Download

1 / 62

650 likes | 1.14k Views

Introduction to double entry system. 1.The need for book-keeping. 2. The accounting equation. 3. The double entry system for assets, liabilities and capital. 4. The asset of stock. 5. The double entry system for expenses and revenue. 6. Balancing off the accounts.

E N D

Introduction to double entry system 1.The need for book-keeping 2. The accounting equation 3. The double entry system for assets, liabilities and capital 4. The asset of stock 5. The double entry system for expenses and revenue 6. Balancing off the accounts

Introduction to double entry accounting 1.The need for book-keeping

What is accounting? Introduction to double entry accounting 1.Recording Accounting Data e.g. Peter… RECORDS Motor Van Buildings Computer

What is accounting? e.g. Chan’s family Introduction to double entry accounting 1.Recording Accounting Data RECORDS 2.Classifying and summarising data ? We should put them in a systematical way!

What is accounting? Introduction to double entry accounting 1.Recording Accounting Data RECORDS 3. Communicating Information 2.Classifying and summarising data ? I can tell you! Loss? 2.Classifying and summarising data We should put them in a systematical way! How can I know? Profit? Accountant

What is accounting? Introduction to double entry accounting RECORDS 1.Recording Accounting Data 2.Classifying and summarising data 3. Communicating Information

Accounting is the process of… What is book-keeping? Introduction to double entry accounting 1.Recording Accounting Data YES! Book keeping 2.Classifying and summarising data NO! NO! 3. Communicating Information

Introduction to double entry accounting 2. The Accounting Equation

Capital , Assets and Liabilities Introduction to double entry accounting e.g. S.Wong wants to open a fast food shop… What are they? $160 000 Desk and chair $500 000 $40 000 Computers $210 000 Goods $90 000 Cooker

Capital , Assets and Liabilities Introduction to double entry accounting Asset : The resources possessed by the firm Desk and chair Computers Goods Cooker

Capital , Assets and Liabilities Introduction to double entry accounting Capital : The resources supplied by the owner $500 000

Capital , Assets and Liabilities Introduction to double entry accounting Assets Capital $160000 Desk and chair + Computers $40000 $500 000 = + Goods $210000 + Cooker $90000

Capital , Assets and Liabilities Introduction to double entry accounting e.g.One year later,S.Wong wants to expand his business… e.g. S.Wong want to open a fast food shop… $160 000 Desks and chairs $500 000 $40 000 Computers $210 000 Extra goods Goods Extra Desks and chairs $90 000 Cooker Assets Capital =

Capital , Assets and Liabilities Introduction to double entry accounting e.g.One year later,S.Wong want to expand his business… But no money left… Borrow from bank! $500 000 $100 000 Desk and Chair Computer Extra goods Goods Extra Desks and chairs Cooker What can he do? Assets=Capital

Introduction to double entry accounting Capital , Assets and Liabilities Liabilities:The indebtedness of the firm for the resources $100 000 Assets: Extra goods Extra Desks and chairs

Introduction to double entry accounting Capital , Assets and Liabilities Capital Assets Liabilities + = Desk and Chair Computers Goods $500 000 $100 000 Cooker Extra Desks and chairs Extra goods

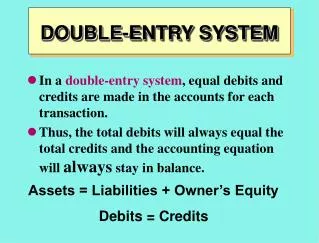

Introduction to double entry accounting Capital , Assets and Liabilities Accounting Equation: Assets = Capital + Liabilities

Introduction to double entry accounting 3.The double entry system: Assets,liabilities and capital

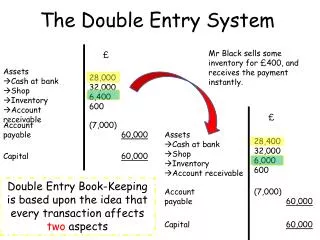

The Double Entry System Introduction to double entry accounting e.g. Tai Hung has a habit of recording the money he spent. When he buys a CD… We have to entertwice… Cash - CD + Double Entry System Each transaction affects 2 items…

Specify asset, capital or liability What is an account? Introduction to double entry accounting Account Name 2001 2001 $ $ Date Debit Credit

How to process the double entry system? 1.Double entry for ASSETS Introduction to double entry accounting Jan 4 Bought motor van paying by cash $160 000. Bought motor van paying by cash $160 000 Cash 2003 $ Jan 4 Motor Van 160 000 Motor Van $160 000 2003 $ Jan 4 Cash 160 000 Recall: $160 000 Assets = Capital + Liabilities

1.Double entry for ASSETS Introduction to double entry accounting Jan 6 Sold motor van by cash $90 000. $90 000 Cash 2003 $ Jan 6 Motor Van 90 000 Motor Van $90 000 2003 $ Jan 6 Cash 90 000 $90 000 Assets = Capital + Liabilities

1.Double entry for ASSETS Introduction to double entry accounting Conclusion: For ANY asset a/c - Decrease + Increase Assets = Capital + Liabilities

2.Double entry for Liabilities Introduction to double entry accounting Jan 10 Bought machinery from L.Lo Ltd. on credit $93 000. $93 000 Machinery 2003 $ Jan 10 L.Lo Ltd. 93 000 L.Lo Ltd. $93 000 2003 $ Jan 10 Machinery 93 000 $93 000 $93 000 Assets = Capital + Liabilities

