Download

1 / 41

420 likes | 615 Views

Investment incentive system in Tunisia. THE QUESTION. To know whether using tax and financial instrument to promote private investment is cost efficient option

E N D

THE QUESTION • To know whether using tax and financial instrument to promote private investment is cost efficient option • OR it would be better to rationalize these incentives while investing in other more efficient instruments by focusing more on improving company business climate (ie: infrastructure networks and investment and trade facilitations).

CONTENTS • TUNISIA AN ATTRACTIVE LOCATION FOR INVESTMENT • CURRENT TAX AND FINANCIAL INCENTIVE SYSTEM (Strengths, Weaknesses, Opportunity, Threat ) • NEEDED REFORMS (a gradual process of reforms)

AN ATTRACTIVE LOCATION FOR INVESTMENT • A strategic position in the mediterranean area • Solid macro economic fondamental • Strong achievements in human capital development • Increasing openess of the economy • A diversified economy • Generous investment incentives

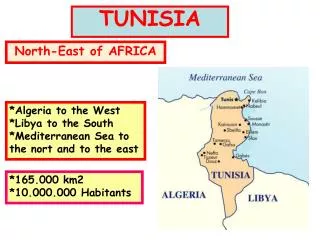

A STRATEGIC POSITION IN THE EURO-MEDITERRANEAN AREA • Strategic geographical position: Tunisia is considered to be at the crossroads of continents • It is located in North Africa. At 140km from Italy • It is less than three hours flying time from major European, sub-saharan Africa and Middle East cities.

Solid macro economic fundamental • Solid GDP growth since the mid-1960sConstantly growing real incomes of 5 % a year since mid- 1960(2007 forecast : 6,1%) • Fiscal and current account deficits have remained manageable(-2.7% and -2.9%, respectively) • Inflation low: 2.9% a year(1996-2006) • Public externel debt declined to 54.5% in 2006 and is expected to come down further (Tunisia has always honored its commitments and never asked for rescheduling of debt) • Exhibiting resilience to exogenous shocks especially in the two latest decades (such as a severe drought in 2002, the september 11 shock which hurt tourism) • GDP per capita reached $7,447(in PPP) in 2005: the second highest in the maghreb(after Libya’s) • Since mid- 1960’s contribution to per capita GDP growth Productivity (51%)>traditional factor contribution (49% )

Strong achievements in human capital development • This reflects the country’s steady investment in education and health since the early 60’s offering today • Human development index well above the average for developing countries • Life expectancy is 74.4 years • 80% of households belong to middle class and own their homes • Poverty has gone down to less than 4% • A skilled workforce with a great capacity of apprenticeship and a recognized know-how • 1 out of 4 Tunisians is in school (The budget for education accounts7%of GDP) • About 57% of new job seekers are university graduates, with competitive labor costs compared to other emerging markets. • 500,000 is the forecast of the number of students in Tunisia by 2009. • Faster Demographic transition than in neighboring countries:Fertility rate declined from 7 children per woman in 1961 to 2.04 in 2005

increasing openness of Tunisian economy to international competition • Productivity growth reflects also the opening of the industrial sector to competition(as well as rapid development of an offshore sector largely integrated with EU production networks) • Tunisia has opted to integrate the world economy in a “preferential fashion” : - 96% of tunisian external trade is made under FTA regime: EU (already implemented by 2008), Great Arab FTA,EFTA, Aghadir,Turkey… - Average tariff faced by EU industrial products dropped from about 100% in 1996 to about 4% in 2007( while the non preferential partners average is about 24% )

A diversified economy • Electronics : leading sector on a steep rise (more than 15%) • Services gaining ground (57% of GDP in 2006)

Export-oriented economy • The Tunisian economic growth is mainly driven out by exports: 50% the share of exports in GDP. • The share of fuel exports plummeted (from 52% in 1980 to 13% in 2006)giving way to textile and clothing (from 18% to 33% ) and engineering and electrical components (from 9.5% in 1995 to 19% in 2006)

