Download

1 / 13

130 likes | 155 Views

Explore the methodology, challenges, and solutions related to actuarial valuations for captive insurance companies. Learn about risk models, third-party support, old and new business considerations, and the truths and fictions surrounding captives.

E N D

Actuarial Considerations for Captive Insurance Companies Presented by Allan P. Harris September 11, 2007

Why do we perform captive actuarial valuations in-house? • Develop expertise, cost efficiency over long term • Better understand our data by getting dirty with it

What lines • AL, GL, WC • EE benefits (LTD, GTL) – for now, relying on carriers w/benefits consultant oversight; long-term goal is to develop in-house expertise • Management liability (PL, Bond, D&O, Fiduciary, Employment Practices) – increasing number of data points, still not enough for full-blown actuarial conclusions, rely on combination of actual loss history & market pricing to set our premium rates and reserve levels

Methodology • Casualty: all info is captured in RMIS (Stars) • Triangles are developed • For Work Comp, separate CA & Non-CA • Separate triangles for major acquisitions • Separate triangles for pre-merger, old WFC work comp (completely different development patterns) • Year-over-year and ultimate development factors are computed • For forecasting and premium setting, use industry published law level and inflation factors

Uses • Set premiums for captive • Determine adequacy of reserve levels • Weigh quotes from (re)insurers

ISSUE: Standard triangle and loss development method is incomplete, as it does not price the cost of capital of retained risk, i.e. the potential earnings hit from a large outlier loss within retained limits SOLUTION: Risk models that weigh the probability of various loss levels against the associated costs of risk transfer CHALLENGE/OPPORTUNITY: Risk management departments need to develop (or outsource) this expertise

Third-party Support? • KPMG certifies reserves in conjunction with the audit as required by domicile (Vermont) • Many years ago we had an independent actuarial review, with strong confirmation of our methodology and results

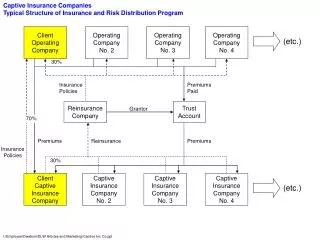

Old Business • Concentric Risk Integration program • Multi-year, multi-line – given the spread of risk with “black hole” deductibles and aggregate retention, allowed reasonable estimate of exposure based on loss history (more or less actuarial) • Reinsurers are no longer interested in writing this business – not interested in risk transfer in this working layer

New Business • Employee Benefits – Long-term Disability and Term Life • Pro: Predictable cost; risk diversification • Con: Catastrophe correlation (Life) with other captive lines (WC, Property) • Other – e.g. Lender Placed Hazard, Crop Insurance (and large deductible management liability) • Pro: Profitable business; risk diversification • Con: Large cat exposure

ISSUE: Deterministic actuarial models (mine) fail to alert management to size and probability of significant loss SOLUTION: Need new tools employing stochastic, random methodology, e.g. Monte Carlo models CHALLENGE/OPPORTUNITY: Need new technical and interpretive skills, software, large amounts of data

Captives : Truth and Fiction • Truths • Eliminates third-party insurers’ margins (partially the result of subsidizing companies with poorer risk profiles) • Retains cash flow benefits • Allows direct control of administrative and claims handling fees • Access to cheaper reinsurance market • Avoid cyclical hard/soft markets or coverage unavailability • Internally, can eliminate volatility for business lines • Promotes aggregation and analysis of risks

Captives : Truth and Fiction • Fictions • Tax breaks – Same deduction exists from simply buying insurance (captive deduction is less, as IRS requires discounting of captive reserves to calculate the tax deduction); savings derive from reducing commercial insurer profits, not tax breaks • Reinsurance of employee benefits puts parent company employees’ benefit programs at risk – No –the insurers, whether in a fronting or insuring position, remain on the hook for these liabilities if captive cannot meet its reinsurance obligations

Contact Information: Allan P. Harris Wells Fargo www.Allan.P.Harris@wellsfargo.com