Download

1 / 6

60 likes | 197 Views

This article explores the concept of contribution analysis in multi-product firms, focusing on how different products contribute to fixed and indirect costs. It discusses the importance of a product covering its direct costs, the role of contribution pricing for decision-making, and how businesses can manage their product portfolios. The concepts of cost and profit centers are examined, detailing their advantages and disadvantages, including accountability, efficiency, and potential conflicts. This guide offers insights on optimizing resource allocation and enhancing profitability in large organizations.

E N D

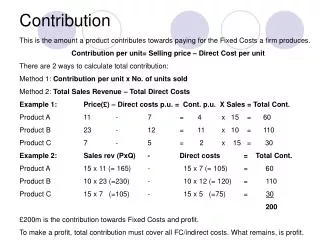

Contribution analysis for multiproduct firms • In a multi product firm a business will have many different products that contribute to paying indirect or fixed costs • If a product does not make a profit but contributes to paying indirect costs the business will most likely continue with the product. • The key is that the product covers it’s direct costs. • Profit = total contribution – (TFC + overheads)

Contribution analysis uses: • Contribution pricing – helps to see how much sales of a product help to pay fixed and indirect costs • Product portfolio management – allows a firm to give products with high contributioninvestment priority. Also products with a low contribution need to have high volume or will be withdrawn and replaced. • Allocation of overheads to cost and profit centers – costs are distributed fairly • Make or buy decisions – businesses need to decided on if it is better to make a product themselves or buy it from a supplier (outsource) • Special order decisions are helped – this refers to when a customer offers a higher price but wants special treatment (quick delivery or added credit) or gives a lower price because they are buying volume. Contribution analysis will help a business to determine if the special order is worthwhile.

Cost and Profit centers • When businesses become large different sections of a business can be divided into either sections responsible for watching costs or increasing revenue. • Cost centers are sections of a business that are in charge of monitoring and lowering costs for a business. They will not be in charge of making a profit. • Profit centers are sections of a business that usually have a large product portfolio. They will help a business to figure out how much profit certain sections make. Banks will use these to dived the different products they have like insurance, mortgages, commercial loans. • Franchisees will use each store as a profit center.

Advantages of cost and profit centers • Helps accountability for their departments contribution to paying fixed costs. The cost centers can easily move the direct costs to where they belong. • It helps to determine which sections of a business are profitable. If a large business is profitable on the whole then a section that is unprofitable may be hard to notice without centers • Costs can be spread easily to the profit or cost center then they can be more easily allocated • Better team sprit can be achieved within a cost or profit center where as businesses that do not use them can be disorganized and demotivated. • Benchmarking the best profit center will sometimes make the other centers more efficient • Delegation to the managers of profit and loss centers can help to motivate people. This can also help by rewarding the best profit and cost centers.

Disadvantages of cost and profit centers • Accurately allocating costs can be very subjective (same as full cost and absorption pricing) • A change in the allocation of fixed costs can cause an apparent decrease in profits for a center but that does not really mean that they have made less profit from trading. • External factors (rise in supply costs, change in interest rates) can cause a profit center to look like there is a problem when it is not really their fault. • Data collection can be expensive • Conflict and competition between profit and cost centers can arise. • Staff and mangers can become stressed and this can be demotivating. The need to raise revenue while decreasing cost can be overwhelming. • Cost and profit centers will be less likely to think of Corporate Social Responsibility than the overall company because of the need for profit

Appropriating overheads to cost and profit centers • Full costing is based on a single criteria such as output, sales revenue, floor space, employees or capital equipment used. • Absorption to a cost or profit center is the extension where individual costs are allocated to departments depending on individual criteria. (is considered more accurate)