Download

1 / 44

440 likes | 459 Views

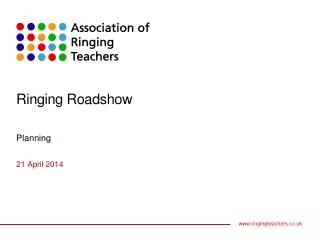

International Roadshow Presentation. April 2005 www.liberty.co.za. Liberty Life. Shareholder structure. Structure. Standard Bank. (54,65%). Liberty Holdings Limited. (50,17%). Liberty Group Limited. Life Assurance. Asset Management. Liberty Personal Benefits

E N D

International Roadshow Presentation April 2005 www.liberty.co.za

Liberty Life Shareholder structure

Structure Standard Bank (54,65%) Liberty Holdings Limited (50,17%) Liberty Group Limited Life Assurance Asset Management • Liberty Personal Benefits • Liberty Corporate Benefits • Liberty Active (Charter) • STANLIB (37,4%) • Liberty Ermitage • Liberty Properties

Liberty Life People the cornerstone of our business

Liberty Life Overview of business

Mix of business (2004) Market related (linked) Reversionary bonus Smoothed bonus Non profit • Total new indexed premiums * • Total in force indexed premiums * 7% 7% 17% 19% 5% 6% 71% 68% * Indexed refers to recurring premiums plus 10% of single

Overview of premiums (2004) Individual Group • Total new indexed premiums * • Total in force indexed premiums * 15% 24% 85% 76% * Indexed refers to recurring premiums plus 10% of single

Life insurance operations 35 30 25 20 15 10 5 0 • New individual business market share (including Liberty Active) % 27 26 25 25 24 23 20 20 17 15 Recurring individual Single individual Year ended 31 December 2000 Year ended 31 December 2001 Source: LOA market share statistics for all life offices Year ended 31 December 2002 Year ended 31 December 2003 Nine months ended 30 September 2004

Individual average new recurring premiums Source: LOA market share statistics for all life offices

Market share – corporate benefits • Not comparable due to size of funds targeted • Number of schemes: 9 500 • Number of members: 287 000 • Typically funds with 10 to 300 employees • Scale of business to change significantly

Liberty Life Our key financial value drivers

Driving improved performance through higher ROEV’s • ROEV = EV earnings/EV • EV earnings drivers • new business profits • managing the in-force • costs • mortality/morbidity • persistency • investment performance • Capital management • capital management committee • Capital Alliance • debt

Seven key financial measures These items drive ROEV

New business premiums Total +15% to R13 440m Individual life +22% to R11 374m Corporate benefits -12% to R2 066m Indexed new business premiums Total +10% to R4 186m Individual life +11% to R3 544m Corporate benefits +3% to R642m Life insurance operations 12000 12000 10000 10000 8000 8000 6000 6000 4000 4000 2000 2000 0 0 2001 2002 2003 2004 Rm +22% +11% -12% +3% 2001 2002 2003 2004 Rm Corporate benefits Individual life

Total in force business premiums Total +13% to R20 544m Individual life +21% to R16 359m Corporate benefits -8% to R4 195m Indexed in force business premiums Total +17% to R11 343m Individual life +17% to R8 571m Corporate benefits +18% to R2 771m Life insurance operations +21% +17% -8% +18% Rm Rm Corporate benefits Individual life

New business • CAGR of 11,3% in total new business (5yrs) • Consistent market share gains • Upper income segment – growing disposable income • Standard Bank’s client base presents further opportunities • Changing model for corporate benefits business • Liberty Active (Charter) for the future • New product development unit

Value of new business and new business margins* 815 30% 28% 609 605 26% 455 24% 24.4% 391 22% 20.3% 20% 19.9% 18.5% 18% 17.6% 16% 2004 2000 2001 14% 2002 2003 Rm 600 900 800 700 400 300 200 100 500 0 Value of new business New business margin • Margins exceeded our longer term average of 18-22% • Individual margins range 20-24% • Corporate margins range from 6-10% * Value of new business divided by indexed new business premium

Headline earnings Operating profit from insurance operations Revenue earnings attributable to shareholders’ funds

