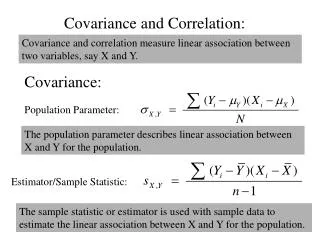

Covariance

290 likes | 372 Views

Covariance. And portfolio variance. Review question. Define the internal rate of return. Answer:. The internal rate of return of a project is r such that, given the cash flows CF t of the project,. The states of nature model. Time zero is now. Time one is the future.

Covariance

E N D

Presentation Transcript

Covariance And portfolio variance

Review question • Define the internal rate of return.

Answer: • The internal rate of return of a project is r such that, given the cash flows CFt of the project,

The states of nature model • Time zero is now. • Time one is the future. • At time one the possible states of the world are s = 1,2,…,S. • Mutually exclusive, collectively exhaustive states. • This IS the population. No sampling.

The states of nature model • States s = 1,2,…,S. • Probabilities ps • Asset j • Payoffs Rj,s • Expected rate of return

= rate of return on j in state s = probability of state s = expectation of rate on j

Variance and standard deviation • Form deviations • Take their expectation.

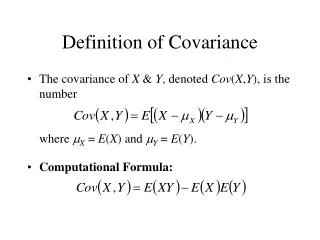

Covariance • Form the product of the deviations • (positive if they both go in the same direction) • and take the expectation of that.

Covariance • It measures the tendency of two assets to move together. • Variance is a special case -- the two assets are the same. • Variance = expectation of the square of the deviation of one asset. • Covariance = expectation of the product of the deviations of two assets.

Correlation coefficient • Like covariance, it measures the tendency of two assets to move together. • It is scaled between -1 and +1.

Correlation coefficient • = covariance divided by the product of the standard deviations. • Size of deviations is lost.

Intuition from correlation coefficients • = 1, always move the same way and in proportion. • = -1, always move in opposite directions and in proportion. • = 0, no tendency either way.

Portfolio Risk and Return • Portfolio weights x and 1-x on assets A and B.

An amazing fact • Mixing a risky asset with a safe asset • is often safer than the safe asset.

Variance of portfolio return • Diversification effects

Portfolio deviation Deviation squared Remember

Portfolio variance depends on covariance of the assets. Positive covariance raises the variance of the portfolio.

Portfolio variance depends on covariance of the assets. Positive covariance raises the variance of the portfolio.