Download

1 / 29

290 likes | 314 Views

This article discusses the Forward LIBOR Model and its application in valuating knockout cap securities. It covers topics such as lattice calculation, transitional probability, martingale measures, and valuation techniques. The impact of different measures and lattice generation methods on the pricing accuracy is examined. The article concludes with a discussion on the future research directions in incorporating transitional probabilities of other periods for valuing various derivatives.

E N D

Lattice Calculation for Forward LIBOR Model Tadashi Uratani Hosei University uratani@k.hosei.ac.jp and Makoto Utsunomiya Bank of Tokyo-Mitsubishi Jafee 99

Outline • Interest rate sensitive security (e.g. Cap) • Definitions: Bond Price, LIBOR • Forward LIBOR Model • Martingale, No Arbitrage, and • Backward, Forward Induction Method • Lattice Calculation • Transitional Probability among Measures • Valuation of Knockout Cap Jafee 99

Short term interest(LIBOR) difference Interest rate derivatives E.g. Cap rate Company premium difference Exercise rate Bank date Jafee 99

3 month Returning date Borrowing date LIBORLondon Interbank Offer Rate Typical short-term interest rate in international capital market 3 month LIBOR 6 month LIBOR Jafee 99

Forward LIBORand Discount Bond Price Forward LIBOR Jafee 99

Forward LIBOR and Bond Price Jafee 99

Bond process Forward LIBOR Model Ito’s Lemma Valuation of derivatives by Forward LIBOR Jafee 99

Change of Probability Measure Girsanov Theorem Jafee 99

Market value of risk Martingale No Arbitrage Condition Jafee 99

Pricing by Martingale Martingale under Jafee 99

Risk Neutral Measure Jafee 99

Risk Adjusted Measure Jafee 99

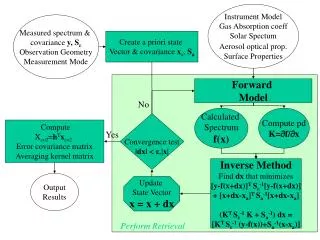

Valuation of cap Generation :F. LIBOR Choice :Meas. Forward Backward Lattice martingale Jafee 99

Lattice Calculation Martingale Measures Jafee 99

Transition Probability Jafee 99

Relation of Transition Probabilities Jafee 99

One measure Jafee 99

Cap contract is knockout Knockout Cap rate LIBOR Year Jafee 99

Binominal tree under each measure Calculate the knocknout Unify one measure Valuation of derivative Jafee 99

Knockout Cap Underlying security:3 month LIBOR maturity 3 years knockout cap Jafee 99

fd La fd La fd La fd La Error Knockout rate Jafee 99

Why lambda affect? Large λ Lattice generation Jafee 99

End Jafee 99

単純モンテカルロ法 試行回数10000回 時点分割10 時点分割10 Knockout Cap 前進法、後退法 多重格子法 3ヶ月LIBORを対象とした3年満期の0時点における価格 Jafee 99

Conclusion • 異なった測度による推移確率関数を関係付けることによりいくつかの金利派生証券を評価 • 推移確率関数を格子法に利用 • Knockout Capletにおいてλが大きいとき他の方法に比べ誤差が大きい • 各格子の作成方法を検討 • 推移確率関数の検討 • 他の期間同士のForward LIBORの推移確率の導入し、他の派生証券を評価 Jafee 99