A competitive country • The Global Competitiveness Report 2006-2007 released by the World Economic Forum ranked Tunisia out of 125 developed and emerging countries • 30thin terms of global competitiveness • 26thin termsof business competitiveness • Tunisia is rated « flat » with the prospect of upgrading to « stable » by standard and poor’s and european company Fitch Ratings(BBB and BBB+ by japanese rating agency)

CURRENT TAX AND FINANCIAL INCENTIVE SYSTEM (Strengths, Weaknesses, Opportunity, Threat )

The investment incentives code • Common incentivesgranted to all invesments in the activities eligible for invesment incentive code • Specific incentives granted according to major priorities • Export • Regional development • Agriculture development • Transfer of technology • Environment protection • Additional incentives granted to projects having a particular interest to the national economy or to the border zones

Strenghts • Free investment (Investment can be freely carried out by a simple declaration) • Generous system (fully exporting and regional development regimes) • Supporting institutions • Almost all sectors are covered (except mining, energy, the financial sector and domestic trade which governed by special legislation)

Free investment Investment can be made after submitting a simple « declaration of investment intentions » to • The Agriculture Investment Promotion Agency for agriculture and fishing activities • The Tunisian National Tourism Board for tourism activities • The Tunisian National Handicrafts Board for handicrafts • The Industry Promotion Agency for industrial and all remained activities

Generous system Most used instruments • Corporate income tax holiday: 41% • Tax exemptions: 34% • Investment grants:13% This reflects the country’s incentive strategy: • Fully exporting sectors • Regional development • Agriculture development

Major incentives for fully exporting companies • 10-yearfull tax exemption on profits, then a reduced income tax of 10% from the 11th year of operation, onward • Duty free raw material and equipment imports

Major investment incentives in regional development areas • 10-year full corporate income tax exemption and a 50% tax deduction on profits or revenues the next10 years. • Investment grants of 15% to 25 % of the investment cost depending on the selected area • Assumption of social costs • Assumption of certain infrastructure expenses

Supporting Institutions • Many supporting institutions such as investment promotion agencies, are at the investors’ service to help them set up their companies in Tunisia in the best possible conditions. • Investors are entitled to freely benefit from a one-stop-shop to complete all their formalities within 2 days • Companies can also perform their customs clearance on site

However, compared to other high growth countries and despite solid macro economic fundamental and generous investment incentives in place,Tunisian growth was driven more by public and less by private investment.

Weaknesses • Exception to free investment:For Some services activities ,foreign investment requires prior agreement of the investment commission • Costly system • Many sectoral investment promotion agencies • Less targeted system : Multiplicity of exemption regimes (Inside and out side investment incentive code)

Investment incentivescost • 5 US$ billion(cumulative) • 10% of government revenue • Double in 1O years • Rapid increase of financial incentives(×3) comparing to tax incentives(×1.5)

Opportunities • Free transfer of profits and capital Same advantages for Tunisian nationals and foreigners • Rationalize these incentives while investing in other more efficient instruments by focusing more on improving company business climate • Specialized study of the projects • Some high potential sectors (Electric and electronic industry, Automotive components)

Threat • Risk of no local reinvestment of foreign companies profits • Delay Risk of Tax transition process (to substitute tariff revenue for intern tax revenue such as VAT…) • Risk of management and monotoring problems for promotion investment agencies and understanding difficulties for investors. • Much more incentives to use capital factor rather than labor factor while job creation is the first development priority • Not limited in time incentives

