Download

1 / 24

250 likes | 562 Views

Chapter. 27. Departmentalized Profit and Cost Centers. Section 1: Profit and Cost Centers and Departmental Accounting. Section Objectives. Explain profit centers and cost centers. Prepare the Gross Profit section of a departmental income statement.

E N D

Chapter 27 Departmentalized Profit and Cost Centers Section 1: Profit and Cost Centers and Departmental Accounting Section Objectives • Explain profit centers and cost centers. • Prepare the Gross Profit section of a departmental income statement. • Explain and identify direct and indirect departmental expenses. • Choose the basis for allocation of indirect expenses and compute the amounts to be allocated to each department.

Managerial Accounting • Provides financial information about business segments, activities, or products. • Supplies information on profitability of a specific department or order. • Provides data for making decisions.

Objective 1. Explain Profit Centers and Cost Centers

QUESTION: What is a cost center? ANSWER: A cost center is a business segment that incurs costs but does not produce revenue.

Cost Centers Cost centers do not directly earn revenue. Cost centers often provide services to other business segments: • Accounting department • Information systems department • Purchasing department

QUESTION: What is a profit center? ANSWER: A profit center is a business segment that produces revenue.

Profit Centers • Sells products or services to customers outside the business. • Can also be a segment of a company that provides a product to another revenue- producing segment. Accounting data is gathered and analyzed separately for each center.

Objective 2. Prepare The Gross Profit Section Of A Departmental Income Statement.

QUESTION: Why do businesses track revenue and expenses by segment? ANSWER: Detailed data on individual departments helps managers assess the profitability of products and department operations.

Departmentalized Operations • Departmental accounts are included in the general ledger. • Sales and purchases are recorded by department. • Merchandise inventories are counted and reported by department.

Departmental Accounts in the General Ledger Sales—Shoes Sales—Clothing Record all sales for the Clothing department. Record all sales for the Shoes department.

SALES JOURNAL PAGE 1 SALES ACCOUNTS SALES TAX SALES— SALES— DATE SLIP CUSTOMER’S POST. RECEIVABLE PAYABLE CLOTHINGSHOES NO. NAME REF. DEBIT CREDIT CREDIT CREDIT 2007 Jan. 2 1005 Ashley Morgan 106.40 6.40 100.00 3 1006 Robin Sullivan 477.00 27.00 300.00 150.00 3 1007 Billy Wilson 190.80 10.80 115.00 65.00 31 Totals 9,964.00 564.00 6,200.00 3,200.00 (111) (231) (401) (402) Departmental Sales Journal Separate columns are kept for the two different departments.

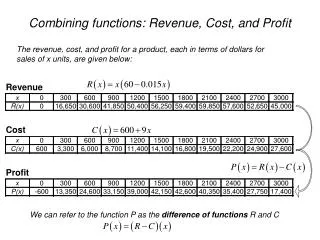

Fifth Avenue Income Statement (Partial) Year Ended December 31, 2007 Clothing Shoes Total Operating Revenue Sales 487,950 162,650 650,600 Less Sales Returns and Allowances 4,125 1,375 5,500 Net Sales 483,825 161,275 645,100 Cost of Goods Sold Merchandise Inventory, Jan. 1, 20-- 32,000 15,000 47,000 Purchases 216,000 48,000 264,000 Freight In 4,200 500 4,700 Delivered Cost of Purchases 220,200 48,500 268,700 Less: Purchases Returns and Allowances 3,500 350 3,850 Purchases Discounts 4,000 400 4,400 Total Deductions 7,500 750 8,250 Net Delivered Cost of Purchases 212,700 47,750 260,450 Total Merchandise Available for Sale 244,700 62,750 307,450 Less Merchandise Inventory, Dec. 31, 20-- 29,650 9,500 39,150 Cost of Goods Sold 215,050 53,250 268,300 Gross Profit on Sales268,775 108,025 376,800 Departmental Income Statement Gross profit by department

Objective 3. Explain And Identify Direct And Indirect Departmental Expenses.

Operating Expenses • Direct expenses can be identified directly with a department. • Indirect expenses cannot be directly related to an activity in a department. • Semidirect expenses cannot be directly assigned to individual departments, but are closely related to individual departments.

Objective 4. Choose The Basis For Allocation Of Indirect Expenses And Compute The Amounts To Be Allocated To Each Department.

AllocatingSemidirect and Indirect Expenses • Takes place after adjusting entries have been made and adjusted trial balance completed. • Can be based on: • percent of sales, • percent of value of merchandise inventory, • percent of space occupied.

QUESTION: Basis: Dept. Square Feet Clothing 2,400 Shoes 600 Total 3,000 % 80 20 100 Rent Expense Allocation x $19,200 = $ 15,360 x $19,200 = $ 3,840 $ 19,200 How is rent expense generally allocated? Allocating Rent Expense Rent expense is generally based on proportion of the square footage occupied.

Expense Allocations Insurance: Based on the cost of the furniture, fixtures, and inventory used in the department’s operations. Utilities: Based on square footage occupied. Office Salaries:Based on total sales for each department.

Nondepartmentalized Expenses • Do not apply to operations. • Are not allocated to departments. • Appear in the Other Income and Other Expenses section of the income statement. Interest income and interest expenses are not allocated to departments.

R E V I E W SECTION Complete the following sentences: Managerial accounting ____________________ provides information about business segments, activities, or products. If a business segment does not directly earn revenue, it is referred to as a __________. cost center In a departmentalized business operation, a ___________ produces revenue by selling products to outside customers. profit center

R E V I E W SECTION Complete the following sentences: The departmental income statement identifies gross profit by __________. department Indirect _______ expenses are operating expenses that cannot be readily identified by department and are not closely related to activity within a department. Rent expenses is often allocated based on _____________. square footage

Thank You for using College Accounting, 11th Edition Price • Haddock • Brock