Download

1 / 65

740 likes | 1.21k Views

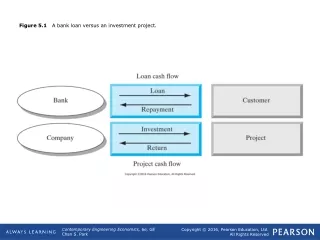

Bank Interest, Loan, and Investment Computation. Interest.

E N D

Interest • Interest – is a fee charged by a lender to a borrower for the use of borrowed money usually expressed as an annual percentage of the principal; the rate is dependent upon the time value of money, the credit risk of the borrower, and the inflation rate. Interest is also defined as the return earned on an investment.

Interest Rate • The Interest Rate – is the cost of borrowing money or the price paid for the rental funds; the ratio of interest to the amount lent. Interest rates have an impact on the overall health of the economy because they affect consumers willingness to spend, save, or make business investment decisions. Ex. Suppose that a $100 is lent and, at the end of the year, and $110 must be paid back. The interest paid is $10 and the interest rate is 10% (10÷100=0.10)

Bank Interest • Bank interest – is the amount of money that banks receive when they extend credit. Note: The rate of interest is the price of credit.

Bank Interest Rates • When banks quote an interest rate, they typically use a “benchmark”to calculate that interest rate. • Most of the time, that benchmark is theprime interest rate. The prime interest rate – is the interest rate a bank charges its most creditworthy customers. It is the base rate on corporate loans posted by majority of banks. • The prime interest rate is relevant to small businesses because bank's use it as the starting interest rate from which to calculate the interest rate on bank loans. • Another important interest rate is the Londan Interbank Offered Rate (LIBOR) for import/export business or another business with an international presence; LIBOR generally moves right along with the prime rate.

Calculating Interest Rate • Before making a decision to borrow money, the prospective borrower considers the rate of interest and should be convinced that it is not too harsh. • The lender on the other hand must be convinced that the reward for his sacrifice (postponing expenditure) is worth it. • Interest rates also serve as a basis for comparing the returns offered by various financial instruments.

The Simple Interest Rate Simple Interest – is a form of computing interest on an annual basis. Formula: Where: FA = Final amount (Total Amount Due) r = Rate of interest P = Principal t = Time i = Interest Ex. If Mr. X borrows $10,000 from Ms. Y at a simple interest of 10% per year, and is due for repayment in 3 years, how much does Mr. X owe Ms. Y on repayment date? Solving for Interest Solving for Total Amount Due

Loan Price • Loan Price (LP): • Corresponds to the total amount a borrower will pay for what he borrowed; the total amount due. Formula: LP = P+i Where: P = Principal i = interest

Calculation of the Loan Price (LP) and Simple Interest on Loans • Simple interest where time (t) is expressed in months: Ex.: Compute the simple interest of a 6-months P100,000 loan with 7%. Solution: i = Prt = 100,000 . 0.07 . 6/12 = P3,500 • Simple interest where time (t) is expressed in weeks: Ex.: Compute the simple interest and LP of a 6-months P100,000 loan with 1% per week. Solution: i = Prt = 100,000 . 0.01 . 26 = P26,000 Note: There are 52 weeks in 12 months

Calculation of the Loan Price (LP) and Simple Interest on Loans • Simple interest where time is expressed between two (2) dates: Ex.: Compute the simple interest of a P100,000 LOANat 7% granted from 10/15/09 until 1/20/10. MonthNo. of days Oct. (31days) 16 Nov. (30days) 30 Dec.(31days) 31 Jan. 20 Total 97 i = Prt =100,000 . 0.07 . 97/360 = P1,886.11 LP = P + i = 100,000+1,886.11 = 101,886.11 (31–15) Note: Banks use 360 days for loans

Calculation of the Final Amount and Simple Interest on Deposits • Simple interest where time is expressed between two (2) dates: Ex.: Compute the simple interest of a P100,000 DEPOSIT at 7% granted from 10/15/09 until 1/20/10. MonthNo. of days Oct.(31days) 16 Nov.(30days) 30 Dec.(31days) 31 Jan. 20 Total 97 i = Prt =100,000 . 0.07 . 97/365 = P1,860.27 F = P+i = 100,000+1,886.11 = 101,860.27 (31–15) Note: Banks use 365 days for deposits

Different Time Factors • Different time factors: • Exact time ÷ 360 • Ordinary time ÷ 360 • Exact time ÷ 365 • Ordinary time ÷ 365 Note: No. of days in a year used by banks: • For loans = 360 days in 1 year (as much as possible exact time) • For deposits = 365 days in 1 year (as much as possible ordinary time)

