Common Probability distributions

Common Probability distributions. Probability distribution. The set of probabilities for the possible outcomes of a random variable is called a “probability distribution.”. The underlying foundation of most inferential statistical analysis is the concept of a probability distribution.

Common Probability distributions

E N D

Presentation Transcript

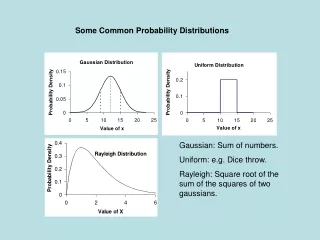

Probability distribution The set of probabilities for the possible outcomes of a random variable is called a “probability distribution.” The underlying foundation of most inferential statistical analysis is the concept of a probability distribution. The focus in the investments arena is on four probability distributions. Uniform Binomial Normal Lognormal An understanding of probability distributions is critical to using such quantitative methods as hypothesis testing, regression, and time-series analysis.

Discrete and continuous random variables A random variable is a variable whose future values are uncertain. Discrete random variables have a theoretically countable number of outcomes. There may be an infinite number of them, but they are countable. Price is a discrete random variable. Continuous random variables have a theoretically uncountable number of outcomes. Rate of return is a continuous random variable. Temperature is a continuous random variable.

Random Variables and outcomes Focus on: Example of a Random Variable and Its Outcomes Consider a special dividend with five possible year-end values: $1, $5, $7, $10 and $11. Each of these values is known as an outcome. The random variable is described by its set of possible outcomes as Div {$1, $5, $7, $10, $11}

Probability functions The possible outcomes of a random variable and their associated probabilities are collectively known as a probability function. By convention, discrete random variable probability functions are denoted as p(x) and known as probability mass functions (pmf). Continuous random variable probability functions are denoted as f(x) and are known as probability density functions (pdf). Probability functions have two very important properties: Any and all individual probabilities described by the probability function take on a value between 0 and 1 (including 0 and 1). The sum of all probabilities described by the probability function is equal to 1.

Verifying a probability function Focus on: Calculations Consider a special dividend with five possible year-end outcomes of $1, $5, $7, $10, and $11. The probability of each outcome is 0.05, 0.3, 0.5, 0.1, and 0.05, respectively. Is this a valid probability function? If so, of what type (discrete or continuous)?

Verifying a probability function Focus on: Calculations Consider a special dividend with five possible year-end outcomes of $1, $5, $7, $10, and $11. The probability of each outcome is 0.05, 0.3, 0.5, 0.1, and 0.05, respectively. Is this a valid probability function? It satisfies our two properties. This is a discrete random probability function. The outcomes are countable, and it is a valid probability function.

The probability density function (pdf) The mathematical expression that describes the individual probabilities that a random variable will take on each of a set of specified values is known as its probability density function. For a discrete distribution, the pdf has discrete, countable, nonzero probabilities for every possible outcome. For a continuous distribution, the pdf has continuous, uncountable probabilities for each possible specified outcome in the set of infinite, uncountable outcomes. Hence, the probability of any specific outcome is zero. For continuous distributions, this result means that the cumulative distribution function will be more useful and, to some extent, more meaningful.

The cumulative distribution function (cdf) The mathematical expression that describes the probability that a random variable will be less than or equal to a specific value for all possible values of that variable is known as its cumulative distribution function. The cumulative distribution function, denoted F(x), is represented as the sum of the probabilities of the specified outcome and all prior outcomes in the distribution for each and every possible outcome. By analogy, this is very similar to the concept of cumulative relative frequency from Chapter 3 on Statistical Concepts and Market Returns. The cdf has the same properties as the pdf, in addition to All values of thecdfare between 0 and 1; As we increase the value of the specified outcome, the cdf must increase or remain constant.

The cdf in action Focus on: Calculations Returning to the special dividend example, the cdf can be written and depicted as: What is the probability of receiving at least a $10 dividend? What is the probability of receiving more than a $7 dividend?

