Interpolation Calculations

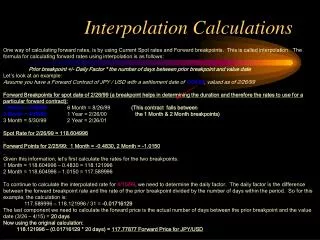

Interpolation Calculations. One way of calculating forward rates, is by using Current Spot rates and Forward breakpoints. This is called interpolation. The formula for calculating forward rates using interpolation is as follows:

Interpolation Calculations

E N D

Presentation Transcript

Interpolation Calculations One way of calculating forward rates, is by using Current Spot rates and Forward breakpoints. This is called interpolation. The formula for calculating forward rates using interpolation is as follows: Prior breakpoint +/- Daily Factor * the number of days between prior breakpoint and value date Let’s look at an example: Assume you have a Forward Contract of JPY / USD with a settlement date of 4/15/99, valued as of 2/26/99 Forward Breakpoints for spot date of 2/26/99 (a breakpoint helps in determining the duration and therefore the rates to use for a particular forward contract): 1 Month = 3/26/99 6 Month = 8/26/99 (This contract falls between 2 Month = 4/26/99 1 Year = 2/26/00 the 1 Month & 2 Month breakpoints) 3 Month = 5/30/99 2 Year = 2/26/01 Spot Rate for 2/26/99 = 118.604996 Forward Points for 2/25/99: 1 Month = -0.4830, 2 Month = -1.0150 Given this information, let’s first calculate the rates for the two breakpoints: 1 Month = 118.604996 – 0.4830 = 118.121996 2 Month = 118.604996 – 1.0150 = 117.589996 To continue to calculate the interpolated rate for 4/15/99, we need to determine the daily factor. The daily factor is the difference between the forward breakpoint rate and the rate of the prior breakpoint divided by the number of days within the period. So for this example, the calculation is: 117.589996 – 118.121996 / 31 = -0.01716129 The last component we need to calculate the forward price is the actual number of days between the prior breakpoint and the value date (3/26 – 4/15) = 20 days Now using the original calculation: 118.121996 – (0.01716129 * 20 days) = 117.77877 Forward Price for JPY/USD