Calculation of the Loan Price (LP) and Simple Interest on Loans • Different time factors: Ex. July 5, 2009 – Sep. 17, 2009 1. Exact time ÷ 360 July(31days)26 (31-5) Aug(31days) 31 Sep 17 74 2. Ordinary time ÷ 360 July(30days) 25 (30-5) Aug(30days) 30 Sep 17 72 ET÷360: 74 ÷ 360 = 0.2056 Only 30 days every month OT÷360: 72 ÷ 360 = 0.2000

Calculation of the Loan Price (LP) and Simple Interest on Loans • Different time factors: Ex. July 5, 2009 – Sep. 17, 2009 Cont’d… 3. Exact time ÷ 365 July(31days) 26 (31-5) Aug(31days) 31 Sep 17 74 4. Ordinary time ÷ 365 July(30days) 25 (30-5) Aug(30days) 30 Sep 17 72 ET÷365: 74 ÷ 365 = 0.2027 Only 30 days every month OT÷365: 72 ÷ 365 = 0.1973

Summary • No. of days in a year used in loans and deposits: • For loans: ET÷360 – this will give them the greatestinterest income • For deposits: OT÷365 – this will give them the least interest expense

Derivation of rate (r), time (t), and principal (P) • Simple interest formula: i = Prt • Based on the above formula, the following can be derived: • To find rate r r = i/ Pt • To find time t t = i/ Pr • To find Principal P P = i/ r t

To find time (t) • Time (t): Ex. Ben opened a time deposit in a bank amounting to P100,000 with a 4% simple interest rate. If he received P8,000 at the maturity date, how many years had his money been deposited in the bank? Solution: Consider i = P8,000 t = i/ Pr = 8,000 ÷(100,000 . 0.04 ) = 2 years

To find rate (r) and principal (P) • Rate (r): Ex. Flor invested P70,000 in a cooperative bank where the interest was P14,000 after two and a half years. What is the rate of her investment? Solution: r = i/ Pt = 14,000 ÷(70,000 . 2.5 ) = 8% • Principal (P): Ex. Lito received an interest of P12,500 in his savings account for 1 year at 5%. What was the original deposit? Solution: P = i/ r t = 12,500 ÷(0.05 . 1 ) = P250,000

Derivation of F and P The two (2) formulas we have to review are i=Prt and F=P+i • Derivation of final amount (F): F = P + i = P + Prt since i=Prt F =P . (1+rt) • Derivation of principal (P): P= F/(1+rt)

Derivation of F and P, Examples • Final amount (F): Ex. Luis deposited P200,000 to a bank which gives 5% simple interest. How much would he received at the end of 48 months? Solution: Consider t = 4 (48 ÷12) F = P . (1+rt) = 200,000 .(1+0.05 . 4 ) = P240,000 • Principal (P): Ex. How much must be invested in order to have P240,000 at the end of 4 years if money’s worth is 5% simple interest? Solution: P = F/(1+r t) = 240,000 ÷(1+0.05 . 4 ) = P200,000

Calculation of Basic Elements of Loan Pricing • 2 Types of interest computation: 1. Ordinary interest – interest is paid at maturity date. 2. Discounted interest – interest is paid in advance. Note: In both instances, one may use the simple interest rate formula.

Simple Discount • Interest discount (i): Formula: i = Fdt Where: F = Final amount d = discount rate t = time • Proceeds (Pr): Formula: Pr = F–i Where: Pr = Proceeds F = Final amount i = Interest

i and Pr, Examples • Interest discount (i) : Formula: i = Fdt Ex: How much interest will be collected in advance of a P114,000 loan for a term of 5 years if the discount rate is 12%. Sol. : i = 114,000 . 0.12 . 5 = P68,400 • Proceeds (Pr): Formula: Pr = F–i Ex: Compute the proceeds of a 1-year discounted loan amounting to P100,000 loan with 7%. Sol. : Consider i = Prt = 100,000.0.07.1= 7,000 Proceeds = 100,000 – 7,000 = P93,000

Simple Discount • Interest discount (i): Formula: i = Fdt • Based on above formula, we can derive the following formulas: • To find maturity value (F) F = i/ dt or F=P-i • To find time (t) t = i/ Fd • To find rate (r) d = i/ Ft

Derivation of Pr and F The two (2) formulas we have to review are i=Fdt and Pr=F– i • Derivation of proceeds (Pr): Pr = F – i = F – Fdt since i=Fdt Pr = F . (1– dt) • Derivation of the Final amount (F): F= P/(1–dt)

Derivation of Pr, Example • Proceeds (Pr): Formula: Pr= F. (1– dt) Ex: What are the proceeds and the discount on P400,000 for 2 years at 10% simple discount. Sol. : Pr = F. (1– dt) = 400,000 (1– 0.10 . 2) = P320,000 i=F–Pr or i=Fdt = 400,000–320,000 = 400,000 . 0.10 . 2 = P80,000 = P80,000

