Double-Entry System

CHAPTER 5. Double-Entry System. Double-Entry System. The double-entry system is considered as the heart of modern accounting. All accounting systems operate on the basis of the double-entry system. Manual accounting system. Computerized accounting system. Double-Entry System.

Double-Entry System

E N D

Presentation Transcript

CHAPTER 5 Double-Entry System

Double-Entry System The double-entry system is considered as the heart of modern accounting. All accounting systems operate on the basis of the double-entry system. Manual accounting system Computerized accounting system

Double-Entry System The double-entry system provides checks and balances to ensure that your books are always in balance. In double-entry accounting, each transaction has two journal entries: a debit and a credit.

Double-Entry System Credits = Debits The sum of all debits should always equal the sum of all credits. Because debits equal credits, double-entry accounting prevents some common bookkeeping errors.

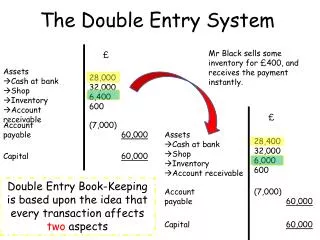

T Account The T account is the basic form of the double-entry system. Title of Account Left or Debit Side Right or Credit Side The rules of the double-entry system are that one transaction affects at least two accounts --- debit accounts and credit accounts.

Double-Entry System Accounting equation Assets = Liabilities + Owner’s Equity

Transaction Analysis Now, let’s analyze the transaction of George Ross Photocopy Company…

Transaction Analysis Transaction 1 March 3: Mr. George starts his photocopy company on March 1 with 20,000 us dollars that was immediately deposited into the bank. ? Increase or decrease Assets Owner’s equity Debited or Credited

Transaction Analysis Transaction 1 Cash at Bank $10,000 George Ross, Capital $10,000

Transaction Analysis Transaction 2 March 6: Rented another office, paying a year’s rent in advance, $4,800 by check. Increase or decrease ? Assets 1 Debited or Credited Assets 2

Transaction Analysis Transaction 2 Prepaid Rent $4,800 Cash at Bank $4,800

Transaction Analysis Transaction 3 March 7: Purchased photocopy equipment for $2,000 with cash. Increase or decrease Assets 1 ? Debited or Credited Assets 2

Transaction Analysis Transaction 3 Photocopy Equipment $2,000 Cash $2,000

Transaction Analysis Transaction 4 March 7: Purchased office equipment from Hougas Equipment Co. for $5,300, paying $2,300 in cash and agreeing to pay the rest next month. Assets 1 ? Increase or decrease Assets 2 Debited or Credited Liability

Transaction Analysis Transaction 4 Office Equipment $5,300 Cash $2,300 Accounts Payable 3,000

Transaction Analysis Transaction 5 March 8: Purchased on credit photocopy supplies for $2,300 an office supplies for $800 from Tim Supply Co. Increase or decrease Assets ? Liability Debited or Credited

Transaction Analysis Transaction 5 Photocopy Supplies $2,300 Office Supplies 800 Accounts Payable $3,100

Transaction Analysis Transaction 6 March 8: Paid $600 in cash for a one-year insurance policy with coverage effective March 1. Assets 1 Increase or decrease ? Assets 2 Debited or Credited

Transaction Analysis Transaction 6 Prepaid Insurance $600 Cash $600

Transaction Analysis Transaction 7 March 9: Paid Tim Supply Co. $3,100 of the amount owed by check. ? Increase or decrease Assets Debited or Credited Liability

Transaction Analysis Transaction 7 Accounts Payable $3,100 Cash at Bank $3,100

Transaction Analysis Transaction 8 March 10: Performed a service by printing throwaways for a garment dealer and agreed to collect the fee at the beginning of the next month, $6,000. ? Increase or decrease Assets Owner’s equity Debited or Credited

Transaction Analysis Transaction 8 Accounts Receivable $6,000 Photocopy Fees Earned $6,000

Transaction Analysis Transaction 9 March 14: Accept $1,300 as an advance fee for copying works to be done for an advertising agency. Increase or decrease Assets ? Liability Debited or Credited

Transaction Analysis Transaction 9 Cash $1,300 Unearned Photocopy Fees $1,300

Transaction Analysis Transaction 10 March 19: Performed a service by printing price lists for Ward Fashion Company and collect a check of $3,400. Increase or decrease Assets ? Owner’s equity Debited or Credited

Transaction Analysis Transaction 10 Cash at Bank $3,400 Photocopy fees Earned $3,400

Transaction Analysis Transaction 11 March 24: George Ross withdrew $980 from the business for personal living expenses. George Ross, Withdrawals $980 Cash $980

Transaction Analysis Transaction 12 March 25: Paid the secretary salary, $1,100. Office Salary Expense $1,100 Cash $1,100

Transaction Analysis Transaction 13 March 29: Received and not paid the utility bill of $700. Utility Expense $230 Cash $230

Transaction Analysis Transaction 14 March 31: Received a telephone bill, $120. Telephone Expense $120 Accounts Payable $120

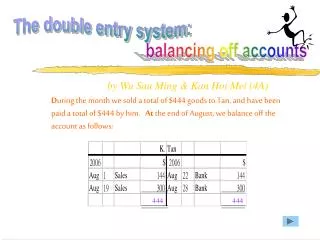

T account Cash(at Bank) 3. $10,000 14. 1,300 19. 3,400 • 6. $4,800 • 7. 2,000 • 2,300 • 600 • 3,100 • 24. 980 • 1,100 • 29. 230 Bal. $410

T account Accounts Receivable Office Supplies 8. $800 10. $6,000 Bal. $800 Bal. $6,000 Prepaid Insurance Photocopy Supplies 8. $2,300 8. $600 Bal. $2,300 Bal. $600

T account Prepaid Rent Office Equipment 7. $5,300 6. $4,800 Bal. $5,300 Bal. $4,800 Accounts Payable Photocopy Equipment 7. $2,000 9. $3,100 8. 3,100 7. $3,000 31. 120 Bal. $2,000 Bal. $600

T account Unearned Photocopy Fees George Ross, Withdrawal 24. $980 14. $1,300 Bal. $1,300 Bal. $980 George Ross, Capital Photocopy Fees Earned 3. $10,000 10. $6,000 19. 3,400 Bal. $10,000 Bal. $9,400

T account Office Salary Expense Telephone Expense 25. $1,100 31. $120 Bal. $120 Bal. $1,100 Utility Expense 29. $230 Bal. $230

T account On the basis of the T account calculation, we get the result as follows: Assets = Liabilities + Owner’s Equity $21,390 = $4420 + $16,970