Download

1 / 14

140 likes | 292 Views

VAT and Capital Projects. Why overlooking VAT is bad in the early stages Hidden financial variable too optimistic creates risk too pessimistic degrades the business plan Credibility Degrades quality of funding targets Affects basis of application vat-exclusive applications vat-inclusive app

E N D

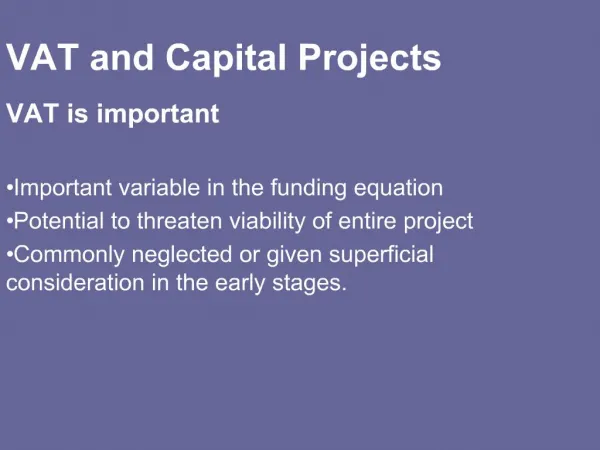

1. VAT and Capital Projects VAT is important

Important variable in the funding equation

Potential to threaten viability of entire project

Commonly neglected or given superficial consideration in the early stages.

2. VAT and Capital Projects Why overlooking VAT is bad in the early stages

Hidden financial variable

too optimistic creates risk

too pessimistic degrades the business plan

Credibility

Degrades quality of funding targets

Affects basis of application

vat-exclusive applications

vat-inclusive applications

Hinders pro-active planning

Business plans and applications

3. VAT and Capital Projects Technical Issues

Basic Assumption:

Standard-rate VAT will be due on the whole project

Only 2 ways to gain relief:

Zero-rating � avoiding being charged VAT

VAT recovery � reclaiming through VAT Returns

4. VAT and Capital Projects Zero-rating

New charitable buildings

Parts of new charitable buildings

Annexes to charitable buildings

Parts of Annexes to charitable buildings

Alteration work to listed charitable buildings

Certain types of work to aid access and facilities for the handicapped

New residential buildings

5. VAT and Capital Projects Zero-rating � conditions

New building definition

Charitable building definition

Annexe definition

Protected building definition

Alteration work definition

Residential building definition

Conditions for relief re: handicapped facilities/access

Scope of Zero-rating

6. VAT and Capital Projects Zero-rating

Certificates

transfers legal responsibility

civil penalties for the Charity

builders reluctance

The 10 year rule

change of use within 10 years

business definition

need to understand the rules well

monitoring protocols

7. VAT and Capital Projects VAT Recovery

VAT Registration

Never straightforward for Charities

Basic principles of VAT

taxable supplies � recoverable

exempt supplies � non-recoverable

non-business activities � non-recoverable

Use of building is critical

Mixed use � partly recoverable

need for methods and negotiation

8. VAT and Capital Projects VAT Recovery

It is critical to carry out a detailed analysis at the outset

Credible forecasts

Range of options with numbers

Greater structural and practical flexibility

VAT-smart business plans and applications

Credibility

presentation to HMRC

Work depends on complexity

9. VAT and Capital Projects VAT Recovery � Detailed analysis

VAT treatment of proposed uses

HMRC policy

VAT Law

Historic practise, changes in practise

Relationship of uses to building

floor area

cost profile

VAT Status of Charity

historic practise (especially treatment of proposed uses)

review trigger

skeletons and jewels

10. VAT and Capital Projects VAT Recovery � Detailed analysis

VAT Recovery forecast eg range 35-85%

VAT Strategic Options

liability options

activity options

space options

status

structure

Numbers on options

Formation of refined VAT strategy

11. VAT and Capital Projects VAT Recovery � Detailed analysis

Formation of refined VAT strategy

practical

legal

likelihood of success

implementation cost

timetable of actions

12. VAT and Capital Projects VAT Management process

HMRC rulings

hypothetical reluctance

written ?

unequivocal ?

base on full knowledge of the facts

definitely provisional

Other forms of assurance

authorised reclaims

VAT assessments following visits

3 year rule

specialist support and advice

13. VAT and Capital Projects VAT Management process

Detailed Analysis

VAT recovery forecast range

VAT strategic options

Strategy formation

consideration and formation

timing and implementation strategy

Strategy Implementation

VAT status, registration

Contractors, Architects

Business plans, applications, forecasts

HMRC

14. VAT and Capital Projects VAT Management process

Initial scoping VAT review

If the issues are not complex or contentious the scoping review should confirm that fact.

Detailed Analysis

VAT forecast

Strategic VAT options.

Consider the Strategic VAT options and form a refined VAT strategy.

Implement the VAT Strategy.

Alun Mathias

VAT Capital

02920 623655

alunmathias@vatcapital.co.uk