Download

1 / 5

60 likes | 212 Views

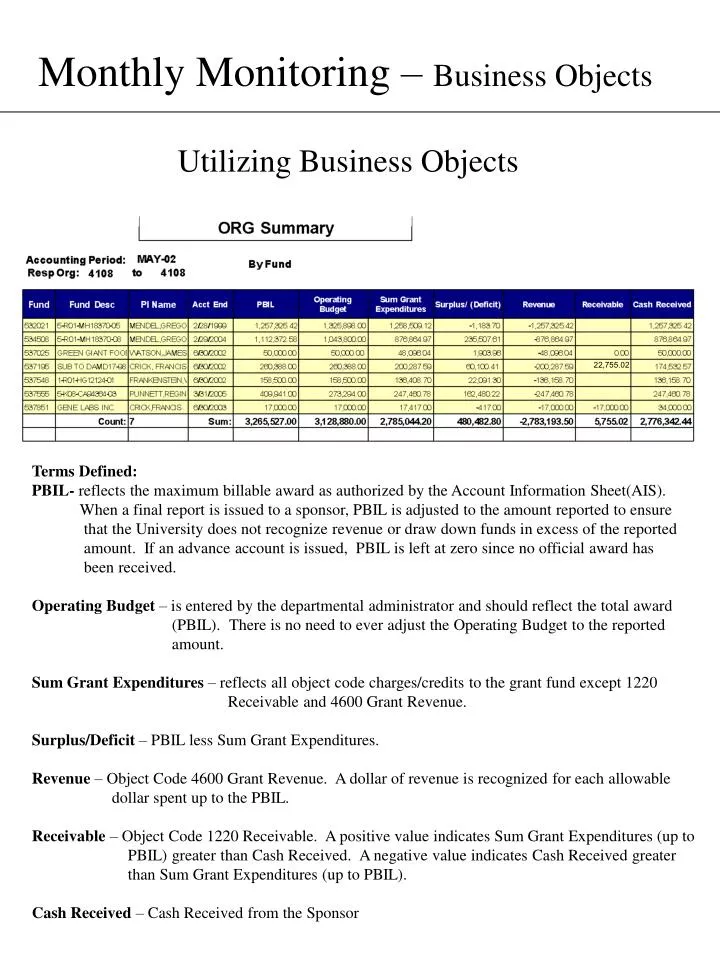

Monthly Monitoring – Business Objects. Utilizing Business Objects. 22,755.02. Terms Defined: PBIL- reflects the maximum billable award as authorized by the Account Information Sheet(AIS).

E N D

Monthly Monitoring – Business Objects Utilizing Business Objects 22,755.02 Terms Defined: PBIL- reflects the maximum billable award as authorized by the Account Information Sheet(AIS). When a final report is issued to a sponsor, PBIL is adjusted to the amount reported to ensure that the University does not recognize revenue or draw down funds in excess of the reported amount. If an advance account is issued, PBIL is left at zero since no official award has been received. Operating Budget – is entered by the departmental administrator and should reflect the total award (PBIL). There is no need to ever adjust the Operating Budget to the reported amount. Sum Grant Expenditures – reflects all object code charges/credits to the grant fund except 1220 Receivable and 4600 Grant Revenue. Surplus/Deficit – PBIL less Sum Grant Expenditures. Revenue – Object Code 4600 Grant Revenue. A dollar of revenue is recognized for each allowable dollar spent up to the PBIL. Receivable – Object Code 1220 Receivable. A positive value indicates Sum Grant Expenditures (up to PBIL) greater than Cash Received. A negative value indicates Cash Received greater than Sum Grant Expenditures (up to PBIL). Cash Received – Cash Received from the Sponsor

Monthly Monitoring – Business Objects ORG Summary 22,755.02 Problem Areas to look for: Unbudgeted Funds : PBIL Not equal to Operating Budget As indicated with the above, funds 534508 and 537555 need to have their Operating Budgets increased. 534508 probably had carry over from the previous segment 532021 and 537555 probably just received funding for the –03 budget period. Unallowable Charges : Sum Grant Expenditures not equal to (Grant Revenue) This will only be true if expenditures exceed PBIL causing a (deficit) or if an unallowable charge has been made. As indicated with the above, on fund 537548, expenditures exceed revenue by $250 which means an unallowable charge of $250 has been made on the fund since there is not a (deficit) on the fund. No AIS issued : Cash Received greater than PBIL Often with Corporate Clinical Trials, the award(PBIL) is only increased when the sponsor makes payment. As indicated with the above, this occurs on fund 537851. The fund is showing a deficit because the award has not been increased by the $17,000 in excess cash. You would want to contact Research Services to see if an AIS is going to be issued.

Monthly Monitoring – Business Objects ORG Summary 22,755.02 More Things to look for: Reported Funds or Carryover: PBIL not an even dollar amount PBIL is reduced to the reported amount. On 532021 above there is a good indication that the fund was reported on because PBIL is less than the operating budget and and not an even dollar amount. On that fund expenditures are greater than reported causing a (deficit) on the fund. 534508 also has a PBIL without an even dollar amount, but in this case PBIL is greater than or equal to the Operating Budget. This is an indication that there was a carryover of funds from another fund. All AIS’s are rounded to the dollar with the exception of AIS’s that carryover funding. NIH or other Federal Letter of Credit(LOC) funds with any Receivable value Since Penn draws down funds as it expends them on LOC funds, there should never be a receivable of any amount on the fund. If there is, Research Services should be contacted. Expired Corp. Research/Clinical Trials with cash balances:Negative Receivables If theCorporate Research/Clinical Trial is finished you should follow the SOP for Clinical Trial Residual Balance Tranfers. IN SUMMARY The ORG Summary Report provides a quick status of all active grant funds for which the ORG is the RESP ORG. Separate tabs are provided to identify grants sorted by fund, PI, Account End Date, Receivables only, Overdrafts only, funds due to freeze in the next 90 days, analysis of expired funds, funds with illegal object code charges, late FSR’s, and a comparison of budgeted payroll to actual payments. To monitor for activity on funds for which your ORG is not the RESP ORG, subbudgets.rep can be run. For specific fund detail, the fundsummary.rep can be run.

Monthly Monitoring – Business Objects Fundsummary This an example of the fundsummary report for the first fund listed on ORG 4108’s ORG Summary Report. Observations to be made: The fund was reported on 5/27/1999. Res Svcs sets the Fin. Rpt Due date = to Last Fin. Rept File when a final report gets issued. Although the fund shows a Budget Balance Available(BBA), the fund is really in overdraft because Res. Svcs. has set Special Object PBIL to the reported amount. PBIL controls Revenue Recognition and Expense now exceeds Revenue. FSRD and FSRI represent the Direct and Indirect Costs reported to the sponsor. The fund is frozen for C forms, Feeder Systems, Journal Entries, Accounts Payable, and Purchase Orders.

Monthly Monitoring – Business Objects Fundsummary Key to further detail of amounts using Business Objects Reports * Payroll.rep or fund detail.rep # DETAIL OBJECT RPT.rep (one object code at a time) DETAIL RPT.rep (all object codes except payroll, E.B. and F&A costs) fund detail.rep @ DETAIL OBJECT RPT(Special Bdgt).rep O DETAIL OBJECT RPT(Operating Bdgt).rep E Encumbrances(Fund).rep $ DETAILOBJRPTCASH.rep