The cdf in action Returning to the special dividend example, the cdf can be written and depicted as: What is the probability of receiving at least a $10 dividend? From the cdf function, it is 0.95. What is the probability of receiving more than a $7 dividend? It will be 1 minus the probability of receiving $7 or less, which is 0.85. The answer is 0.15. Focus on: Calculations

The discrete uniform distribution A basic distribution wherein the probably of every possible countable outcome is equally likely. Consider again our special dividend with five possible year-end outcomes of $1, $5, $7, $10, and $11, except that now the probability of each outcome is 0.2, so this is a discrete uniform random variable. The outcomes are countable. Each possible outcome has a probability between 0 and 1. The sum of the probabilities of the outcomes is 1.0 = 0.2 + 0.2 + 0.2 + 0.2 + 0.2. AND, the probability of each outcome is 1/n = 0.2. Our new special dividend is a discrete uniformly distributed random variable. Any of the distributions we study in this book can be replicated using the uniform random distribution to generate random numbers with specific patterns.

The discrete uniform distribution Focus On: Calculations What is the probability we will receive a $5 dividend? A dividend of at least $5? A dividend that is greater than $9?

The discrete uniform distribution Focus On: Calculations What is the probability we will receive a $5 dividend? A dividend of at least $5? From the pdf, P(Div = $5) = 0.2. From the cdf, P(Div < $5 or = $5) = 0.4. A dividend that is greater than $9? From the pdf, P(Div = $10) + P(Div = $11) = 0.2 + 0.2 = 0.4 or From the cdf, 1 – P(Div < $9) = 1 – 0.6 = 0.4.

Binomial random variables A binomial random variable has only two possible outcomes, termed “success” and “failure” by convention. The basic building block of the binomial distribution is a Bernoulli random variable. A Bernoulli random variable is one for which there are only two possible outcomes, and the probability of these outcomes satisfies the conditions for a valid pdf. That is, each probability is between 0 and 1 and they sum to 1. A single observation of the outcome of a Bernoulli random variable is called a “trial” when the random variable can repeat. The sum of a series of Bernoulli trials is distributed as a binomial random variable. In order to use the binomial distribution, we must satisfy two conditions: The probability of each outcome must be constant for all trials; and The trials must be independent.

Binomial random variables Focus On: Characterizingthe Distribution The pdf for a discrete binomial distribution is written as: We indicate that a random variable is binomially distributed as: The mean and variance of a binomially distributed variable X ∼ B(n, p)

Binomial random variables Focus On: A Critical Example The binomial option pricing model developed by Cox, Ross, and Rubeinstein (1979) is one of the most important and famous uses of the binomial distribution. It is widely used to price options. Stock price today is denoted S. If u(d) is 1 plus the rate of return when the stock price moves up (down), then uS (dS) is the end of period price for the stock and the diagram depicts a single Bernoulli trial. Stock price moves up Stockprice equals uS Probability= p Stock price today, S Stock price moves down Stock price equals dS • Probability = 1 –p

Binomial Random Variables Focus On: Calculations You decide to assess an analyst’s ability to forecast the sufficiency of earnings over a 20-quarter period. Over that time, the analyst correctly predicted earnings 13 times and incorrectly predicted earnings 7 times. You decide to model the “correctness” of his predictions using the binomial distribution. What is your estimate of the probability of a successful prediction by this analyst? Assuming the estimated probability is the actual probability, answer the following questions: What is the probability that the analyst will be correct for the next four quarters? What is the expected number of quarters the analyst will be correct over the next three years? What is the standard deviation of “correctness” for that period?

Binomial Random Variables Focus On: Calculations You decide to assess an analyst’s ability to forecast the sufficiency of earnings over a 20-quarter period. Over that time, the analyst correctly predicted earnings 13 times and incorrectly predicted earnings 7 times. You decide to model the “correctness” of his predictions using the binomial distribution. What is your estimate of the probability of a successful prediction by this analyst? 13/20 = 0.65 What is the probability that the analyst will be correct for the next four quarters? (0.65) (0.65)(0.65)(0.65) = 0.1785 What is the expected number of quarters the analyst will be correct over the next three years? 12(0.65) = 7.8 What is the standard deviation of “correctness” for that period? [12(0.65)(0.35)]0.5 = 1.6522