Headline earnings • Operating profit from insurance operations: • Reasons for volatility and decrease since 2000 • 10% shareholders’ participation in investment returns • once off items capitalised by valuation basis e.g. expense profits (or losses) • stochastic modelling of guarantee reserves • AC133 (to be followed by IFRS4 and IAS compliance) • Other earnings contributors: • STANLIB, Liberty Ermitage, trading portfolio and Liberty Properties • Return on other shareholders’ investments • equities • bonds • cash/preference shares • offshore

Life insurance operations 6000 5000 4000 3000 2000 1000 0 -1000 -2000 • Net cash inflows from insurance operations • Total -19% to R3 640m • Individual life +76% to R5 492m • Corporate benefits -234% to -R1 852m R5 492m -R1 852m 2001 2003 2002 2004 Rm Net cash inflows from individual life business Net cash inflows from corporate benefits business

Net cash inflows from insurance operations • Useful when read together with new business growth • In-force book is being managed better • Customer service drive and STANLIB’s investment performance should improve retention • Maturities of property backed products in second half of 2004 of R2bn • Total inflows of R22.6bn (2003 R18.3bn) including asset management inflows

Expenses • Business structure to be restructured into front and back office eliminating duplication • Capital Alliance assists with focusing on efficiencies • Expect once off restructuring costs, but enduring benefit • Targeting expense cost per policy increase at 4.25% • Headcount for Liberty Life & Stanlib reduced by >400 since 30 June 2003, but… • Growing headcount in Liberty Active

Expenses – controlling headcount 3600 3500 3400 3300 3200 3100 3000 2900 2800 • 251 people taken on in October 2003 as part of IEB acquisition • IT outsourcing and HR restructuring - reduction of 95 people • Group expenses increased 5% • Maintenance cost per policy increased +3.5% in Liberty and -4.9% in Liberty Active 3472 3353 3320 3221 3069 Dec 02 Mar 03 Jun 03 Sep 03 Dec 03 Mar 04 Jun 04 Sep 04 Dec 04 Liberty headcount including IEB Liberty headcount excluding IEB

Embedded value Rm Shareholders’ finds Value of in force business BEE impairment Fair value adjustment

Capital adequacy times Times covered incl BEE Times covered

Capital management • Capital management committee • Long-term shareholder portfolio established • Successful Liblife B.V. bond redemption • Application to the FSB to issue debt - conditional approval received • BEE transaction successfully implemented • Offer made for Capital Alliance • Dividend policy introduced

Capital management-dividend policy • Objectives: • predictable growth • less volatility • leave room for new business growth • strong capital adequacy • Yield on EV per share of approximately 4,75% as a base • Going forward – aligned to medium term growth of EV • taking into account: • economic conditions; and • CAR cover >1,5 • interim dividend at 40% of previous full year

Risks and issues • Increasing compliance and regulatory requirements • Volatile investment markets • Risk averse investors • Perception of industry • AIDS (not as much an issue for Liberty Life)

Some positives are emerging • Industry has started recognising its shortcomings • Emerging middle class - a reality, but net spenders • South African economy - a success story • Investors becoming more bullish • Good local investment returns • Cash being accumulated by investors = opportunity

A simple business model • Liberty’s business is conceptually simple and generic • We develop products • We sell products • We receive money • We invest the money according to product specification • We administer according to product specification • We pay benefits

Focus areas for next twelve months • Exciting opportunities • Operational restructuring opportunities • Capital Alliance • new business • efficiency • Products • Capital structuring • Liberty Activeand, as always ... people ... service … costs

Why Liberty Life? • Pure, focussed South African life insurance company • Strong parent • Strong equity play • Low smoothed bonus business • Improved returns through better capital management and efficiencies • A history of delivery

Why Liberty Life? • High dividend yield at current price • Future growth opportunities (market segments) • Revised top team – good mix of insurance and general management experience • Uncomplicated strategy • Share price offers value!

Appendix Insurance industry in South Africa

Competitors * As at 31 March 2005

Total new business Rm 2002 2003 2004 I = Individual; G = Group

Indexed new business * Rm 2002 2003 2004 * Indexed new business as per embedded value statement

Net flow of funds from life insurance operations Liberty Sanlam Old Mutual Momentum Discovery (Life) Rm 2002 2003 2004

Embedded value Rm LGL SLM OML MOM DSY VIF NAV and subs

International Roadshow Presentation April 2005 www.liberty.co.za