Download

1 / 40

410 likes | 603 Views

Market Equilibrium: The Invisible Hand. Randy Rucker Professor Department of Agricultural Economics and Economics June 19, 2013. Review: Consumer Choice and Demand. Determinants of the Demand for a Good: Price of the good of interest Prices of Substitutes Prices of Complements

E N D

Market Equilibrium: The Invisible Hand Randy Rucker Professor Department of Agricultural Economics and Economics June 19, 2013

Review: Consumer Choice and Demand • Determinants of the Demand for a Good: • Price of the good of interest • Prices of Substitutes • Prices of Complements • Incomes • Tastes and Preferences • Quality • etc.

Review: Consumer Choice and Demand • The Demand Curve Shows the Relationship Between the Price of a Good and the Quantity of that Good Demanded • Ceteris Paribus (Other Factors are Held Constant) • The Law of Demand—What does it say?

Review: Consumer Choice and Demand • A Change in Price Causes a Change in Quantity Demanded • This is a movement along the demand curve. • A Change in Other Factors (e.g., Income) Causes a Change in Demand • This is a shift in the demand curve.

Review: Firms, Profits, and Supply • Determinants of the Supply of a Good: • Price of the good of interest • Prices of Inputs • Changes in Technology • Number of Firms in the Industry • Quality • etc.

Review: Firms, Profits, and Supply • The Supply Curve Shows the Relationship Between the Price of a Good and the Quantity of that Good Supplied • Ceteris Paribus (Other Factors are Held Constant) • The Law of Supply—What does it say?

Review: Firms, Profits, and Supply • A Change in Price Causes a Change in Quantity Supplied • This is a movement along the supply curve. • A Change in Other Factors (e.g., an input price) Causes a Change in Supply • This is a shift in the supply curve.

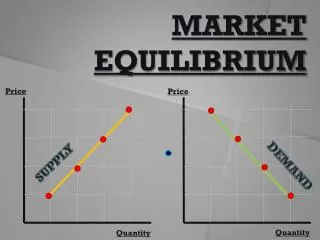

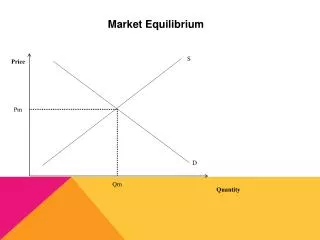

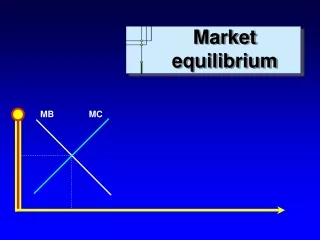

Market Equilibrium • Now, let’s put Demand and Supply on the same Graph . . .

Market Equilibrium • What Will Be the Price and Quantity that “Clear the Market”? • To Answer This, Suppose the Price Is Initially Below the Price Where the Demand and Supply Curves Intersect ($4). • What Will Happen?

Market Equilibrium • At a Price of $2 per Hour, there is a “Shortage.” At that Price, the quantity demanded exceeds the quantity supplied. • Babysitters have way more requests than they are willing to provide at $2 per hour. • What will happen?

Market Equilibrium • Parents who can’t get a babysitter, and are willing to pay more than $2 per hour, will offer, say $3 per hour. • This higher price will cause some parents to stay home, or not stay out as long. That is, quantity demanded will fall. • The higher price will also induce some babysitters to work more hours. That is, quantity supplied will increase. • Thus, the shortage gets smaller and these “market forces” will continue to drive prices up.

Market Equilibrium • Alternatively, Suppose the Price Is Initially Above the Price Where the Demand and Supply Curves Intersect. • What Will Happen?

Market Equilibrium • At a price of $6 per hour, there is a “Surplus.” At that price, the quantity supplied exceeds the quantity demanded. • Babysitters are willing to work way more hours than parents are willing to purchase. • What will happen?

Market Equilibrium • Some babysitters who can’t get any work at $6 per hour, and are willing to babysit for less, will offer their services for, say $5 per hour. • This lower price will induce some parents to go out on a date. That is, quantity demanded will increase. • The lower price will also cause some babysitters to work fewer hours. That is, quantity supplied will decrease. • Thus, the surplus gets smaller and these “market forces” will continue to drive prices down.