Binomial stock price tree Stock price today is denoted S. If u(d) is 1 plus the rate of return when the stock price moves up (down), then uS (dS) is the end of period price for the stock, and the diagram above depicts a series of Bernoulli trials that represents the movement in stock price as a binomial random variable. The probability of an “up” move is known as the up transition probability, and that of a “down” move is known as the down transition probability. Note that this tree recombines. In other words, udS = duS, etc. uuuS uuS uS uudS S udS dS uddS ddS dddS

The continuous uniform distribution Recall that continuous variables are those whose possible outcomes cannot be counted. By analogy, the continuous uniform distribution is the continuous counterpart to the discrete uniform distribution. This distribution is almost always the basis for generating random numbers in simulations; hence, it is a very important distribution. We generally use this distribution when we have no prior beliefs about the distribution of probabilities over outcomes (uncertainty in our beliefs) or when we believe probability is equally spread over the possible outcomes.

The continuous uniform distribution Focus On: Characterizing the Distribution The pdf and cdffor a continuous uniform distribution are written as Probabilities are calculated from The mean and variance of a continuous uniformly distributed variable are

The continuous uniform distribution Focus On: Calculations You are examining the forecasts of a buy-side analyst for the free cash flow (FCF) available to shareholders at a subject company. She estimates that the FCF will fall within –25m to 275m. You have decided to treat this as a continuous uniform variable. What is the expected value of FCF? (–25 + 275)/2 = 125 What is the probability that FCF is negative? [0 – (–25)]/[275 – (–25)] = 0.083333

The Normal distribution A continuous, symmetrical distribution that is completely described by its mean and variance. Arguably, it is the single most important distribution in statistics. It plays a key role in modern portfolio theory and risk management. The central limit theorem demonstrates that the sum and mean of a large number of independent random variables will be normally distributed even when the variables are not themselves normally distributed. The normal distribution ranges from infinitely negative to infinitely positive. It is often used as a model for approximate returns. Linear combinations of normally distributed variables are also normally distributed.

The Normal distribution A continuous, symmetrical distribution that is completely described by its mean and variance. Mean, median, and mode are equal. The normal distribution has skewness of zero. Option returns are skewed; hence, they are not normally distributed. Kurtosis of 3 or excess kurtosis of 0 (3 – 3 = 0). k > 3 fat tails underestimated probability of extreme values (the blue distribution has excess kurtosis). This area is one for which the normal distribution is a poor approximation for stock returns, which have “fat tails.”

The Normal distribution Focus On: Characterizing the Normal Distribution The pdf for a normal distribution is written as We indicate that a random variable is normally distributed as The mean and variance of a normally distributed variable are

Univariate vs. multivariate A single random variable is said to be univariately distributed. A group of related random variables is said to be multivariately distributed. A group of two random variables would have a bivariate distribution. The multivariate normal distribution is common in portfolio applications.

Correlation and the multivariate normal distribution To characterize a multivariate normal distribution, we need: The list of mean returns for each security; The list of variances in those returns for each security; The list of all possible pairwise return correlations. If individual security returns are jointly, normally distributed, then the returns of a portfolio of these securities will also be normally distributed and we can describe the probability behavior of that portfolio with the information in the list.

The normal distribution Focus On: Confidence Intervals Approximately 50% of all observations fall in the interval µ ± (2/3)σ. Approximately 68% of all observations fall in the interval µ ± σ. Approximately 95% of all observations fall in the interval µ ± 2σ. Approximately 99% of all observations fall in the interval µ ± 3σ. We generally don’t observe population mean and variance (µ and σ), but we can estimate them with sample mean and variance. When we do, the same intervals apply, with the sample mean and variance used in place of their population analogs.

