Download

1 / 15

150 likes | 186 Views

This presentation explores the determinants of bank profitability in Vietnamese commercial banks using the dynamic GMM and LSDV methods. The study analyzes data from 1999 to 2018 and considers factors such as equity, capital ratios, operational efficiency, inflation, GDP growth, and more.

E N D

Determinants of bank profitability from the dynamic model: GMM and LSDV methods Dr. Thao Nguyen Dr. Chris Stewart 13-07-19

Outline of the presentation • Objectives • Vietnamese banking system • Literature review • Methodology • Results • Conclusions

1. Objectives • We employ dynamic generalised method of moments (GMM) estimator technique and the Least squares dummy variables (LSDV) • This paper estimates bank profitability determinants of Vietnamese commercial banks • Data 50 commercial banks from 1999 to 2018

CR (3 and 5 banks) and HHI for the Vietnamese banking system from 1999 to 2018

3. Literature review • García-Herrero et al. (2009) indicate that the best performing banks are those who maintain a high level of equity relative to their assets. Banks with higher capital ratios tend to face lower costs of funding due to lower prospective bankruptcy costs. There is also empirical evidence that the level of operational efficiency, measured by the cost-income ratio (Goddard and Wilson, 2009) or overhead costs over total assets (Athanasoglou et al., 2008) positively affects bank profitability. • Most studies have shown a positive relationship between inflation, GDP growth and bank profitability (e.g. Bourke, 1989; Athanasoglou et al., 2008). Furthermore, there is some evidence that the legal and institutional characteristics of a country matter.In Vietnam: problem of data collection • According to the results of Bourke (1989), the bank concentration ratio shows a positive and statistically significant relationship with the profitability of a bank and is, therefore, consistent with the traditional structure–conduct–performance paradigm. In contrast, the results of Staikouras and Wood (2004) show a negative but statistically insignificant relationship between bank concentration and bank profits.

4. Methodology • The (pooled) OLS estimator (without fixed-effects) will suffer from dynamic panel bias and will be inconsistent for small T (the number of time periods) in the sense that increasing N (the number of cross-sectional units) will not make the estimator consistent • The fixed-effects estimator will also suffer from dynamic panel bias and inconsistency (as N tends to infinity) when T is small • We consider both the one-step GMM estimator (with robust coefficient standard errors) and the two-step GMM estimator (with Windmeijer, 2005, small sample corrected coefficient standard errors). A downward bias afflicts the coefficient standard errors calculated by the two-step method, however, using Windmeijer (2005) corrected standard errors with two-step GMM greatly reduces this problem. A feasible approximation of Windmeijer’s small sample correction for two-step GMM’s coefficient standard errors have been shown to perform well in simulations (Roodman, 2009). • Bruno (2005a and b) implements the Least square dummy variables (LSDVC) and estimates a bootstrap variance-covariance matrix for the corrected estimator.

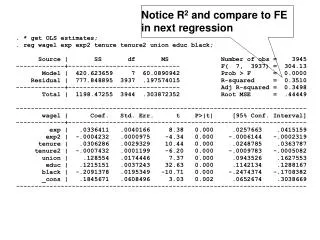

5. OLS, FE, Biased corrected FE and GMM estimations for the full sample with ROA

5. OLS, FE, Biased corrected FE and GMM estimations with ROA using GSM procedure

6. Conclusions • We find that profit is statistically significant with assets size (LNTA), equity (ETA), deposits (DTA), off-balance-sheet items (OOTA), labour productivity (RE) and expansion of the number of branches (LNBR). When the bank improves the performance via profit, the overhead cost also increases significantly (OCTA). The main component of the profit is interest income (INI). The factors that reduce that profitability of banks include loan loss provisions (LLPL), operating expenses (EXTA) and non-performing loans (LNPL). Banks with high values of customer loans (LA) and have been in existence for a long period of time also suffer from decreasing profitability. • Regarding the industry-macroeconomic factors, market share of the banks in assets size (HHI-TA) is statistically significant with profitability. When the economy develops at high speed via increasing inflation rate and GDP growth rate, bank profitability also experiences increasing values.

6. Conclusions • The next step is to investigate the determinants of other bank profitability including the return to equity (ROE) and interest income to assets (IOA). Moreover, we also need to examine the impact of the recent financial crisis, with samples of time periods: the pre-crisis period (1999-2006); the crisis period (2007-2009), the post-crisis period (2010-2018). The determinants of sub-samples following the bank types (SOCBs, JSCBs, JVCBs and FBs) and bank asset size are also being considered for investigations.