Download

1 / 42

420 likes | 569 Views

Extending Aggregate Supply. Previous Assumption. Shift in AD no effect AS Actuality “long-term”: AD up price level up lower real wages negotiate higher nominal wages to restore real wage left shift in AS Real wage: Nominal/price index (as decimal) $10/1.0= $10 $10/2.0=$5

E N D

Previous Assumption • Shift in AD no effect AS • Actuality “long-term”: AD up price level up lower real wages negotiate higher nominal wages to restore real wage left shift in AS • Real wage: Nominal/price index (as decimal) • $10/1.0= $10 $10/2.0=$5 • Review Determinants of AS: • 1) Input prices (domestic resources, imported resources, market power) • 2) Productivity • 3) Legal-institutional environment (taxes, regulations)

Short-Run / Long-Run • Short-run: “a period in which nominal input prices remain fixed as the price level changes” • 1) Resource providers may be unaware of extent of price change no adjustment of supply/demand • 2) Contracts • Long-run: “a period in which nominal wages are fully responsive to changes in the price level”

Short-Run AS • 1) Initial price level is P1; 2) nominal wages set on expectation this price level will persist; 3) price level flexible up and down • a1 at price level P1 is Qf, natural rate unemployment

AS a2 PL2 a1 PL1 a3 PL3 Q3 Qf Q2

P2: increased revenues, fixed wages higher profits increase output (above Qf, below natural rate U) • P1: reduced revenues reduced profits lay-offs reduce output (below Qf, above natural rate U)

Long-Run AS • P2 initially increases output, but demands for higher nominal wages (now expect P2 will continue) fall back to Qf • P3 initially decreases output, but bosses negotiate lower nominal wages (now expect P3) rise back to Qf

ASLR ASsr a2 b1 PL2 a1 PL1 a3 c1 PL3 Q3 Qf Q2

Equilibrium in Extended AS-AD ASsr ASlr PL a AD Qf

Short-run AS positive slope: nominal wages constant • Long-run AS vertical: nominal wages adjusted • Equil GDP + price level: intersection AD, ASlr and ASsr

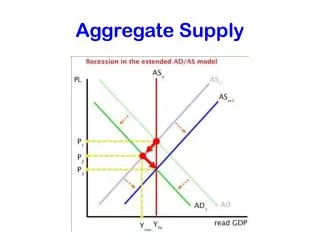

Applying Extended AS-AD Model • 1. Demand-pull inflation (AD up PL up) ASsr ASlr PL2 PL a AD2 AD1 Qf

ASsr2 ASlr ASsr1 c P2 b P a AD1 Qf Q2 p334

Short-run: d-p i P and real output up • Long-run: movement along ASlr • Economy can only exceed Qf for short time before renegotiating prices back to Qf

2) Cost-Push Inflation ASsr2 ASsr1 ASlr b P2 P a Shift is cause of price change (in d-p I is result) AD Q2 Qf

Policy Dilemma • W/o expansionary policy AD doesn’t shift output decline (recession) • BUT, expansion further inflation • AND, negotiate higher nominal wages left shift AS higher inflation, and so on • Do nothing? Recession lower demand resources falling prices undo initial AS shift

Generalizations • 1) Attempt to maintain full employment in cost-push inflationary spiral • 2) Hands-off recession that eventually corrects (at cost of higher unemployment and loss of real output)

3) Recession • Most controversial • Suppose investment spending dramatically declines AD shifts left • IF prices downwardly flexible, PL falls higher real wages AS shifts left lower nominal wages AS shifts right equilibrium at lower price level • No need for fiscal or monetary policy

ASsr1 ASlr ASsr2 P a b P2 AD1 P3 AD2 p335 Q2 Qf c

Disagreement: if adjustments forthcoming, only after extended period of recession/depression

The Phillips Curve • Suppose right shift in AD increase in P and Q decrease unemployment • Greater shift in AD even greater P, Q, and U changes • Smaller shift in AD smaller changes • Generalization: Assuming constant ASsr, high inflation accompanied by low U; low I accompanied by high U

Annual rate of inflation (%) Unemployment rate (%)

Tradeoffs • Tradeoff I and U “full employment without inflation” is impossible • Question is: where along Philips Curve do we want to be? • Expansionary: low U + high I • Contractionary: high U + low I • Fiscal/monetary policy moves economy along the curve in the short-run

Annual rate of inflation (%) 12 2 2 Unemployment rate (%) 9

Stagflation • Stable PC in 1960s highly unstable 1970s + 1980s • Inverse relationship became obscure and questionable • 1970s: high I + high U (stagflation) • At best: PC shifted higher levels of U and higher levels of I • At worst: no dependable relationship

Annual rate of inflation (%) 12 2 2 Unemployment rate (%) 9

Cause Stagflation? • Aggregate Supply Shock: rapid, significant increase resource costs leftward jolt AS • Cost-push Inflation undermines assumption of PC (stable AS)

Stagflation’s Demise • 1) deep recession ‘81-82: v. tight monetary policy (Paul Volcker) high U smaller increase nominal wages (bad job>no job) + firms kept prices down (hold onto diminished market share) • 2) Foreign competition • 3) Deregulation (Reagan) • 4) Decline OPEC monopoly power • right shift AS return to PC of 1960s

Natural-Rate Hypothesis • Explanation 1 of stagflation: PC still holds true, 70s+80s just abnormal • Explanation 2: no inverse relationship; economy is stable at natural rate (full employment) • U above or below NRΔ inflation • NAIRU

Adaptive Expectations Theory • Assumption: expectations about future inflation based on current inflation • Short-run tradeoff I and U, but not in long-run • Attempts to lower U below NR instability right shift in PC

PClr b1 6 a1 3 PCsr 4 6=NR

Movement consistent w/ AS-AD and original PC assumptions greater output at cost of higher inflation • Perhaps because expansionary policy because G misjudged natural rate • Adaptive Expectations: “When the actual rate of inflation is higher than expected, profits temporarily rise and unemployment rate temporarily falls.”

PClr Point B not stable b1 6 a1 3 PCsr 4 6

Nominal wages not increased as fast as inflation negotiate higher wages profits fall employment + output falls back to full employment at higher PL

PClr b1 6 a2 3 a1 PCsr2 PCsr1 4 6

Higher actual and expected inflation (6%) PCsr shifts • Movement along PCsr1 (a1 b1) long-run shift back to natural rate • G policy may continue upward movement of prices (if again misjudge causes)

G attempts to move along PC causes shift to less favorable position long-run Philips Curve showing levels of inflation at full-employment U • So society should choose low inflation over high

PClr b1 6 a2 3 a1 PCsr2 PCsr1 4 6

Disinflation • When the actual rate of inflation is lower than the expected rate, profits temporarily fall and the unemployment rate temporarily rises. • Fall in inflation fall in profits higher U negotiate down nominal wages U falls • PC shifts left, new equilibrium back at long-run PC

PClr a3 b1 c3 6 a2 PCsr1 3 a1 PCsr2 4 6

Rational Expectations Theory • Adaptive Expectations assumes people respond to changes, RE assumes f + h anticipate impacts of G and factor into their decision making • Result: if G policy fully anticipated no increase profit/output/employment but quick increase inflation • Both support conservative view that G policy typically fails

Shifts in Philips Curve • Expectations: in long-run expected inflation adjusts to changes actual inflation new level of I at NRU • Supply shocks