Download

1 / 0

0 likes | 188 Views

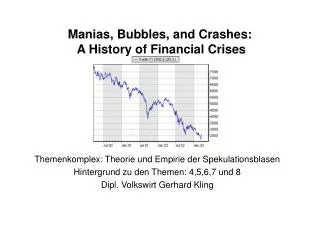

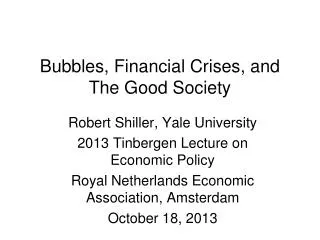

Bubbles, Financial Crises, and The Good Society . Robert Shiller , Yale University 2013 Tinbergen Lecture on Economic Policy Royal Netherlands Economic Association, Amsterdam October 18, 2013. Part I: Bubbles and Financial Crises. USA Real S&P500 and Earnings 1871-2013.

E N D