Download

1 / 4

40 likes | 49 Views

Taxguru provides with the Latest Goods and Services tax news, updates, articles, etc..

E N D

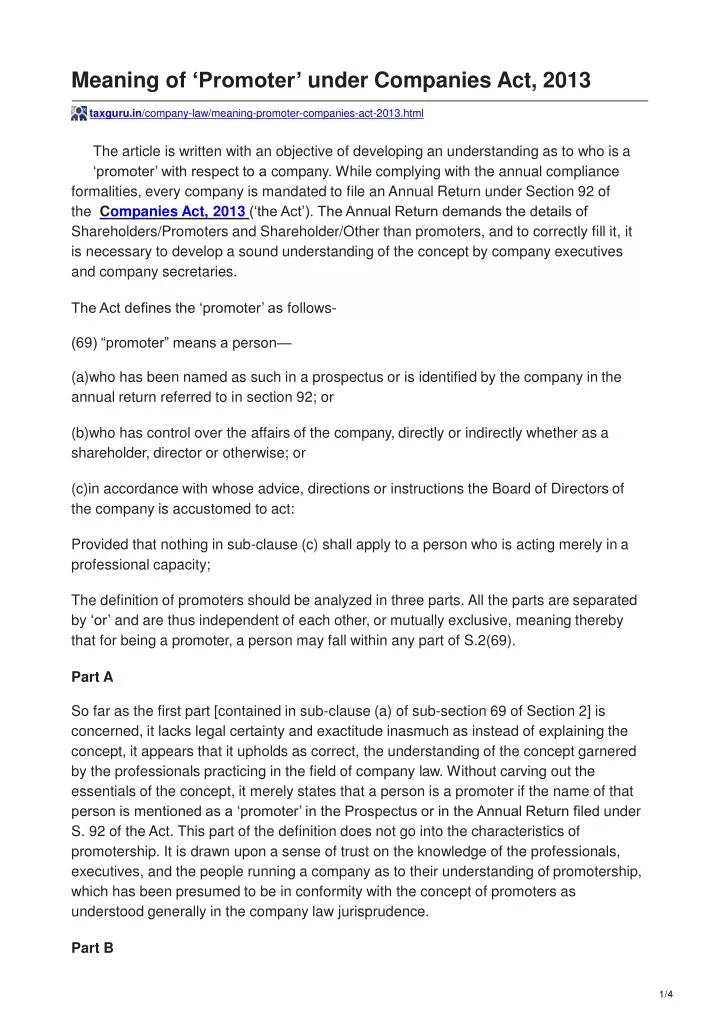

Meaning of ‘Promoter’ under Companies Act,2013 taxguru.in/company-law/meaning-promoter-companies-act-2013.html The article is written with an objective of developing an understanding as to who isa ‘promoter’ with respect to a company. While complying with the annualcompliance formalities, every company is mandated to file an Annual Return under Section 92 ofthe Companies Act, 2013(‘the Act’). The Annual Return demands the details of Shareholders/Promoters and Shareholder/Other than promoters, and to correctly fill it, it is necessary to develop a sound understanding of the concept by company executives and companysecretaries. The Act defines the ‘promoter’ asfollows- (69) “promoter” means aperson— who has been named as such in a prospectus or is identified by the company inthe annual return referred to in section 92;or who has control over the affairs of the company, directly or indirectly whether asa shareholder, director or otherwise;or in accordance with whose advice, directions or instructions the Board of Directorsof the company is accustomed toact: Provided that nothing in sub-clause (c) shall apply to a person who is acting merely ina professionalcapacity; The definition of promoters should be analyzed in three parts. All the parts areseparated by ‘or’ and are thus independent of each other, or mutually exclusive, meaning thereby that for being a promoter, a person may fall within any part ofS.2(69). PartA So far as the first part [contained in sub-clause (a) of sub-section 69 of Section 2] is concerned, it lacks legal certainty and exactitude inasmuch as instead of explaining the concept, it appears that it upholds as correct, the understanding of the concept garnered by the professionals practicing in the field of company law. Without carving out the essentials of the concept, it merely states that a person is a promoter if the name of that person is mentioned as a ‘promoter’ in the Prospectus or in the Annual Return filedunder S. 92 of the Act. This part of the definition does not go into the characteristics of promotership. It is drawn upon a sense of trust on the knowledge of the professionals, executives, and the people running a company as to their understanding ofpromotership, which has been presumed to be in conformity with the concept of promoters as understood generally in the company lawjurisprudence. PartB

