property to the extent of any interest therein…” Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Fair Market Value… “…willing buyer and willing seller” “…neither any any compulsion” “…both having reasonable knowledge of relevant facts.” Reg. § 20.2031-1(b) Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(a) D Property Transfer T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder T dies, survived by X,Y,Z. Not included in T’s estate. No beneficial interest. Reg 20.2033-1(a). Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(b) D Property Transfer T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder X dies. Nothing included in X estate because X interest terminates at death. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(c) D Property Transfer T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder Y dies survived by X. Nothing in Y’s estate because Y did not outlive X. Had Y outlived X, he would own remainder interest. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(d) D Property Transfer T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder Z dies survived by X, but not Y. Z’s remainder interest is taxable in Z’s estate. It is a valuable remainder interest that Z’s estate owns. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Dynasty Trust D Property Transfer T … C GC GGC Income For Life Income for life Income for life Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(d) Calculation Property Value $100,000 X Age 60 Interest Rate 6% Table S Factor .35033 Remainder Value $35,033 Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(e) D Property Transfer T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder Z Dies, Survived By X and Y. Z’s contingent remainder interest included but messy valuation issue. Suppose X then dies before Y but before Z return filed? Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(f) D Property Transfer Revocable T X Y Z Income For Life 1st Contingent Remainder 2nd Contingent Remainder Z Dies, Survived By X and D, not Y. D still owner by virtue of revocation power. Rev. Rule 67-370 suggested inclusion in Z estate, but valuation problem insurmountable – include but value at nada. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (1)(g) D Property Transfer Contingent Reversion T X Y Income For Life 1st Contingent Remainder D Dies, Survived By X and Y. Reversion is real property interest. Reversion value included in D’s estate per 2033, but note future impact of 2037. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (2) • Homestead included under 2033, even if SS has occupancy rights for life. • Only half community property included in D’s estate, • but all CP gets basis step-up under 1014(b)(6). • Surviving spouse legal interest not impact inclusion in D • estate per 2034. Marital deduction eliminates tax hit. • If D and S are tenants in common with no survivorship, • only half included in D’s estate. • (e) If JT with survivorship right or tenancy by entirety, • nothing included under 2033 because interest terminates at death, but 2040 (b) includes one-half. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (3) • Accrued salary includable in estate under 2033. • Cash basis: Income in estate, IRD income-taxable to • recipient with deduction for estate tax. §691. • Accrual basis: Income in estate, estate pays income tax, • income tax will be estate tax deduction. • If income subject to contingencies that are gone, it is • included in estate per 2033. Goodman case. • If income mere expectancy at death, not included in • estate. But when recipient gets, is IRD subject to income tax. • Soc. Sec. benefits not included in estate because D has no • property right per law and can’t direct them. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (4) • Value of all business assets included in estate, including • goodwill. • Value of stock included in estate. Public stock: mean • between high & low sell on valuation date. Non-public: • what the experts say. • Partnership interest included. Look through to partnership • assets. Buy-Sell and discount factors. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 2 (5) • Any life insurance policy owned by D included in • estate under 2033. Valuation issue. • Annuity not included in D estate under 2033 because • all rights end at death. BUT, included per 2039 to extent • D purchased annuity. • Installment obligation included in estate under 2033. Valued at face if no proof otherwise. Income component is IRD to recipient with no basis step-up. §691. If note self-canceling • at D’s death (SCIN), no inclusion in estate. Must have • consideration for SCIN feature. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (1) • Fair market value stock: $2,000,000. • Book value stock: $1,500,000. • Why ever agree to sell at book? • Should Buy-Sell Contract govern? • If D taxed at $2 mill, but only gets $1.5 mill for stock, • is he getting cheated? Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (1) • For buy-sell to control under §2703(a): • 1. Agreement is bona fide business arrangement. • 2. Agreement is not device to transfer to family for less than • full consideration. • 3. Terms are comparable to similar arms-length deals. • If over 50% rights to purchase held by persons not natural • objects of bounty, §2703 requirements satisfied. Then what? Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (1)(a)-(c) • (a) $2 mill included in estate if sole shareholder. No arm’s length comparable and not bona-fide business deal. • (b) Sibling deal won’t qualify for non-family exception, nor meet three prong test. • (c.) If unrelated own 2/3 and are subject to same restriction, 2703 standards not apply. Still must meet prior law standards of (1) reasonable when made, (2) lifetime transfer restriction, and (3) obligated to sell. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (2)(a) • Partnership Property Value: $4,000,000. • Percentage Interest in Partnership: 25%. • Amount included in estate: $1,000,000 ? • Two huge discount factors: • D is minority interest with no control • D can’t market interest. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (2)(b) • Partnership Property Value: $4,000,000. • Percentage Interest in Partnership: 25%. • D’s pro rata share 1,000,000. • Less: Minority discount 20% 200,000. • Net 800,000. • Less: Marketability discount 20% 160,000. • Value net of discounts 640,000. • Must layer discounts Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (3) S P D Cash for stock $4 mill property for 99% LP Cash for stock Cash for stock C Corp. FLP Cash for 1% Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (4)(a) D dies, owning trust remainder interest behind B age 70. Value 100k at death; 200k six months following. Date of death included value: Remainder factor table S at 6%: .49007 Taxable Value on $100,000 $49,007 Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (4)(b) • Executor selects alternative valuation date: • Included value at alternative date: • Remainder factor table S at 6%: .49007 • Taxable Value on $200,000 $98,014 • Why didn’t factor change since B now 71? Not adjust for mere lapse of time factors. • What about 2032(c) – use alternate date only if reduce • estate? Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (4)(c) Changed facts: - B dies before alternate date. - Executor elects alternate date. Then, full $200,000 included. No more uncertainty on when B will die. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (4)(d) Changed facts: - Securities sold for $150k 3 months post death - Executor elects alternative date. Then, amount included is $150,000 plus valuation factor of .49007 = $73,510.50 Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Special Use Valuation Under 2032A Purpose: To give valuation break to farms and real property used in an active business. How: Allowing valuation not based on “highest and best” use. Max valuation savings: $750k plus inflation adjustment. Two valuations methods: Formula and Factor Recapture risk within 10 years – sale or cease use. Heirs liable for recapture tax. Income basis step-up may be elected on recapture, but then must pay interest from date of original return. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake

Problem 11 (5)(a)-(e) • Facts: • - Farm with FMV of $5 mill. • - Farm only real property and bulk of estate • - §2032A value is $4 mill • - D dies, heir cool with 2032A election • (a) Included in estate is $4.25 mill less inflation adjustment • per 2032A(a)(3) • (b) Income tax basis to heir is lower 2032A value • (c) Sale 5 years out for $6 mill. 2032A savings, at max • rate, must be paid within 6 months of sale. Basis step- • up allowed but then must pick up interest hit from date • of original return. • (d) Heir is liable for addition estate tax triggered on sale. • (e) Office building works. Only different valuation factors. Law T510 - Estate and Gift Tax- Instructor: Dwight Drake