Download

1 / 17

200 likes | 930 Views

Captive Insurance. What is a Captive Insurance Company?. It is an insurance company Limited-purpose, wholly owned entity whose primary function is insuring exposures and risks of parent, designated affiliates or subsidiaries.

E N D

What is a Captive Insurance Company? • It is an insurance company • Limited-purpose, wholly owned entity whose primary function is insuring exposures and risks of parent, designated affiliates or subsidiaries. • Separate legal entity, generating financial statements, conducting all business usual and customary to any corporation registered in a domicile.

Benefits of a Captive Coverage availability: Captive owner has greater flexibility than with cost cap or finite options in design of insurance program coverage. Cost efficiencies: Typical commercial insurers premiums have expense ratios of 30-40% of premium, including profit and loss provision.. Captives expense ratios are 10-15%, or less. Investment: Captive has greater flexibility over cost cap or finite in selection of investment manager and choice of investments.

Benefits of a Captive (cont.) Reinsurance costs: Captive has access to higher limits at lower cost by purchasing limits directly from reinsurers. Tax savings: With a captive, the entire premium is tax deductible. Captive structure allows accelerated deduction for losses (captive is able to establish reserves for the majority of ultimate projected losses on its income statement rather than when losses are paid).

Benefits of a Captive (cont.) Greater control: Captive owner determines what risks are covered, retentions, limits, and when premiums are paid. (Whereas the finite program provides a guaranteed investment return, a finite’s investment and inflation assumptions are typically more conservative than prevailing market yields would justify.) Reduced fees: No excess and surplus lines tax of cost cap program, reduced broker fees.

Key Decision Factors • Formation time: Captive feasibility study required. Captive must be incorporated and established as required by domicile. • Operating costs: In addition to start up costs, domiciles require legal filings, auditing and other professional reporting/filing on an annual basis. • Capitalization of captive: Domiciles mandate capitalization requirements. • Risk sensitivity to adverse loss experience: Captive less sensitive. • Acceptability to regulators: Captive structure might confuse regulators. “Fronting” mitigates this.

Types of Captives • Single parent • Group • Protected cell • Rent-a-captive

Single Parent Captive This form of the captive has the greatest degree of program control: • Underwriting terms (coverages, premiums, payment schedule) • Accrual of investment income • Parent company has flexibility on purchase and renewal of reinsurance programs.

Who forms Single Parent Captives? • Medium to large companies with predictable schedule of losses, focused risk management objectives and strong risk mitigation programs in place. • Ideally suited for markets where commercial insurance is perceived to be overpriced relative to risk profile. • A captive should be considered a long-term commitment by the entity responsible for structuring it.

Captive legal authority • Numerous foreign countries and many U.S. states have enacted captive legislation to attract banking and corporate business necessary to support captives. • Captives can be formed offshore or onshore. Most popular offshore domicile is Bermuda. Most popular onshore captive is Vermont. These two domiciles are credited with 28% and 10% of the worldwide captive market, respectively. Total number of captives incorporated in all domiciles: >4,000.

Captive domiciles Domiciles have developed unique expertise to support certain classes of business risks. For example: Cayman Islands: Health care. Bermuda: Derivatives, reinsurance, ART. Bermuda allows captives for environmental liabilities. Vermont: Popular with companies that do not want to leave U.S. Vermont will allow captives for environmental risks.

How to select captive domicile • Regulatory authority: Review jurisdiction’s rules and regulations to find best fit for captive owner. • Legal framework: Jurisdiction needs to be captive-friendly. • Infrastructure: Proximity to resources necessary to make a captive operate efficiently – reinsurance markets, banking and investment choices, tax treatment, professional services.

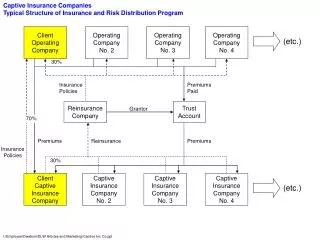

Considerations in structuring captives • Analysis of which (or all) elements of the transaction that are best suited to captive structure. • Proper use of “fronting arrangement” or “reinsurance”. • Management of captive • Tax implications

Reinsurance versus insurance A captive is structured to pre-fund “working layer” of expected losses. For cost exposures above that, the captive purchases insurance directly from reinsurance company. In general, due to the working layer of loss in a captive, the cost of reinsurance is lower than comparable cost cap commercial insurance (which includes cost of insurance and reinsurance).

Tax implications of a captive The most important tax question for a captive owner is whether the entire amount paid to the captive is treated as premium and is therefore tax-deductible. Two important considerations in establishing deductibility: • extent to which there is risk shifting, and • extent to which there is risk pooling. All funds paid out in claims are tax deductible eventually. Issue is the timing of the deduction.

Principal criteria for determining deduction • “Unrelated business” rule: either 30-50% unrelated business risk in the captive, or • Ownership: Ownership structure of the parent and its operating subsidiaries in relation to the captive (subs shouldn’t have ownership interest, parent can; must be arms length insurance contracts and subs can not simply be branches of the parent). • For deductibility avoid: financial guarantees between captive and owner; insufficient capitalization; noncommercial agreements between captive and parent; and, covering risks passing directly from parent rather than from subs.

Further assurance of tax-deductibility of a captive • Captive must be regulated in its domicile as an insurer. • Loss reserves must be reasonable. • Risks should be pooled within the captive—not separate accounts for each subsidiary contributing premium and business to the captive