SWOT STRENGTHS • Free investment • Generous system(Same advantages for Tunisian nationals and foreigners) • Supporting institutions • Almost all sectors are covered WEAKNESSES • A prior agreement is needed for Some not fully exporting service activities • Costly system • Many sectoral agencies • Less targeted system :Multiplicity of exemption regimes (Inside and out side investment incentive code) OPPORTUNITIES • Free transfer of profits and capital • Rationalize these incentives while investing in other more efficient instruments • Specialized study of the projects • Some high potential sectors (Automotive components) THREAT • No local reinvestment of profits • Delay Risk of Tax transition process • Risk of management and monotoring problems for agencies and understanding difficulties for investors. • Not limited in time incentives • The system encourage more the use of capital factor than labor factor

In order to Reinforce Strengths, Avoid Weaknesses, Exploit Opportunities, Eliminate Threat, A gradual process of reforms is proposed in order to establish through operational and strategic actions a new system easy to Understand Implement Measure

ACTIONS • Reduce the dichotomy onshore/offshore • Improve procedures • More efficient instruments to promote private investment

Reduce the dichotomy onshore/offshore • Simple and reduced common law taxation regime • Unique, simple and limited preferential regime

Simple common law taxation regime • Progressive reduce of corporate tax rate taking into account tax competition with similar countries (such as Morocco) in order to • Secure the foreign investor • Reduce the incentive gap between the offshore and on shore sectors, • Increase integration and technology transfer between the two sectors. . • Reducing the number of VAT ratewhile assessing the social impact of eliminating tax exemptions on the poorest

Unique, simple and limited preferential regime (Short term actions) Reviewing investment incentive code by • Removing the unused or less used tax and financial incentives, • Keeping some financial incentive as well as customs duties exemptions or reductions granted to equipment from countries outside the EU in order to reduce the gap between preferential and the MFN tariffs and avoid the phenomenon of "trade diversion"

Unique, simple and limited preferential regime(long term actions) • One unique incentive code including all preferential regimes with simple, exceptional and limited in time incentives focusing on projects with high economic profitability. • One unique investment promotion agency (in stead of current different sector agencies), in charge of managing, monitoring and assessing investment incentives.

Improve procedures • Establishing incentive management software for monitoring and evaluating tax and financial incentives in order to ensure growing rationalization of investment aid through better incentive targeting; • Manual of procedures describing the different stages for granting incentives and clearly defining the role of each partner in the investment promotion effort. • Generalized electronic tax payment in order to Make easier to companies paying taxes

More efficient instruments to promote private investment • Strengthen assets • Reducing the rigidity of labor market: Many studies show the importance of the dismissal rules relaxation and removing firing restrictions in promoting private investment and reducing unemployment in Tunisia. • Gradual liberalization of capital account toward total Dinar convertibility

Reduce transaction costs • Strengthening infrastructure networks and improving their qualities while decreasing their costs • Strengthening the public-private partnership especially in the service sector (economic growth locomotive in Tunisia) • Trade facilitation with post and targeted control (to avoid the 100% control of goods) through prior and efficient risk management. • Deepening and harmonizing trade agreements by reducing current large gap between preferential and MFN tariff in order to avoid “trade diversion”.

RECENT TAX REFORM The government has been gradually reducing the incentive gap between onshore and offshore sectors:On december 2006, a fiscal law • Reduced the onshore corporate tax from 35% to 30% • Raised the offshore corporate tax from 0% to 10% • Offshore firms are allowed to sell up to 30% of their production in the onshore sector and be subject to the onshore tax regime on that proportion

Other tax mesures • Increase VAT reimbursement to 100% • Rebalance VAT rates(6,12,18%) and suppressed the 29% rate • Reduced the number of Tariff rates from 54 rates(2001) to only 9 rates

TRADE FACILITATION MESURES • Much effort was deployed to facilitate global integration through trade facilitation mesures • Electronic documentation procesing was introduced(tunisia trade net) • Streamlined technical controls • Improved customs procedures

Numerous logistics projects in progress • Deep Water Port • Enfidha Airport (The 8th) • Industrial Zone : Enfidha – Hergla • 6 projected logistics platforms

Thank You for Your Attention Tunisia: a competitive economy