Effective Interest Bond Amortization

Effective Interest Bond Amortization. Prepared for Accounting 212 Summer 2010. What are Bonds?. Bonds are interest-bearing notes issued by corporations, universities and governmental entities. Usually sold to many investors.

Effective Interest Bond Amortization

E N D

Presentation Transcript

Effective Interest BondAmortization Prepared for Accounting 212 Summer 2010

What are Bonds? • Bonds are interest-bearing notes issued by corporations, universities and governmental entities. • Usually sold to many investors. • Are traded, like stocks, on open markets where the price is determined by the market interest rate. Interest is the cost incurred by the bond issuer for the use of the investor’s money. • The face value is the amount of principal the bond issuer must pay at the maturity date.

Interest Rates: Stated vs. Market • Each bond has a contractual, or stated rate of interest (ex: 5% per year). This rate may be higher or lower than the prevailing interest rate, determined on the open market. • If the market interest rate is less than the stated rate, investors will equalize the difference by purchasing the bond at a higher price. The difference between the higher market price and the face value of the bond is called a premium. • If the market interest rate is greater than the stated rate, investors will equalize the difference by purchasing the bond at a lowerprice. The difference between the lower market price and the face value of the bond is called a discount. • For accounting purposes, we must calculate and journalize (record) both the interest expense and the discount or premium. Amortization is the process of allocating the discount or premium over the term of the bond.

Amortization of Premium or Discount • Two types of amortization include: • Effective-Interest: the periodic interest expense equals a constant percentage the carrying value of the bond. • Straight-line: The same amount of interest expense of interest expense is allocated in each period. • Let’s illustrate the Effective-Interest method.

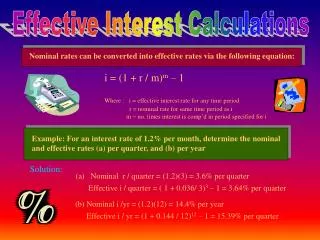

Effective-Interest Method • First, assume a bond with a face value of $100,000, a stated interest rate of 10% and a 5-year term. Interest is paid semi-annually (twice a year). • Next, assume that the market interest rate is 12%. Using a present value table, the investor compensates for the lower stated interest rate by paying $92,639 (the carrying value). Thus, the total discount to amortize is: • $100,000 - $92,639 = $7,361

Effective-Interest Method - Discount There are three computations to make: • Compute the bond interest expense: carrying value X effective-interest rate • Compute the bond interest paid: face value X stated (contractual) rate • Compute the amortization: difference between two steps above Then, ADD the amortization from the current carrying value to get the carrying value for the next period Repeat the process for each interest period

Effective-Interest Method - Discount The journal entry on the first interest date is: Bond Interest Expense 5,558 Discount on Bonds Payable 558 Cash 5,000 What is the entry on the second interest date?

Effective-Interest Method - Discount The journal entry on the second interest date is: Bond Interest Expense 5,592 Discount on Bonds Payable 592 Cash 5,000 Now, let’s do the computations for a premium!

Effective-Interest Method • First, assume a bond with a face value of $100,000, a stated interest rate of 10% and a 5-year term. Interest is paid semi-annually (twice a year). • Next, assume that the market interest rate is now 8%. Using a present value table, the investor compensates for the higher stated interest rate by paying $108,111 (the carrying value). Thus, the total premium to amortize is: • $108,111 - $100,000 = $8,111

Effective-Interest Method - Premium There are three computations to make: • Compute the bond interest expense: carrying value X effective-interest rate • Compute the bond interest paid: face value X stated (contractual) rate • Compute the amortization: difference between two steps above Then, SUBTRACT the amortization from the current carrying value to get the carrying value for the next period Repeat the process for each interest period

Effective-Interest Method - Premium The journal entry on the first interest date is: Bond Interest Expense 4,324 Premium on Bonds Payable 676 Cash 5,000 What is the entry on the second interest date?

Effective-Interest Method - Discount The journal entry on the second interest date is: Bond Interest Expense 4,297 Premium on Bonds Payable 703 Cash 5,000 The effective-interest and straight-line methods produce different results. If the difference is material, the effective-interest method must be used.