Moving on to the second independent leg of the definition of ‘promoter’, we find a little objectivity in the definition, as it hinges on the presence of one’s control over the affairs of the company as a prerequisite for being classified as a promoter. Such control may arise out of the position of that person as a shareholder, or a director or otherwise. Interestingly, the definition also contemplates a person who may neither be a shareholder nor a director, and yet be a promoter if he has control over the affairs of the company (However, the nature of such a promotership is a subjectmatter of further deliberation). And at the same time, every shareholder or director need not be treated as promoter of the company if he does not exercise any control over the affairs of the company. In this context, it is notable to refer to the definition of ‘control’ as given in S. 2(27) of the Act. The definition is reproduced hereunder- (27) “control” shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any othermanner; The definition of control is an inclusive one meaning thereby that apart from whatis mentioned in the definition, there may be other facets of control. However,reading together the second leg of S.2(69) alongwith S.2(27), one gets clarity that if a person has a right to appoint the majority of directors or to control the management or policy decisions of a company, then he/she would be considered to a be a promoter. What may be classified as control over management and policy decisions can be yet anothersubject of academic debate andinterpretation. PartC The last part of the definition states that a promoter is a person – “(c) in accordancewith whose advice, directions or instructions the Board of Directors of the company is accustomed to act”. This is again vague and from the perspective of a person who is an outsider to the management of the company, this fact may not be evident very easily.It would be even more difficult to ascertain promoters falling under this category in thecase of private companies as the disclosure requirements in their case are not as rigid as that of public companies and listed publiccompanies. So, applying the rules of literal interpretation on S. 2(69) of the Act, and reading all the parts of the definition together, a person may be a promoter of the company even without being a director or a shareholder, if he/she has been named so in the Prospectus or Annual Return of the Company. Similarly, a person who has been stated to be apromoter in the prospectus of the company or the Annual Return of the Company, would be treated as a promoter even if he/she does not exercise any control over the affairs of the company or even if doesn’t has any right of appointment of majority of the directors. The strict interpretation of the definition is against the traditional understanding of the concept of promoters which is usually linked to significant shareholding in the company.

The status of a promoter comes with many responsibilities and compliances which are absent in the case of a mere shareholder. Thus, no one would practically agree or volunteer to be a promoter or claim to be promoter unless the consequent gains arisingto him/her are proportional to the responsibilities/ liabilities/ compliances imposed upon him/her under theAct. Another interesting aspect of this concept is that the promoters are not a sine qua non for a continued existence/sustenance of a company. Recently, Infosys founders approached SEBI for being re-classified as public shareholder rather than promoter shareholders of Infosys. In a similar move, Poddars, the original promoters of Gillette,got their reclassification as public shareholders approved from SEBI. Companies such as ITC, HDFC, L&T do not have any promoters as on today. For listed companies, Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957as amendedby Securities Contract (Regulation) (Third Amendment ) Rules, 2017(w.e.f., July 3, 2017 ) requires a minimum 25 per cent of public shareholding but there is no suchlegal requirement of minimum promoter group holding. [Here, it may be noted that when a promoter led company raises funds through a IPO, then it must maintain 20%minimum shareholding of the post-issue capital for a minimum period of three years therefrom. But in this case also, such requirement is only for a short period of time for fastening a sense of responsibility upon the promoters. See Securities and Exchange Board ofIndia (Issue of Capital and Disclosure Requirements) Regulations, 2009. In cases,where there is no identifiable promoter, even this requirement does notexist.] You may write you views, doubts, or questions in the Comments Section below oremail to [emailprotected] Tags: Companies Act, Companies Act2013 Kindly Refer to Privacy Policy & Complete Terms of Use andDisclaimer. AuthorBio Name: Shashank S.Mangal Qualification: LL.B /Advocate Company: SHASHANK MANGAL &CO. Location: DELHI, New Delhi,IN

Member Since: 16 Oct 2020 | Total Posts:2 I am a practicing Advocate in Delhi. My practice is mainly concentrated on theAppellate side. View FullProfile My PublishedPosts Director Remuneration- Not a RelatedPartyTransaction View More PublishedPosts More Under Company Law «PreviousArticle Next Article» Leave aComment Your email address will not be published. Required fields are marked*