Download

1 / 16

160 likes | 307 Views

Financial Levees: Intermediation, External Imbalances, and Banking Crises. Mark S. Copelovitch Department of Political Science & La Follette School of Public Affairs University of Wisconsin – Madison copelovitch@wisc.edu. David Andrew Singer Department of Political Science MIT dasinger@mit.edu.

E N D

Financial Levees:Intermediation, External Imbalances, and Banking Crises Mark S. CopelovitchDepartment of Political Science &La Follette School of Public AffairsUniversity of Wisconsin – Madison copelovitch@wisc.edu David Andrew SingerDepartment of Political ScienceMIT dasinger@mit.edu

What Caused the “Great Recession”? External imbalances and capital inflow bonanzas • Widely seen as proximate or underlying causes (Reinhart and Reinhart 2008, Bernanke 2009, Reinhart and Rogoff 2009, Caballero 2011, Chinn and Frieden 2011) • Building on earlier work on crises in Latin America and East Asia (Diaz-Alejandro 1985, Calvo 1998, Kaminsky and Reinhart 1999) The new conventional wisdom? • Obstfeld and Rogoff (2009): crises and imbalances “intimately related” • Bini Smaghi (2008): “two sides of the same coin” • Portes (2009): “global macroeconomic imbalances are the underlying cause of the crisis”

The Global Imbalance Chorus Portes (2009) • “Global imbalances…brought low interest rates, the search for yield, and an excessive volume of financial intermediation, which the system could not handle responsibly” King (2010) • “The massive flows of capital from the new entrants into western financial markets pushed down interest rates and encouraged risk-taking on an extraordinary scale” Reinhart and Reinhart (2008) • “Capital inflow bonanza periods are associated with a higher incidence of banking, currency, and inflation crises in all but the high income countries.” • “Episodes end, more often than not, with an abrupt reversal or “sudden stop” a la Calvo (1998)”

Problems With the Imbalances View Empirical anomalies • Some countries with large current account deficits escaped the crisis (Australia, New Zealand) while others were hit hardest (US, UK, Greece) • No “sudden stop” in the US, despite collapse of interbank lending • 2/3 US capital inflows came from Europe, not large surplus countries • “Financial crises, driven by excessive loan growth, occurred by and large independent of current account imbalances” (Jorda, Schularick, and Taylor 2011) • 1981-2007: weak correlation between credit booms and both current account deficits (0.01) and bonanzas (0.11) • Large credit booms in key surplus countries (China 1997-2000; India 2001-4; Brazil 2003-7; Japan in 1980s; US in 1920s)

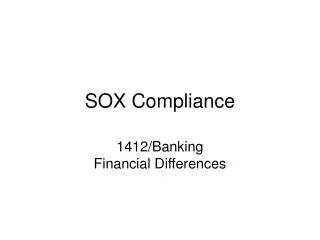

US Balance of Payments (% of GDP) SOURCE: Borio and Disyatat 2011; Bureau of Economic Analysis

Our Argument: Consider Financial (Dis)intermediation Global imbalances are destabilizing only under certain circumstances • Unpacking the “current account” • Savings minus investment: an intertemporal phenomenon • Deficits are especially problematic when returns on investment are uncertain • Financial sectors with low levels of securitization are resistant to the destabilizing influences of capital inflows • Securitization exacerbates the mispricing of risk • Disintermediation distorts the assessment of returns on investment Traditional banking activity acts as a “financial levee” • Caveat: traditional banking does not prevent all crises! • Bank credit growth is still a key determinant of financial instability

Empirical Analysis – Variables and Model Specifications • Dependent variable = 1 if country i experiences a banking crisis in year t • All crisis (Reinhart and Rogoff 2008/9): 375 crises (20.1%), 1981-2007 • Systemic crises (Laeven and Valencia 2008): 114 crises (2.4%), 1981-2007 • Key independent variable: Level of securitization of the financial sector • Measured two ways: • 1) Regulatory measure of depth/liberalization (Abiad et. al. 2008) • Has a country taken measures to develop securities markets (0/3)? • Is a country’s equity market open to foreign investors (0/2)? • 2) Market/bank ratio: stock market volume / bank lending • Crisisit = 0 + 1 External imbalance + 2 Securitization + 3 Imbalance*Securitization +4Credit growth + 5Regime type + 6GDP per capita + 7GDP growth +8Inflation + 9OECD average growth + 10Commodity prices + 11 US interest rate + 12 (Last crisis) + 13 (Last crisis)2 + 14 (Last crisis)3+

SOURCE: World Bank, Database on Financial Development & Market Structure

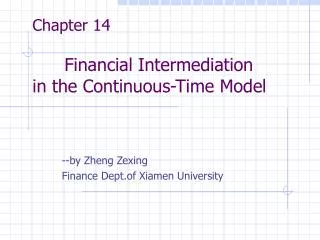

Interactive Marginal Effects – Banking Crisis (Reinhart-Rogoff)

Interactive Marginal Effects – Banking Crisis (Reinhart-Rogoff)

Conclusions and Next Steps Conclusions • Market structure conditions the impact of current account deficits on financial stability • Capital inflows need not be destabilizing: traditional intermediation serves as a “financial levee” • However: extension of bank credit – independent of the current account balance – is a key determinant of crises Next Steps • Consider more directly the role of regulation • Find (or create) better data on the scope & stringency of regulation, and de jure vs. de facto supervisory independence & mandates • State ownership • Case study analysis

Interactive Marginal Effects – Banking Crisis (Reinhart-Rogoff)

Countries in Sample N = 1247

Predicted Change in Probability of a Banking Crisis, One Standard Deviation Increase in Current Account Deficit, by Market/Bank Ratio Market/Bank ratio (log), percentile Current account (% GDP, 5 year moving average): increase from deficit of 1.5% to 5.4%