Market Equilibrium • So, if price is below $4, there will be a shortage, and price will increase. • Alternatively, if price is above $4, there will be a surplus and price will fall. • In each case above, what causes prices to change? An all-knowing central planner? Happenstance? Market forces?

Market Equilibrium • When the price is equal to $4, quantity supplied is equal to quantity demanded. • That is, the market clears—all parents who are willing to pay that price for a babysitter are able to get one, and • all babysitters who are willing to babysit at that price are able to.

Market Equilibrium • Note: If market forces are allowed to work, prices will adjust and shortages and surpluses will go away. • Think: What if prices are not allowed to adjust? • Let’s come back to this if we have time.

Market Equilibrium • The fundamental forces just described in the market for babysitters will also be at work in markets for other goods. • QUESTIONS???

Market Equilibrium • Next, let’s apply these principles to see what happens if the market equilibrium described above is disturbed . . . • NOTE: Such disturbances are the rule rather than the exception. Markets are always adjusting to changing conditions.

Market Equilibrium • First, what happens to the market for Tenderloin Steaks if incomes increase? • Recall that Tenderloin Steaks are a “normal good.”

The Market for Tenderloin Steaks Price ($/Q) S0 P0 D0 Q(Quantity/week) Q0 The Initial Equilibrium Price and Quantity

The Market for Tenderloin Steaks Price ($/Q) S0 2 2 1 P1 P0 D1 D0 Q(Quantity/week) Q0 Q1 Impacts of an Increase in Demand Resulting from an Increase in Incomes

Market Equilibrium • Second, what happens to the market for Top Ramen if incomes increase? • Recall that Top Ramen is an “inferior good.”

The Market for Top Ramen Price ($/Q) S0 P0 D0 Q(Quantity/week) Q0 The Initial Equilibrium Price and Quantity

The Market for Top Ramen Price ($/Q) S0 1 2 2 P0 P1 D0 D1 Q(Quantity/week) Q1 Q0 Impacts of a Decrease in Demand Resulting from an Increase in Income

Market Equilibrium • Third, what happens in the wheat market if there is an increase in supply due to favorable growing conditions in China and Russia?

The Market for Wheat Price ($/Q) S0 P0 D0 Q(Bushels/year) Q0 The Initial Equilibrium Price and Quantity

The Market for Wheat Price ($/Q) S0 2 2 S1 P0 1 P1 D0 Q (Bushels/year) Q0 Q1 Impacts of an Increase in Supply Resulting from Good Growing Conditions

Market Equilibrium • Fourth, what happens to the market for peanut butter if there is a drought in the Southeastern United States?

The Market for Peanut Butter Price ($/Q) S0 P0 D0 Q(Quantity/year) Q0 The Initial Equilibrium Price and Quantity

The Market for Peanut Butter Price ($/Q) S1 S0 2 2 1 P1 P0 D0 Q0 Q (Quantity/year) Q1 Impacts of a Drought in the Southeastern United States

Cautionary Notes • Choose your examples carefully • Why babysitters, steaks, Top Ramen, wheat, and peanuts? Rather than, say • Cars, houses, or shoes?

Cautionary Notes (cont.) • Analyze the effects of one change at a time. • It is easy to try to analyze real-world examples and create confusion because more than one factor is changing. • Examples

Cautionary Notes (cont.) • Shortages and surpluses and the media. • Does a decrease in supply cause a shortage? • Does an increase in supply cause a surplus?

Cautionary Notes (cont.) • What if prices are not allowed to adjust? Quickly? or Another day? • These stories can be complex . . .

Cautionary Notes (cont.) • Maximum prices (price ceilings) • Apartments in NYC and CA • Anti-price gouging laws • Gas price controls in the 1970s • Rationing of health care services • Others . . .

Cautionary Notes (cont.) • Minimum prices (price floors or price supports) • Minimum wages • Farm programs • Proposal for minimum price for alcohol in the U.K. • Others . . .