The normal distribution Focus On: Confidence Interval Calculations Your client’s portfolio has a mean monthly return of 1.2% with a standard deviation of 3.7%. You assume for now that returns are normally distributed. Your client’s return can be expected to fall in what range 50% of the time? [0.12 – 2/3*0.037, 0.12 + 2/3*0.0377] [–0.01267, 0.036667] 68% of the time? [0.12 – 0.037, 0.12 + 0.0377] [–0.025, 0.049] 95% of the time? [0.12 – 2*0.037, 0.12 + 2*0.0377] [–0.062, 0.086]

Standard Normal A normal distribution with a mean of 0 and standard deviation of 1 is called “standard normal.” The prevalence of the normal distribution has led to a process whereby probability tables that have been calculated for a standard normal distribution can be used to make probability statements for any normally distributed variable. This process is known as “standardizing” and is accomplished by: Taking the observation(s) of interest and subtracting the mean of that observation’s observed distribution; Dividing the result by the observed distribution’s standard deviation.

The Standard normal distribution Focus On: Calculations Your client’s portfolio has a mean monthly return of 1.2% with a standard deviation of 3.7%. You assume for now that returns are normally distributed. What is the chance that returns will be between –2.5% and 4.9%? P(r < 4.9) – P(r< –2.5) = P(z < 1) – P(z< –1) = 0.682689 What is the chance that returns will be negative? P(r < 0) = P(z < –0.0324) = N(–0.0324) = 0.372846 A stop-loss order automatically sells the stock if the price is below a set amount. You can set a stop-loss so that the portfolio is liquidated when it is triggered. How often will such a stop-loss be triggered if you set it so that it triggers when losses are below 1%? P(r< –1.0) = N(–0.595) = 0.276057, or 27.61% of the time

Shortfall risk The risk that portfolio value will fall below a minimum acceptable level across a specified time horizon. We can define a threshold below an acceptable minimum threshold level, RL. Roy’s safety-first criterion states that the optimal portfolio is one that minimizes the probability of a return below RL. If returns are normally distributed, then we can calculate Roy’s safety-first ratio as The optimal portfolio will be the one with the highest SFRatio because that portfolio minimizes the probability of a shortfall.

The safety-first criterion Focus On: Implementing Shortfall Risk Calculations You are researching asset allocations for a client with an $800,000 portfolio. Although her investment objective is long-term growth, at the end of a year she may want to liquidate $30,000 of the portfolio to fund educational expenses. If that need arises, she would like to be able to take out the $30,000 without invading the initial capital of $800,000.

The safety-first criterion Focus On: Implementing Shortfall Risk Calculations Given the client’s desire not to invade the $800,000 principal, what is the shortfall level, RL? Use this shortfall level to answer the next questions. 0.0375 from 30k/80k According to the safety-first criterion, which of the three allocations is the best? Calculate SFRatio score B What is the probability that the return on the safety-first optimal portfolio will be less than the shortfall level? Use standard normal tables to evaluate SFRatio for B 0.182

The Lognormal distribution The normal distribution is unsuited for modeling prices because it has an infinitely negative lower bound, so we use the lognormal instead. Y follows a lognormal distribution if Y = ln(Y) is normally distributed or if ln(Y)=Y is normally distributed. Characterized by four parameters: (1) mean and (2) standard deviation of the underlying normal variable; (3) mean and (4) standard deviation of the lognormal variable itself, which are functions of (1) and (2).

Asset prices and the lognormal distribution Focus On: Characterizing the Distribution The lognormal distribution is bounded below by zero and positively skewed. The lognormal distribution underlies the Black–Scholes option pricing model. Empirically, it has been found to be a useful description of asset prices. The mean and standard deviation of a specific lognormal distribution are: where µ and σ are the parameters for the normal distribution underlying it. Key result: If a stock’s continuously compounded return is approximately normally distributed, then its future stock prices are lognormally distributed.