2.Double entry for Liabilities Introduction to double entry accounting Feb 3 Paid L.Lo Ltd. $93 000 in cash. $93 000 Cash 2003 $ Feb 3 L.Lo Ltd. 93 000 L.Lo Ltd. $93 000 2003 $ Feb 3 Cash 93 000 $93 000 $93 000 Assets = Capital + Liabilities

2.Double entry for Liabilities Introduction to double entry accounting Conclusion: For ANY liability a/c + Increase - Decrease Assets = Capital + Liabilities

3.Double entry for Capital Introduction to double entry accounting Jan 1 The proprietor started business with $500 000 in cash. $500 000 Cash 2003 $ Jan 1 Capital 500 000 $500 000 Capital 2003 $ Jan 1 Cash 500 000 $500 000 $500 000 Assets = Capital + Liabilities

3.Double entry for Capital Introduction to double entry accounting Conclusion: Capital a/c + Increase - Decrease Assets = Capital + Liabilities

Conclusion for double entry system Introduction to double entry accounting Assets = Capital + Liabilities + Debit Credit Credit - Credit Debit Debit

The concept of Debtor and Creditor Introduction to double entry accounting Debtor Goods When he has not paid the business money, he is a debtor. Business Creditor Goods When the business has not paid him the money, he is a creditor. Business

Introduction to double entry accounting 4. The Asset of Stock

Accounts for each type of dealing in goods Introduction to double entry accounting Purchases Goods Supplier Sales Goods Business Customer In the business point of view…

Paid by cash or chequeimmediately Introduction to double entry accounting Purchases Paid for it later Cash Purchases Credit Purchases

1.Double entry of Purchases of stock for Cash Introduction to double entry accounting Aug 2 Goods costing $160 are bought by using cash. Purchases $160 2003 $ Aug 2 Cash 160 Cash $160 2003 $ Aug 2 Purchases 160 $160 Assets = Capital + Liabilities

2.Double entry of Purchases of stock on credit Introduction to double entry accounting Aug 4 Goods costing $160 are bought on credit from Wong. Purchases $160 2003 $ Aug 4 Wong 160 Wong $160 2003 $ Aug 4 Purchases 160 $160 $160 Assets = Capital + Liabilities

Receive cash or chequeimmediately Introduction to double entry accounting Sales Receive it later Cash Sales Credit Sales

1.Double entry of Sales of stock for Cash Introduction to double entry accounting Aug 6 Goods are sold for $55,cash being received. Cash $55 2003 $ Aug 6 Sales 55 Sales $55 2003 $ Aug 6 Cash 55 $55 Assets = Capital + Liabilities

2.Double entry of sales of stock on credit Introduction to double entry accounting Aug 8 Sold goods on credit for $250 to K.Lee. K.Lee $250 2003 $ Aug 8 Sales 250 Sales $250 2003 $ Aug 8 K.Lee 250 $250 Assets = Capital + Liabilities

Accounts for each type of dealing in goods Introduction to double entry accounting In the business point of view… Purchases Goods Sales Customer Supplier Goods Returns Outwards Business Damaged goods Damaged goods Returns Inwards

1.Double entry for Returns Inwards Introduction to double entry accounting Aug 5 Goods which had been previously sold to F.Lo for $29 are now returned by him. Returns Inwards $29 $ 2003 Aug 5 F.Lo 29 F.Lo $29 2003 $ Aug 5 Returns Inwards 29 $29 Assets = Capital + Liabilities

2.Double entry for Returns Outwards Introduction to double entry accounting Aug 6 Goods previously bought for $96 are returned by the firm to K.Lo. K.Lo $96 $ 2003 Aug 6 Returns Outwards 96 Returns Outwards $96 2003 $ Aug 6 K.Lo 96 $96 $96 Assets = Capital + Liabilities

Summary Cash Purchases – Dr. Purchases Cr. Cash Introduction to double entry accounting Credit Purchases – Dr. Purchases Cr. Supplier (Creditor) Cash Sales – Dr. Cash Cr. Sales Credit Sales – Dr. Customer (Debtor) Cr. Sales Returns Inwards – Dr. Returns Inwards Cr. Customer (Debtor) Returns Outwards – Dr. Supplier (Creditor) Cr. Returns Outwards

Introduction to double entry accounting 5. The double entry system for expenses and revenue

What is revenue? Introduction to double entry accounting Revenue is the sales value of goods and services that have been supplied to customers. e.g. Commission Received Rent Received

What is expense? Introduction to double entry accounting Expense is the value of all assets and costs that have been used to get those income. e.g. Motor Expenses Postage

Recall: Introduction to double entry accounting Capital a/c + Increase - Decrease Assets = Capital + Liabilities

What is the relationship between expenses and capital? Introduction to double entry accounting Expenses Profit Capital Capital a/c Any Expenses - + Debit

Examples on double entry Introduction to double entry accounting Aug 6 The rent of $300 is paid in cash. Rent $300 2003 $ Aug 6 Cash 300 Cash $300 $ 2003 Aug 6 Rent 300 $300 $300 Assets = Capital + Liabilities

Examples on double entry Introduction to double entry accounting Aug 8 Motor expenses are paid by cheque $200. Motor Expenses $200 2003 $ Aug 8 Bank 200 Bank $200 $ 2003 Aug 8 Motor Expenses 200 $200 $200 Assets = Capital + Liabilities

What is the relationship between revenue and capital? Introduction to double entry accounting Revenue Profit Capital Capital a/c Any Revenue - + Credit