Cost Analysis Chapter 8

Cost Analysis Chapter 8. The meaning and measurement of cost Short-run Cost Functions Long-run Cost Functions Scale Economies and Cost Appendix 8A : Cobb-Douglas & Long Run Cost. 2002 South-Western Publishing. The Object of Cost Analysis.

Cost Analysis Chapter 8

E N D

Presentation Transcript

Cost AnalysisChapter 8 • The meaning and measurement of cost • Short-run Cost Functions • Long-run Cost Functions • Scale Economies and Cost • Appendix 8A: Cobb-Douglas & Long Run Cost 2002 South-Western Publishing

The Object of Cost Analysis • Managers seek to produce the highest quality products at the lowest possible cost. • Firms that are satisfied with the status quo find that competitors arise that can produce at lower costs. • The advantages once assigned to being large firms (economies of scale and scope) have not provided the advantages of flexibility and agility found in some smaller companies. • Cost analysis is helpful in the task of finding lower cost methods to produce goods and services. 1999 South-Western College Publishing

Managerial Challenge:US Airways • US Airways created in mergers with Allegheny, Mohawk, Lake Central, Pacific Southwest and Piedmont Airways. • Mostly in the East, with high cost but high yields (most seats were filled). • But, this situation invites entry by competitors by Continental or others. • The key to US Airways’ survival lays in managing its high cost.

Meaning of Cost There an Many Economic Cost Concepts Opportunity Cost -- value of next best alternative use. Explicit vs. Implicit Cost -- actual prices paid vs. opportunity cost of owner supplied resources.

機會成本(Opportunity Cost) • 定義 • 在所有被放棄的可能方案中,所能帶來的最大可能淨收益 • 揭露相關的成本有兩種方式 • 直接把所有可能的方案都列出來 • 利用機會成本的概念 • 機會成本帶有相關性,但可能不反映在會計報表中 • 必須透過分析才能發現 • 機會成本是財務上非常重要的概念 • 支撐「附加價值」的概念,如今常出現在公司的年報中

案例8-5 機會成本 • 永安集團在香港上市,旗下百貨公司擁有很久歷史 • 百貨公司總店,香港Des Voeux Road • 底層:25,000平方英尺 • 其他層面:64,000平方英尺 • 永安集團該對旗下百貨公司收多少房租? • 製造壓縮機有規模經濟 • 變成製造空調和冰箱的多樣化經濟 • 另外,顧客是一樣,所以在銷售方面,用同一品牌即可得到多樣化經濟

案例8-5 機會成本(續) 單位:百萬港幣

案例8-5 機會成本(續1) • 零售地產市場是競爭性的:永安應該收取市場租金 • 假設永安將零售場地租給其他承租人並賺取了5,300萬港幣 • 某種程度上,永安有向百貨公司收取租金,但沒有達到市場租金 • 除了市場租金,永安集團應考慮其他因素 • 從百貨公司到辦公樓承租人有什麼外部性? • 另外考慮 • 飯店、咖啡店和停車場對百貨公司有什麼外部性?

Examples of Relevant Cost Concepts • Depreciation Cost Measurement. Accounting depreciation (e.g., straight-line depreciation) tends to have little relationship to the actual loss of value • To an economist, the actual loss of value is the true cost of using machinery. • Inventory Valuation. Accounting valuation depends on its acquisition cost • Economists view the cost of inventory as the cost of replacement.

Unutilized Facilities. Empty space may appear to have "no cost” • Economists view its alternative use (e.g., rental value) as its opportunity cost. • Measures of Profitability. Accountants and economists view profit differently. • Accounting profit, at its simplest, is revenues minus explicit costs. • Economists include other implicit costs (such as a normal profit on invested capital). Economic Profit = Total Revenues - Explicit Costs - Implicit Costs

相關性原則 • 只應考慮相關成本,忽略其他成本 • 整個行動過程中,哪些成本是相關的 • 相關成本可能很隱蔽 • 不相關成本極可能出現在報表裡 • 會計原理 • 注重客觀而確定的數字 • 可以被缺少商業知識的獨立審計師批准 • 會計報表不一定能為管理決策提供最有用的訊息

Sunk Costs -- already paid for, or there is already a contractual obligation to pay • Incremental Cost - - extra cost of implementing a decision = TC of a decision • Marginal Cost -- cost of last unit produced = TC/Q • SHORT RUN COST FUNCTIONS • 1. TC = FC + VC fixed & variable costs • 2. ATC = AFC + AVC = FC/Q + VC/Q

沉沒成本(Sunk Cost) • 定義 • 已經(或承諾)支出而無法挽回的成本 • 另外的行動 • 先前的承諾 • 較少承諾→較少沉沒成本 • 計畫期的長短 • 較長的計畫期→較少沉沒成本

沉沒成本(Sunk Cost)(續) • 沉沒成本是商業策略的重要概念 • Qwest光纖網絡的沉沒成本阻止了新進入者 • 技術密集型產業:高沉沒成本 • 與傳統投資相比,研發成本不易回收