The Compound Interest Rate The Final Amount (FA or simply F) in a compound interest is said to be the loan price (in a loan transaction) or future value (in an investment). Formula: FA = P (1 + r)n Ex. In a $10,000 loan, if the 10% is compounded annually for 3 years, what is the total amount due on maturity date? FA = 10,000 (1 + 0.10)3 = $13,310 Where: P = Principal r = Rate of interest n = Compounding period

Compound Interest – Computing for r and n • Computing for r and n Formula: r = j/m Where j = nominal rate m = frequency of conversion n = tm Where t = time m = no. of times compounded • Ex.: Compute the compounded amount of a 2-year loan amounting to P100,000 with 7% interest rate compounded quarterly. Sol. F = P . (1+j/m) t.m = 100,000 . (1+0.07/4) 2.4 = 100,000 . (1.0175)8 = P114,888.18

Compound Interest • Compound Interest – is the method of calculating interest on the original capital invested on interest earned on previous periods. Formula: Compounded once a year i = P. [(1+r) n– 1] Where: i = Compound interest P = Principal r = rate t = No. of years Compounded n times a year i = P. [(1+ j/m) tm – 1] Where: A =Amount P = Principal j = nominal rate m = Frequency of conversion t = No. of years

Compound Interest • Compound interest Ex.: Compute the compounded interest of a 2-year loan amounting to P100,000 with 7% interest rate. Sol. i = P . [(1+ r) n– 1] = 100,000 . [(1.07)2– 1] = P14,490 • Compound interest (w/ no. of times compounded) Ex.: Compute the compounded interest of a 2-year loan amounting to P100,000 with 7% interest rate compounded quarterly. Sol. i = P . [(1+ j/m) tm – 1] = 100,000 . [(1+0.07/4)2 . 4– 1] = P14,888

Compound Interest • Total deposits after n payments have been made: Formula: Bn = A (1+i)n + {P÷i . [(1+i)n – 1]} Ex. At the end of every month, you put P10,000 into a mutual fund that pays 6%, compounded monthly. How much will you have at the end of five years? Solution: Consider P = 10,000, i = 6%/12 = .005, A = 0 (because you start with nothing in the account), n = 60 (5x12) B60 = 0 + {10,000÷0.005 . [(1+0.005)60 – 1]} = P697,700 Where: B = Balance P = Principal A = Amount n = No. of months i = interest rate/month

Compound Interest • Loan balance after n payments have been made: Formula: Bn = A (1+i)n – {P÷i . [(1+i)n – 1]} Ex. You have a $18,000 car loan at 14.25% for 36 months. You have just made your 24th payment of $617.39 and would like to know the payoff amount Solution: Consider P = 18,000, i = 14.25%/12 = .011875, n = 24 B24 = 18,000 . 1.01187524 – {617.39÷0.011875 . (1.01187524 – 1)} = $6,866.97

Compound Interest • Computing monthly payment on a loan: Formula: P = iA 1-(1+i)-n Ex. What is the monthly payment if you bough a P2.5M house, with 10% down, on a 30-year mortgage at a fixed rate of 7.8%? Sol. n = 360 (30x12); i = 0.0065 (0.078/12); A = 2.25M (2.5M x 0.90) P = 0.0065 x 2,250,000 1-(1+0.0065)-360 = P16,197.09

Compound Interest • Original loan amount: Formula: A = P÷i . [1 – (1+i)–n] Ex1. You want to purchase a 20-year annuity that will pay $500 a month. If the guaranteed interest rate is 4%, how much will the annuity cost? Solution: Consider P = 500, i = 4%/12 = .0033, n = 240 (20x12) A = 500÷0.0033 . [1 – (1.0033)–240] = $82,798.67

Compound Interest Ex2. You’re looking to buy furniture for your living room. You can afford to pay about $60 a month over the next three years, and your credit card charges 4% interest. How much furniture can you buy? Solution: Consider P = 60, i = 4%/12 = .0033, n = 36 (3x12) A = P ÷i . [1 – (1+i)–n] = 60/0.0033 . [1 – (1.0033)–36] = $2,033

Compound Interest Ex3. (Continued from Ex2). But you have your eye on a set that’s on sale for $1850. The saleswoman offers you a store credit card with a special promotional rate of 12% for three years. Now can you afford the furniture? Solution: Consider P = 60, i = 12%/12 = .01, n = 36 (3x12) A = P ÷ i . [1 – (1+i)–n] = 60/0.01 . [1 – (1.01)–36] = $1,806.45 You cannot afford the furniture. Either you raise your monthly payment or lower the interest rate.

