Download

1 / 28

280 likes | 475 Views

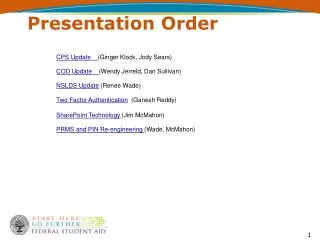

Order Of Presentation. Topic Motivation Data Collection and Challenges Issues of Interest Discussion. T he Economic and Reporting Incentives of State and Local Government Pensions. Charlie Kile. State & Local Government Pensions The Next Financial Bubble ?.

E N D

Order Of Presentation • Topic • Motivation • Data Collection and Challenges • Issues of Interest • Discussion

The Economic and Reporting Incentivesof State and Local Government Pensions Charlie Kile

State & Local Government Pensions The Next Financial Bubble? “The unfunded liability for Illinois’ five state-run pension systems has officially passed the $100 billion mark.” http://www.illinoispolicy.org/congrats-illinois-your-pension-shortfall-is-a-100-billion/ Ted Dabrowski Illinois Policy Institute 13 Mar 2014 accessed 4 Apr 2014

State & Local Government Pensions The Next Financial Bubble? Commission on Government Forecasting and Accountability

State & Local Government Pensions The Next Financial Bubble? The General Assembly Retirement System, a defined benefit plan for 294 General Assembly retirees has only 17 cents in assets for each of the 303 million dollars it needs to have invested today meet its [estimated] $900 million required benefit payouts over the next 33 years. Stated differently, the fund’s assets cover only the next 2.5 years of benefit payouts. http://www.illinoispolicy.org/congrats-illinois-your-pension-shortfall-is-a-100-billion/ Ted Dabrowski Illinois Policy Institute 13 Mar 2014 accessed 4 Apr 2014

State & Local Government Pensions The Next Financial Bubble? “Some state pension funds could run out within the decade.” “As many as 31 states are on track to run out of funds by 2030” “Unfunded State Pensions Face Prospects of Becoming Federal Issue” by Nicole Bullock and Hal Weitzman. Financial Times May 20, 2010 accessed May 5, 2013 Joshua Rauh and Robert Novy-Marx “Pension Security Bonds: A New Plan to Address the State Pension Crisis” The Economist’s VoiceBerkeley International Press (June 2010).

State & Local Government Pensions The Next Financial Bubble? “New York City’s pension costs have increased tenfold in the past decade” “According to estimates presented in this report . . . over the next five years, tax-funded annual contri-butionsto the New York State Teachers’ Retirement System (NYSTRS) will more than quadruple”. McMahon, E. J. and Josh Barro (2010) New York’s Exploding Pension Costs Empire Center for New York State Policy, a project for the Manhattan Institute of Policy Research. SR8-11 December 2010.

State & Local Government Pensions The Next Financial Bubble? “Most affected groups see the advantages in the process that allows public employees to seek benefits, politicians to grant them and taxpayers to acquiesce, while deferring the problems of funding public pensions to a future generation of taxpayers” National Conference of State Legislatures, (1985) Public Pensions: A Legislator’s Guide. Denver CO. (p.3)

State & Local Government Pensions The Next Financial Bubble? The Intergenerational Effect - One generation benefits from a particular public service and leaves the cost to another generation. Future generations will choose to “vote with their feet” Tobin, James. 1974. “What Is Permanent Endowment Income?” American Economic Review, 64:2, pp. 427-32. Tiebout, Charles A Pure Theory of Local Expenditures. The Journal of Political Economy, Vol. 64, No. 5, (Oct., 1956), pp. 416-424.

Government Pension ConsequencesCredit Downgrades “Credit pressure related to large unfunded pension liabilities has led to ratings downgrades in the debt of several states and municipalities, and in some cases, has led to bankruptcies of the affected municipalities.” Medioli, Alfred, Thomas Aaron and Jessica Raab (2013) The US Public Pension Landscape: Patterns of Funding, Correlation and Risk. Moody’s Investors Services Report Number 157154 (September 9, 2013).

Government Pension Consequences Legislative Reform “The National Picture of Public Pension Changes: What Benefit Reductions have States Enacted?” by Nancy Hudspeth. University of Illinois at Chicago Institute of Public Affairs (10 May 2013).

Government Pension Consequences Legislative Reform “As a result, state pension obligations in many states have legal priority that is senior even to general obligation bonds”. Brown, Jeffrey and Wilcox, David (2009) Discounting state and local pension liabilities. American Economic Review, 99 (2): 538–542.

Government Pension Consequences Accounting Reform GASB Statement No. 67 “Financial Reporting for Pension Plans” (issued June 2012) GASB Statement No. 68 “Accounting and Financial Reporting for Pensions” (issued June 2012) Government Accounting Standards Board

Government Pension ConsequencesAlleged Benefits • Ability to attract and retain risk averse workers, who are willing to trade lower wages for financial security; • Behavioral Evidence • Economic Stability

Government Pension ConsequencesAlleged Benefits: Behavioral Evidence “Savings and investment outcomes are heavily influenced by plan design features that matter little in standard economic models” John Beshears, James J. Choi, David Laibson and Brigitte C. Madrian. “Behavioral economics perspectives on public sector pension plans” Journal of Pension Economics and Finance (2011).