案例8-9 蘋果公司的訂價策略 • 1988年夏天 • 以每顆38美元的價格買下共計幾億美元的百萬位元的DRAM • 1989年元月 • 市場價格跌到23美元 • 為給Macintosh訂價,百萬位元的DRAM庫存該是多少成本

案例8-9 蘋果公司的訂價策略(續) • 蘋果電腦沒有將15美元的差異作為沉沒成本 • 將最終產品訂價在較高的位置上 • 無法銷售高階產品,只能銷售低階產品 • 毛利從1988年的51.5%下降到1989年第二季的46.2% • 蘋果電腦應該不理會沉沒成本 • 極端情形:假使蘋果電腦的市場部從現貨市場購買存儲器 • 價錢是23美元,這就比倉庫存貨來得便宜

沉沒成本:策略影響 • 在第九章詳細分析這些策略影響 • 鎖定顧客 • Microsoft讓學生以特價購買軟體,目的就是使他們習慣這些軟體 • 推廣牛奶與孕婦 • 台灣例子 • 驅逐競爭對手 • 減少未來的邊際成本,例如Qwest

沉沒成本與固定成本 • 並非所有沉沒成本都是固定的 • Qwest鋪設48束10GBPS的光纖:一旦發生就沉沒 • 但最初也可以選擇較少的束數 沉沒 成本 固定 相關 變動

沉沒成本與固定成本(續) • 假設,簽訂三年的勞動合約來滿足全職生產工人 • 所有勞動報酬成本是沉沒的 • 但是事先可以談判若干不同的工資或更具彈性的條件 • 並非所有固定成本都是沉沒的 • 例如,所有商用飛機必須要有一位飛行員和領航員,這就是固定成本 • 但不是沉沒成本,因為從這個線路轉移到另一條線路,可以辭退飛行員

Short Run Cost Graphs MC ATC 3. 1. AVC AFC AFC Q Q MCintersects lowest point of AVC and lowest point of ATC. When MC < AVC, AVC declines When MC > AVC, AVC rises 2. AVC Q

邊際成本與平均成本 • 邊際成本 • 每增加一單位產出所須增加的生產成本 • 平均成本 • 又稱為單位成本 • 總成本除以總產量 • 總成本曲線 • 變動成本曲線平行上移,移動量為固定成本

圖4-2 短期邊際成本與平均成本 3.00 成本(千元) 2.50 邊際成本 2.00 平均成本 1.50 平均變動成本 1.00 0.50 0 2 4 6 8 生產量(千個 / 週) • 邊際產量遞減 (diminishing marginal product)使邊際成本曲線和平均成本曲線上升

AP & AVC are inversely related. (ex: one input) AVC = WL /Q = W/ (Q/L) = W/ APL As APL rises, AVC falls MP and MC are inversely related MC = dTC/dQ = W dL/dQ = W / (dQ/dL) = W / MPL As MPL declines, MC rises Relation of Cost & Production Functions in SR prod. functions AP MPL AVC MC cost functions

短期邊際成本、平均變動成本和平均成本 • 邊際產量 • 每增加一單位投入所增加的產出 • 從生產量=0開始 • 平均變動成本隨著產量增加而下降 • 因為被divide by愈大生產率 • 平均(總)成本類似

短期邊際成本、平均變動成本和平均成本(續)短期邊際成本、平均變動成本和平均成本(續) • 邊際產量遞減(diminishing marginal product) • 平均變動成本隨著產量增加而上升 • 平均(總)成本隨著生產率的增加而增加 • 邊際成本、平均變動成本與平均成本三條曲線都顯現出「U」字型

Problem • Let there be a cubic VC function: VC = .5 Q3 - 10 Q2 + 150 Q • find AVC from VC function • find minimum variable cost output • and find MC from VC function • Minimum AVC, where dAVC/dQ = 0 • AVC = .5 Q 2 -10 Q+ 150 • dAVC / dQ = Q - 10 = 0 • Q = 10, so AVC = 100 @ Q = 10 • MC= dVC/dQ= 1.5 Q2 - 20 Q+ 150

Long Run Costs SRMC1 • In Long Run, ALL inputs are variable • LRAC • long run average cost • ENVELOPE of SRAC curves • LRMC is FLATTER than SRMC curves SRAC1 LRMC LRAC Q

個別廠商的長期供給曲線 • 和短期相似 • 從會計科目數據開始 • 分析並確認邊際成本和平均成本 • 利潤極大化原則 • 價格等於邊際成本是確定產量 • 長期和短期的原則相同 • 但使用長期價格和長期邊際成本

個別廠商的長期供給曲線(續) • 對製造業和服務業的分析是相同的 • 製造業—生產量,比如對汽車生產商來說,就是每年的汽車生產數量 • 服務業—運轉量,比如對電信營運商來說,就是每月通訊的分鐘數

Long Run Cost Functions: Envelope of SRAC curves Ave Cost SRAC-small capital SRAC-med. capital SRAC-big capital LRAC--Envelope of SRAC curves Q

Economists think that the LRAC is U-shaped • Downward section due to: • Product-specific economies which include specialization and learning curve effects. • Plant-specific economies, such as economies in overhead, required reserves, investment, or interactions among products (economies of scope). • Firm-specific economies which are economies in distribution and transportation of a geographically dispersed firm, or economies in marketing, sales promotion, or R&D of multi-product firms.