Continuous compounding If the frequency with which we calculate interest is infinitely large or the time interval infinitely small, we are using continuous time compounding. A continuously compounded return is one in which time is viewed as continuous; with discrete compounding, time advances in finite intervals. A continuously compounded return is calculated as If the holding period return from time = 0 to time = T is 0.056, then the continuously compounded return for time (0,T) can be determined. If the holding period return is 0.056, then a stock that begins with a price of $1 ends the period with a price of $1.056. or or

Monte Carlo simulation Monte Carlo simulation is one method for representing a complex financial system in which a number of random variables interact. Monte Carlo simulation relies on the generation of a large number of random samples in which the randomly generated variables interact with the structure of the simulation to provide a probability distribution of possible outcomes. The generation of the random values provides the mechanism for the operation of risk within the system. One drawback of Monte Carlo analysis is that it provides only statistical estimates and not exact results, so it is only as good as the model of the data and their interactions. Historical simulation, in contrast, draws repeated samples from historical data rather than specified probability distributions. It can only reflect risks present in the historical data and, therefore, does not lend itself to “what if” analysis.

summary Four probability distributions are commonly used in investments applications: the uniform, the binomial, the normal, and the lognormal distributions. The uniform distribution is generally used in simulation applications, including Monte Carlo analysis. The binomial forms the basis for many option pricing applications. The normal distribution, with its attractive statistical properties, is prevalent throughout investments and is used as a central distribution for modeling returns. The lognormal distribution is generally used to model asset prices for which the normal, with its theoretical infinitely negative lower bound, is unsuited. If returns are normally distributed and continuously compounded, then asset prices can be shown to be lognormally distributed.

Bernoulli Example • Evaluating Block Brokers • View each trade as a Bernoulli trial. • What are probabilities of a successful trade with each broker? • Binomial assumes • Probability is constant for all trials. • Trials are independent. • Probabilities are based on the counting from the prior chapter.

Bernoulli Example • If you are paying a fair price on average in your trades with a broker, what should be the probability of a profitable trade? • Did each broker meet or miss that probability expectation? • Under the assumption that the prices of trades were fair: • Calculate the probability of three or fewer profitable trades with Broker BB001. • Calculate the probability of five or more profitable trades with Broker BB002.

Bernoulli Example • Probability is 50/50 if the trades are fair. • BB001 misses at 0.25; BB002 exceeds expectations at 0.625. • You need the cdf for three or fewer for BB001, and five or greater for BB002. • For BB001, this probability is 0.0730. • For BB002, this probability is 0.3633. Note: The magnitude of trade losses/gains may also be important, and that is masked by the classification as profitable or not.

Tracking Error Example • Suppose you are evaluating a manager on the level of tracking error with respect to his or her reference index. • You believe • The manager should be able to meet your tracking error requirement of 75 bps 90% of the time (p = 0.90). • You have eight periods of observation during which the manager met the objective six times. • You will examine P(X < 7|p = 0.90, x = 6, n = 8). • Solution: P(X < 7|p = 0.90, x = 6, n = 8) = 0.1869.

Expected Number of Defaults Example • Determine the number of expected defaults in a bond portfolio with 25 issues. • The estimated annual default rate is .107. • Over the next year, what is the expected number of defaults in the portfolio, assuming a binomial model for defaults? np = 25(0.107) = 2.675 • Estimate the standard deviation of the number of defaults over the coming year. np(1 − p) = 25(0.107)(0.893) = 2.3888 • Critique the use of the binomial probability model in this context.

Continuous Uniform Distribution Example Given: • There is an interest coverage requirement of 2.0. • EBITDA ranges from $40 million to $60 million. • Interest is expected to be $25 million. • If the outcomes for EBITDA are equally likely, what is the probability that EBITDA/interest will fall below 2.0, breaching the covenant? 50% • Estimate the mean and standard deviation of EBITDA/interest. 2.0 and 0.0533

Common Stocks and Normality You have a portfolio with • Weighted average forecast mean of 0.12. • Forecast standard deviation of 0.22. • Calculate and interpret a one-standard-deviation confidence interval for portfolio return, with a normality assumption for returns. • Calculate and interpret a 90% confidence interval for portfolio return, with a normality assumption for returns. • Calculate and interpret a 95% confidence interval for portfolio return, with a normality assumption for returns.

Common Stocks and Normality • What is the probability that portfolio return will exceed 20%? • What is the probability that portfolio return will be between 12% and 20%? In other words, what is P(12% ≤ Portfolio return ≤ 20%)? • You can buy a one-year T-bill that yields 5.5%. This yield is effectively a one-year risk-free interest rate. What is the probability that your portfolio’s return will be equal to or less than the risk-free rate?