Download

1 / 13

130 likes | 270 Views

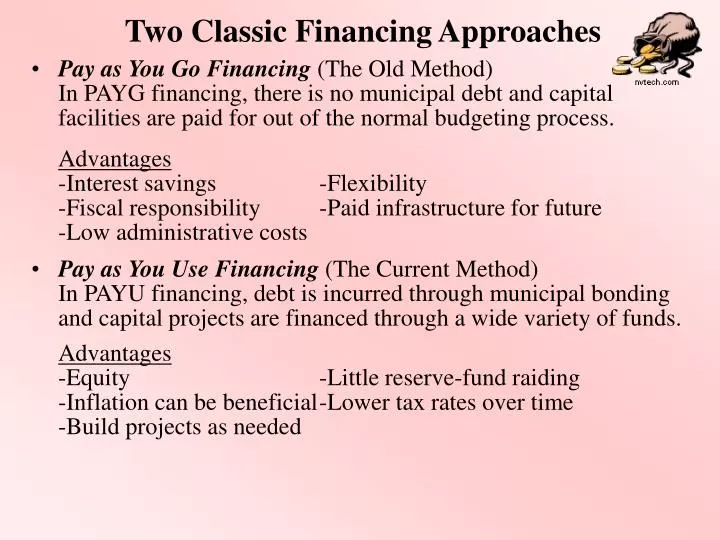

Two Classic Financing Approaches. Pay as You Go Financing (The Old Method) In PAYG financing, there is no municipal debt and capital facilities are paid for out of the normal budgeting process.

E N D

Two Classic Financing Approaches • Pay as You Go Financing (The Old Method)In PAYG financing, there is no municipal debt and capital facilities are paid for out of the normal budgeting process. • Pay as You Use Financing(The Current Method)In PAYU financing, debt is incurred through municipal bonding and capital projects are financed through a wide variety of funds. Advantages-Interest savings -Flexibility-Fiscal responsibility -Paid infrastructure for future-Low administrative costs Advantages-Equity -Little reserve-fund raiding-Inflation can be beneficial -Lower tax rates over time-Build projects as needed

Debt Financing • General Obligation (GO) Debt Financing • Backed by the “full faith and credit” of the jurisdiction • Usually paid back through property taxes • There are no limitations on the funds that have to be raised to pay for these bonds • Subject to constitutional/statutory limits • Normally require voter approval • Revenue Bond Debt Financing • Not backed by the “full faith and credit” of the jurisdiction • Secured by revenues of a given project • Credit quality depends on strength of underlying project • Credit quality is normally lower than for GO Bonds due to limited revenue streams • Usually not limited by constitutional/statutory limits • Usually do not require voter approval

Choosing a Debt Vehicle • General Obligation Bonds are appropriate for capital projects benefiting community as a whole. Examples: Libraries, Parks, Civic Centers • Revenue Bonds are appropriate when a specific, reliable, predictable, and sufficient revenue stream can be garnered from a project or financing mechanism.Example Projects: Parking Decks, Conv. Centers, Airport Terminals Example Mechanisms: TIF for CRAs, Impact Fees for Infrastructure • What factors influence the choice of debt type? • --Total cost of project • --Types of benefits of the project • --The timing of benefits of the project • --Probability of voter approval for GO bonds • --Availability of revenues from other sources • --Current debt situation (flexibility, available debt)

Debt Policy and Local Governments • States require local governments to have written policies that establish guidelines for the use of debt. • Included in this should be: • Maximum amount that can be issued • Purposes for which debt can be issued • Type(s) of debt allowed • Debt maturity structure and schedule--Schedule should not exceed the useful life of the project--Usually a single security, sold in $5,000 issues--Most GO bonds are serial bonds, with a variable maturity date--Revenue Bonds are usually term bond, with a single maturity date and a sinking fund provision • The ratio of GO to Rev Bonds has changed dramatically: 1950: $5 GO to $1 Rev 1984: $1 GO to $3 Rev (Pre 1986 Tax Reform Act) 1993: $1 GO to $2 Rev (Post 1986 TRA)

Other Debt Financing Terminology • Other Long-Term Financing Vehicles--Double-barreled bonds (backed by FFC and other defined source) --Special assessment bonds (backed by special assessment) • Short-term Notes--BANs (Bond anticipation notes) --TANs (Tax anticipation notes) --RANs (Revenue anticipation notes) --GANs (Grant anticipation notes)Each of these is issued in the short term (less than 13 months) to smooth out government cash flow. • Arbitrage: Refers to the tax free interest nature of municipal bonds. • Arbitrage Bonds: Taxable bonds that require the reporting of interest income for federal tax purposes. • Callable Bond: The bond issuer has the option to “call in” bonds on a certain date, pay them off, and then resell the bonds at a lower rate. • Put Bond: The bondholder has the right to sell (or put) back to the issuer at a fixed price.