Government Pension ConsequencesAlleged Benefits: Behavioral Evidence • A pervasive lack of financial literacy in the U.S. Population e.g., Lusardi and Mitchell (2006); Lusardi and Mitchell (2007); LusardiTufano (2009); Lusardi et. al. (2010) • Irresponsible management of retirement accounts • Procrastination and avoidance behavior • Inability to identify essential features of their plan • Failing to utilize employer matching Choi et al. (2013); Carrol et al. (2009); Beshears et al. (2008); Choi et al. (2004); Choi et al. (2006); Madrian and Shea (2001); Gustmanet al. (2007); Chan and Stevens (2008); Choi et al. (2013) • Irrational investing behavior • Chasing past returns in their allocation choices. • Ignoring mutual fund fees • Diversifying mutual funds within the same asset class Benartzi, 2001; Choi et al., 2004, Calvetet al., 2009 Choi et al., 2009; Choi et al., 2010; Huberman and Jiang (2006). • Removing choices from plans dramatically increases participation. Beshearset al. (2010)

Government Pension ConsequencesAlleged Benefits: Economic Stability $187 Billion paid to retired state and local government employees generated over $170 Billion in economic activity, $50 billion paid back to other workers. $5.6 billion paid back in taxes on the benefits (Direct Effects of Benefits only). Bovie, Ilana “Pensionomics: Measuring the Economic Impact of DB Pension Expenditures” National Institute on Retirement Security 6 Mar 2012.

Data Collection Challenges Chicago residents, through their state and local taxes, support 16 different pensions: City Police, Fire, Laborers and Municipal Employees, Transit Authority, City School District, Parks and Recreation District, Regional Transportation Authority, Cook County, County Forest Preserve District, Chicago Metropolitan Water Reclamation District and five State of Illinois plans. “The U.S. Public Pension Landscape: Patterns of Funding, Correlation and Risk” by Alfred Medioli, Jessica Raaband Thomas Aaron Moody’s Investor Services.

Data Collection Procedure • Collect the CAFRs of all 50 states • Note all pension plans identified in the CAFRs • Locate the CAFR for the plan online • Contact plan administrator for missing plans • 260 Distinct Plans

Issues – Measuring the Liability (and Unfunded Liability) “The true extent of public pension underfunding has been obscured by governmental accounting rules, which allow pension liabilities to be discounted at expected rates of return on pension assets”. Novy-Marx, Robert, and Rauh, Joshua D. “The Intergenerational Transfer of Public Pension Promises”

Issues – Measuring the Liability GASB requires that the future benefit payments be measured with a “liability”. The reported liability measure is determined using a discount rate equal to the expected return of the assets.

Issues – Measuring the Liability Assumed higher returns reduce the measured liability. A reduced liability requires fewer assets to be set aside, which in turn, lowers the amount contributed from this period’s revenues.

Issues – Measuring the Liability Financial Theory would suggest that the sourcing and usage of funding are independent. Typically, the discount rate measures the degree of certainty that payments will be made.

Issues – Measuring the Liability “Changing the discount rate to reflect state general obligation debt, the authors estimate that the national total of promised liabilities is $3.20 trillion (based on current salary and service).” “Using zero-coupon Treasury yields, estimated promised liabilities are $4.43 trillion.” Novy-Marx, Robert and Rauh, Joshua D. (2011) Public pension promises: how big are they and what are they worth? Journal of Finance, forthcoming.

Issues – Questions of Interest • Incentives that may help explain underfunding or contribution levels. • The economic and reporting consequences of new government accounting standards • Pension asset allocation and performance

Issues – Variables of Interest • Revenue (scaled by population) • Interest Payments (scaled by population) • Key Actuarial Assumptions • Bond Ratings • Portfolio Risk / Assumed Investment Returns • Plan Governance (Pct. Board Appointed by State, Pct. Board Members of a given plan)

The 1% increase in return assumption reduces the normal costs by over 25%, but is offset by the increased normal costs from General Salary Growth and Inflation. Taxpayers are “better off” deferring taxes until pension payments become due, and then using the excess cash to reduce debt, rather than giving to the fiduciary (government) to invest at expected returns. Hustead, Edwin C. “Determining the Cost of Public Pension Plans” in Pensions in the Public Sector, ed. Olivia Mitchell and Edwin C. Hustead (Philadelphia, PA. University of Pennsylvania Press 2001).

Pension fund managers assume higher investment risks and assume a higher rate of return following periods of relatively poor performance. Evidence that plan administrators use Economically Targeted Investments (ETIs) that are associated with below market risk adjusted returns Pennacchi, George and Mahdi, Rastad (2011) Portfolio allocation for public pension funds.Journal of Pension Economics and Finance, 10 (2): 221–245. Doyle (2006) Mitchell & Hsin (1997), Nofsinger (1998) and Ramano (1993)