Compound Interest • Number of payments on a loan: Formula: N = -log(1-iA÷P) log (1+i) Ex1. Sally offers to lend you P35,000 at 6% for that new home theater system you want. If you pay her back P1,000 a month, how long will it take? Sol. Consider i = 0.005 (0.06/12) N = -log(1-0.005 . 35,000÷1,000) log (1.005) = 38.57 months

Compound Interest Ex2. (Continued from Ex1). How much is the final balance you owe Sally? Formula: Bn = A (1+i)n – {P÷i . [(1+i)n – 1]} B38 = 35,000 . 1.00538 – {1,000÷0.005 . (1.00538 – 1]} = P568.25 Interpretation: You will pay Sally P1,000/month for 38 months and finish-off the loan on the 39th month paying P568.25.

Compound Interest • Number of payments on a loan: Formula: N = -log(1-iA÷P) log (1+i) Ex. You have $15,000 in a 5% savings account, which is compounded monthly. How long will it take to run down the account if you withdraw $100 a month? Sol. Consider i = 0.004167 (0.05/12) N = -log(1-0.004167 . 15,000÷100) log (1.004167) = 235.89 months

Nominal Versus Real Interest Rate • Nominal Interest Rate – refers to the interest rate that takes inflation into account. Ex. If the market, or nominal, rate of interest is 10% per annum, then a dollar today can be exchanged for $1.10 a year from now. Formula: Where: RIR =Real int. rate NIR = Nominal int. rate EIR = Expected inflation rate

Nominal Versus Real Interest Rate • Real Interest Rate – is the rate adjusted for expected changes in the price level (inflation) so that it more accurately reflect the true cost of borrowing. The real rate of interest is adjusted for expected future price-level changes; it is the rate of exchange between goods and services today, and goods and services in the future. Formula: Note: An inflation rate of 10% will off-set the 10% nominal interest rate or a real interest rate of zero. Where: RIR =Real int. rate NIR = Nominal int. rate EIR = Expected inflation rate

Nominal Versus Real Interest Rate Cont’d. Ex.1: Mr. X is considering lending his $100,000 for 1 year to Ms. Y with a promised interest payment of $8,000. As the inflation rate for next 12 months is forecasted at 10%, will it be wise for Mr. X to lend his money to Ms. Y? Answer: The intended loan is not a good proposition because he will stand to lose 2% of the purchasing power of his money instead of adding 8% to it.

Nominal Versus Real Interest Rate Cont’d. Ex.2: If the nominal interest rate on a bond is 4.50%, and a reliable estimate suggests that inflation over the term will average 2.75%, the real interest rate could be estimated as follows: Thus, the real rate of return in this case is just 1.75%.

Nominal Versus Real Interest Rate The Equation This equation can be arranged to show that:

Effective Interest Rate (EIR) on an Ordinary Interest • Effective interest rate on an ORDINARY INTEREST loan: Formula: EIR = i/ P Where: eir = Effective int. rate i = Interest P = Principal Ex. Compute for the effective interest rate of a P100,000 1-year with a P7,000 interest. Sol. EIR = i/ P = 7,000 ÷ 100,000 = 7%

EIR on a Discounted Interest • Effective interest rate on a DISCOUNTED INTEREST loan: Formula: EIR = i/ Pr Where: EIR = Effective int. rate i = Interest Ex. Compute for the effective interest rate of a 1-year discounted loan amounting to P100,000 at 7%. Sol. Consider i = 7,000, Proceeds = 93,000 (100,000 –7,000) EIR = i/ Pr = 7,000 ÷ 93,000 = 7.53%

EIR on a Discounted Interest (Less than 1 yr) • Computing the effective interest rate on a loan with a term of less than 1 year. Formula: EIR = (i/ P) . 360/days loan outstanding Where: EIR = Effective int. rate i = Simple interest rate P = Principal Ex. Compute for the effective interest of a P100,000 120- days at 7% loan with a P7,000 interest. Sol. Consider i = 7,000 EIR = (i/P) . 360/days loan outstanding = (7,000 ÷ 100,000) . 360/120 = 21%

Comparative Analysis • Which has the lower effective interest rate between an ORDINARY and DISCOUNTED INTERES RATE? Ex. Bank A (Ordinary) 20% 1 year Bank B (Discounted) 19% 1 year Sol. Bank A = 20% Bank B 0.19 = 24% 0.81 Bank A has the lower interest rate.

Compensating Balance • Banks, under a line of credit arrangement, may require borrowers to deposit money that will not earn interest known as the compensating balance. • Compensating balance (C/B): Formula: C/B = P . r Where r = rate Ex. A company borrows P200,000 and is required to keep a 12% compensating balance. It also has an unused line of credit in the amount of P100,000 for which a 10% compensating balance is required. Compute the minimum balance the company must maintain. Sol. Consider C/B1 = 24,000 (200,000 x 0.12), C/B2 = 10,000 (100,000 X 0.10) C/Btotal = 24,000 + 10,000 = P34,000