Flat section • Constant returns to scale • Upward rising section of LRAC is due to: • diseconomies of scale. These include transportation costs, imperfections in the labor market, and problems of coordination and control by management. • The minimum efficient scale (MES) is the smallest scale at which minimum per unit costs are attained. • Modern business management offers techniques to avoid diseconomies of scale through profit centers, transfer pricing, and tying incentives to performance.

Equi-marginal Principle in LR • Since, LR costs are least cost, they must be efficient; that is, obey the equi-marginal principle: MPX/CX = MPY/CY. • That is, the marginal product per dollar in each use is equal.

Cost Functions and Production Functions: LR Relationships and the Importance of Factor Costs C. DRS & Constant Factor Prices A. CRS & Constant Factor Prices: AC TC AC Constant cost Q 2Q Q 2Q B. IRS & Constant Factor Prices: Doesn’t quite double output TC D. CRS & Rising Factor Prices -- looks like “C” AC Q 2Q More than doubles output

Problem: Let TC & MC be: • TC = 200 + 5Q - .4Q2 + .001Q3 • MC = 5 - .8Q + .003 Q2 a. FIND fixed cost FIND AVC function b. FIND minimum average variable cost point c. If FC rises $500, what happens to minimum average variable cost?

TC = 200 + 5Q - .4Q2 + .001Q3 MC = 5 - .8Q + .003 Q2 a. FIND fixed cost FIND AVC function Answer: FC = 200 and AVC = 5 - .4Q + .001Q2. b. FIND minimum average variable cost point Answer: First find dAC/dQ = 0:From (a) that is: -.4 + .002Q = 0, so Q = 2,000 c. If FC rises $500, what happens to minimum average variable cost? Answer: No change, since AVC doesn’t change.

Cobb-Douglas Production Function and the Long-Run Cost Function: Appendix 8A • Long Run Costs & Production Functions: 1 Input • In the long run, total cost is: TC = w·L, where w is the wage rate. • production function is Cobb-Douglas: Q = Lß. • Solving for L in the Cobb-Douglas production function, we find: L = Q1/ß. • Substituting this into the total cost function, we get:

TC = w·Q1/ß. This also demonstrates that if the production function were constant returns to scale (ß=1), then TC rises linearly with output and average cost is constant. If the production function is increasing returns to scale (ß >1), then TC rises at a decreasing rate in output and average cost is declining. If the production function is decreasing returns to scale (ß<1), then TC rises at an increasing rate in output and average cost rises. One Input Case

With two inputs, long run cost is: TC = w·L + r·K, where w is the wage rate and r is the cost of capital, K. Cobb-Douglas: Q = K·Lß. The manager attempts to minimize cost, subject to an output constraint. This is a Lagrangian Multiplier problem. Min L = w·L + r·K + ·[ K·Lß - Q ] Taking derivatives and solving yields a total cost: TC = w·L* + r·K* = TC = w·Q(1/(+ß))·(·w/ß·r)(ß/(+ß)) + r·Q(1/(+ß))·(·w/ß·r)(/(+ß)) If (+ß>1), then 1/(+ß) less than 1, and total cost rises at a decreasing rate in output. That means that average cost declines. TWO Input Case

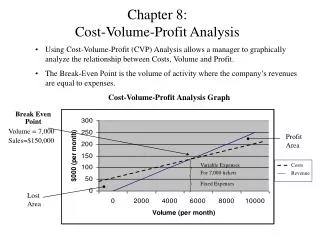

長期收支平衡 • 是否進入 / 退出 • 價格≧平均成本 • 營業規模 • 邊際成本=價格 • 環境條件和短期決策的十分相似 • 關鍵區別為所有變量是對長期而言的 • 長期邊際成本可能和短期的不同 • 長期價格可能和短期的不同

圖4-6 長期產量 成本/收益(元 / 個) 長期邊際成本 長期平均成本 0.70 邊際收益=價格 收支平衡點 0 3.4 產量(千個 /週)

案例4-4 富士通:杜翰市與格力斯翰市 • 已投資英國杜翰市5.9億美元 • 現有設備僅能生產4和16百萬位元DRAM • 需投資10億美元才可生產64百萬位元DRAM) • 長期價格<平均成本(包括重置成本) • 格力斯翰市 • 平均變動成本<長期價格<平均成本 • 註釋 • 這只是作者對真實情況的解釋,不包含有關成本的內部訊息

案例4-5 石油:該不該生產呢? • 原油價格上升時,油井平台的數量增加 • 原油價格下降時,油井平台的數量減少