Tax Aspects of Municipal Bonds • Interest Income on municipal bonds is exempt from federal income taxes. Many states also exempt this income from state taxes. This makes them VERY attractive investments to groups in higher tax brackets. • For example, for someone in the highest tax bracket (31% tax rate in the old days) a municipal bond with a yield of 5.52% is equivalent to a 8% yield from a taxable security. • The Tax Reform Act (TRA) of 1986 changed the rules substantially: • Tax exempt “Muni” bonds represent lost income for the Federal Gvt. • The TRA limited the issuance of private purpose bonds; A bond is private purpose if: 1) Non-governmental groups use 10% or more of the bond proceeds or 2) 10% or more of the bond is secured by private property or revenues • Repealed tax exempt status of many bond types (IDB’s, stadia, etc.) • In general, spelled out much more clearly those bond purposes that were public and private, effectively tightening what local governments could do with tax exempt bonds.

Issuing Debt in the Market • Bonds are sold to investors in a Bond Market. These bonds are sold via a three stage process: • Origination: Most governments use an independent financial advisor who prepares primary documents (Official Statement and Notice of Sale), reviews the financing structure, and is involved in marketing the bonds. • Underwriting: Sale of Bonds occurs in one of three ways: • Private Placement (not used for Public Offerings) • Competitive Bidding (used for Public Sale) • Negotiation (used for Public Sale) Fees are paid to sellers (underwriters) in this process.The choice of method depends upon the size and complexity of the issue, the credit quality of the issuer, and market conditions. • Distribution: The distribution of bonds and payments to buyers. Obviously these must be closely tracked.

Key Players in the Bond Game • Underwriters/Bond Houses: These actors work with city officials to structure the deal and prepare the official statement. They are very interested in seeing a deal go through because they get paid a percentage of the proceeds. • Bond Counsel: Lawyers who work out the technicalities of a deal. They insure that a bond is structured so that it is tax exempt. (also share in the proceeds) • Ratings Agencies/Bond Insurers: Standard and Poor’s and Moody’s are the main players. They assess a bond and rate the bond according to various factors. They also can be called upon to insure the bond (guaranteeing payment) thereby raising the bond rating and lowering the interest rate. • Bond Buyers: Purchasers of bond issues. In the “old days” wealthy families. Now this market is dominated by large institutional investors who buy bonds in bulk.

Credit Quality and Bond Ratings • Credit Quality is VERY important to local government. Governments are typically rated by Standard and Poor’s, Moody’s, and Fitch’s. Better credit ratings lead to lower interest rates. • Debt Burden Very General Rules of Thumb Debt should not exceed: • 10% of Assessed Value - 15% per capita personal income • 20% over previous year - 90% authorized by state law • Other important factors in Credit Quality include: • Budgetary Soundness - Tax Burden • Overall Economic Conditions - Flow of Funds Structure • Covenants • Municipal bond defaults occur when a city makes known that they simply cannot pay their debt. These are disastrous! Drives the credit rating down and the interest rates up and generally make it much more difficult for a government to borrow money.

Indicators of Tallahassee’s Credit Quality Debt Service as a Percentage of General Government Expenditures Debt Service per Capita

Philly & DC The Bond Ratings Breakdown = Florida Bond Ratings = Tallahassee Bond Ratings

Bond Ratings Cont’d • Ratings for given issues occur on two levels: 1) “Issue” creditworthiness--Likelihood of payment: the capacity and willingness of the obligor to meet its financial commitment--Nature of and provisions of the obligation; --Protection afforded by, and relative position of, the obligation in the event of bankruptcy, reorganization, or other arrangement 2) “Issuer” creditworthiness --This focuses on the obligor's capacity and willingness to meet its financial commitments as they come due. --It does not apply to any specific financial obligation Example: City of Tallahassee’s Affordable Housing Fund • Municipalities can acquire Bond Insurance or Bank Letters of Credit to improve the marketability and lower the interest rates of a bond issue.