Automobile title loan

0 likes | 17 Views

A Loan Can provide you with A Hand Up<br/>Owning the great things you deserve may possibly appear to be out of attain. Thats one thing

Automobile title loan

E N D

Presentation Transcript

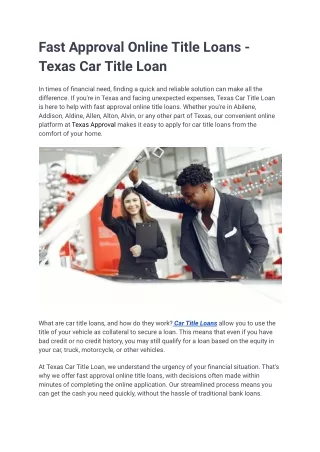

Car or truck Title Loan When you would like dollars, usually periods the need is instant. Finance providers occasionally provide a simple way out of financial difficulties by providing a car title bank loan. However, clientele are misled by the short funds that an auto title personal loan offers. Tagged as abusive, automobile title loans charge exceptionally high curiosity fees of as much as 360%. To receive a auto title mortgage, The buyer ought to signal above their vehicle title as collateral. Build as open-ended credit history, automobile title financial loans aren't subject to an fascination rate Restrict or a maturity day. So So how exactly does one particular get to possess a car title financial loan? Its very simple. A customer enters the finance Workplace to apply for a car or truck title financial loan and is particularly asked simply how much cash they want to borrow. Without any credit Check out and no delay, the borrower can get hold of a mortgage by exchanging their car title and an additional set of keys for their car as collateral. The financial loans are generally under $1,000. The borrower then will make the 1st payment following 15 times and afterwards each individual 30 days thereafter. The borrower pays 1 p.c fascination a day and have to pay back no less than 10 per cent of the personal loan principal with each payment, excluding the primary payment. Every car title financial loan has an annual proportion level of around 360%. When the vehicle title financial loan may be paid out off early without having penalty, the car can be repossessed with one particular skipped payment. Unfortunately, numerous borrowers are shedding their transportation for this reason. This “Secured lending†is alleged to be less costly for borrowers than unsecured lending because the lender can appear to collateral from the celebration of default. That protection suggests that it is a kind of lending that is inside of a vastly diverse category than payday loans and should not be when compared to it. The motor vehicle title lenders have prevented curiosity rate limits by structuring the personal debt as open up-ended credit, like bank cards. Open up-end credit score was deregulated because federal regulation Permit out-of-point out card issuers export their no-cap law. The legislature has never resolved that secured, small loans needs to be deregulated. Most safe title loans are charging a A great deal higher fascination level than unsecured credit cards. Charge cards are unsecured, and therefore far more dangerous than secured loans. Despite the greater danger, the current average curiosity fee billed by bank card companies is 12.five% . Yet car title loans which happen to be secured by cars that are owned free and crystal clear by the title mortgage borrowers, are increasingly being charged costs which have been 29 moments the rate getting billed on credit cards. Due to astronomical yearly proportion costs and due to the significant repossession amount, the very first payment on these loans is owing a scant 15 times soon after borrowing The cash. Failure to create the main payment of your automobile title bank loan, or Anybody payment thereafter brings about repossession. When no facts is currently available on repossessions of automobiles, at one particular Browse around this site auction household, above a hundred and fifty autos have already been offered following becoming repossessed. There is usually the lack of equity. By way of example, For most Iowans their car is their most respected asset. Motor vehicle title loans put this asset in danger and Iowans are getting rid of all of their fairness to your astronomical interest premiums. With the unlucky consumers who eliminate their vehicle to repossession any excessive fairness They could have built is eaten via the repossession expenses and curiosity price expenses. The “economical emergency†that necessitated the Determined motor vehicle title personal loan for these buyers is never as shorter-lived since the financial loan conditions, Therefore the interest quickly mounts as paying the financial loan off having a balloon payment is often impossible. It'll look that in a car or truck title bank loan, you wont be capable to escape in any way. Here are some guiding concepts from An economical bank loan expression. These should preserve you away from vehicle title loans also: Establish Truthful and Very affordable Loan Phrases. Title-secured loans should be repayable in affordable installments instead of a lump sum. Is your car title personal loan such as this? Premiums really should be constrained, and lenders need to be necessary to think about the borrowers capability to repay Protect Borrowers After a Default. States need to bar abusive practices such as seizing cars all of sudden, pocketing the difference between the gross sales selling price and just what the borrower owes or pursuing the borrower for even more money following repossessing the vehicle. Close Loopholes to Ensure Steady Regulation. States that allow title lending ought to near loopholes that exempt some financial loans within the legislation and ensure that legal guidelines use to all lenders, like Individuals operating across state strains. Monitor Lenders Improved. States should really intently observe lenders by way of sturdy licensing, bonding, reporting and examination specifications. Ensure Borrowers Can Work out Their Rights. Car title personal loan borrowers should be capable of sue title lenders and void contracts that violate the legislation. Binding mandatory arbitration clauses that deny borrowers a fair chance to problem abuses in court ought to be eradicated.